This article is written by Esha Barua who is pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from LawSikho.

Table of Contents

Introduction

“I’m going to make him an offer he can’t refuse.” Certainly, the Acquirers are not Marlon Brando and an offer when made can be refused depending on how lucrative it is.

Buying and selling of shares are but a natural market phenomenon. The acquirers to buy their way into a company giving effect to their takeover objectives. Acquisition and takeovers are interchangeably used terms but one is slightly different from the other. Takeovers unlike acquisitions do not require the permission of a board of directors. The usual takeovers are done by acquiring a majority stake in the company.

Nowadays owing to the frequency of mergers and acquisitions the requirement of well-defined rules comes into play and that is where SEBI the Securities and Exchange Board of India exerts its powers. For this article, the discussion of such powers and obligations shall be restricted to the open offer and its process.

This article will cover what an open offer is, why it is required and when it gets triggered along with a step-by-step roadmap of an open offer process for acquiring an entity following the (SAST) takeover code.

What is an open offer?

An Open offer under the Takeover Code is an obligation as per the SEBI SAST (Substantial Acquisition of Shares & Takeover) Regulation. When the acquirer together with PAC (Persons acting in concert) holds a certain stake in the company but wishes to acquire additional share or voting rights such that the number of their shareholding combinedly, exceeds the threshold of 25% in the target company (as per the amended regulation of 2011), then to acquire additional shares the open offer obligation gets triggered. The offer size needs to be a minimum of 26% of the total equitable share capital.

Such an offer is obligatory and must be made to the public shareholders allowing them a fair exit. The open offer is to be made vide a public announcement and kept open for some 30 days (a month) from the date of its notification.

The open offer is thus a fancy legal terminology to describe the takeover offer whereby to acquire another listed company (Target) an acquirer has to propose an offer to its existing shareholders to sell their shares at an offer price determined by the acquirer.

Open offer applies to the acquisition of shares, voting rights, or control of a listed company. A listed company open offer or takeover offer can either be made by an existing shareholder or by an entirely new acquirer together with PAC holding/aiming to hold a minimum of 25 % shares/voting right and more in a company. The offer size should be at least 26 % of the total shares of the target company.

The share acceptance is done on a proportionate basis. There is no guarantee that the shares the shareholders tender to the acquirer will 100 % be accepted by the acquirer. The ratio between Total shares tendered by shareholders and those accepted by the acquirer is proportional and is called the acceptance ratio.

The letter of offer discloses information of the offer price, purpose, and management of the acquiring company and is sent to the stakeholders of the Target company while making an open offer. The addressed letter will also mention the procedures involved in accepting the stakeholders’ tendered shares.

Who are the PAC?

For the understanding of this article and the takeover regulation, PAC is Persons Acting in Concert. According to Regulation 2(q) of the SAST Regulation, PAC is the persons having a common objective as an acquirer who co-operates with the acquirer in the acquisition of shares or voting rights or the exercise of control over the company. PAC can be individuals or legal entities or companies having a common purpose for acquisition under an agreement. It can even be family members, merchant bankers, investors, and any other legal person associated with the acquirer having the same objective towards acquisition.

Types of Open Offer

Open offer can be generally of two types:

- Mandatory Open Offer;

- Voluntary Open Offer.

What triggers an open offer?

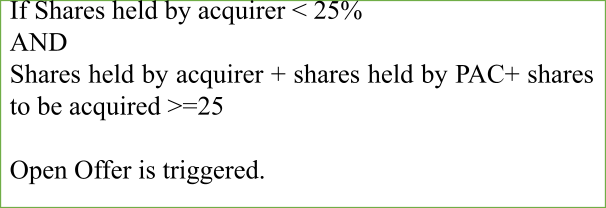

An Open offer obligation arises when the acquirer wants to acquire a certain number of shares in a target company calculated together with the shares or voting rights already held by the acquirer along with PAC which entitles them to exercise a voting right of 25% or more in such company.

The triggers can be in scenarios-

- When an individual acquirer acquires shares that exceed the threshold of 25%.

- When the aggregate of Acquirer’s shares and PAC’s shares is less than 25 % shares initially but exceeds the threshold when the initial holding is calculated in addition to the shares of PAC + shares they want to acquire, an open offer is triggered.

Again,

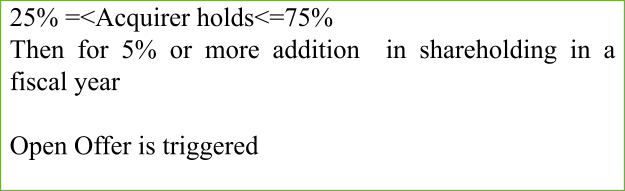

- When acquirer together with PAC has already acquired shares or voting rights in a target company which entitles them to exercise a voting right of 25% or more but less than equal to 75 % (which is the maximum permissible limit for nonpublic shareholding).

Then, to acquire additional shares or voting rights in a fiscal year that enables them to exercise an additional 5% of voting rights, a public announcement of an open offer needs to be made.

Promoters (or acquirers+PAC) holding a stake(shares/voting rights) of more than 25% and but less than 75% can acquire up to 5% additional shares/voting rights in a financial year. Creeping acquisition of less than 5% would not require an open offer to be made but any amount of shares exceeding the 5% limit will trigger the open offer obligation.

Open offer size for this purpose has to be at least 26%.

Open offers can also be voluntarily made when an acquirer along with PAC holds more than 25% of the control/voting rights/ shares of the target company and wants to acquire shares to his existing stake by making a total offer of the size of 10% of the share capital of the target. (Regulation 6).

Voluntary Open Offer is at the option of the acquirer. For example, when Uniliver PLC wanted to increase its stake in India, it made a voluntary public offer to the Public shareholders of Hindustan Unilever.

What is the need for an open offer?

As an investor when one chooses to invest in the stock of the company the basic factors that one looks at are management, business strategy, profitability, liability, along with many other important factors. When an acquirer steps over the company all of these factors can be subject to change or modification, therefore the initial reason based upon which a person had bought the stock no longer remains valid. This is the reason why SEBI, requires the acquirer to make an Open Offer so that all shareholders who bought the stock based on certain factors get an opportunity to sell when the management or control of the company is changed. It is to give the shareholders who are caught up in such a situation where they do not want to continue with the new management, a suitable exit. It is also to be born in mind that the shareholders’ vision must be in harmony with the new acquirer’s vision in case they wish to stay.

What is the Takeover Code?

A takeover can be fittingly understood as the taking over control (acquisition) of a company by another. It takes place through purchasing of shares of a company or by having sufficient controlling right over the same. It means gaining control of the ownership (shares or voting rights) of a target company.

Takeover code is a set of regulations governing the takeover mechanism.

The Substantial Acquisition of Shares and Takeover (SAST) Regulations of SEBI (Securities Board of India) is commonly known as the Takeover Code. It is the code or a rulebook that the regulatory body has created to procedurally give effect to a takeover. SEBI governing the securities market assumes the obligation to protect the rights of the vulnerable in the market.

The code regulates Takeovers or acquisitions of companies and thus prescribes the timing, procedure, the announcements that must happen, the disclosure requirements, and other procedures which should legally happen. To prevent the rights of the shareholders from being trampled upon, the takeover code was brought into being in India by the SEBI (SAST) regulation in 1994 which was then repealed by the 1997 Regulations. The present and working takeover code of 2011 is the updated version of SAST Regulations 1997 brought about by the report of Takeover Regulations Advisory Committee (TRAC) which proposed changes in the open offer processes.

What role does SEBI play?

SEBI (Securities and Exchange Board of India) established under the Securities and Exchange Board of India Act, 1992 serves the objective to protect the investors in securities, promote development, and regulate the securities market.

The takeover code is one such regulatory charter by SEBI to check the processes of a Takeover.

The rules are to protect the rights of the shareholders and the rule keeper is the securities commission.

The Code is required to ensure that there is an information efficient market and also to intrinsically ensure that shareholders are not prevented from accepting an offer when the acquisition offer is made to the company. The open offer under the takeover code is to prevent the promoters and founders from executing a secret deal that is hefty beneficial to them but leaves the shareholders hanging to dry. It is to ensure that the shareholders are sufficiently informed enabling them to decide on the acceptance or refusal of the offer.

SEBI tries to strike a balance between the rights of the shareholders and the efficiency of the takeover processes keeping market bureaucracy in the hindsight thereby facilitating takeovers. It is concerned with leveling the field for the players in the market and ensures that the takeovers happen in the right way. It acts as the umpire of the game.

What is the Open Offer Process?

An open offer process is the course of action that requires the acquirer to make an open offer to the existing shareholders of the target to accomplish a takeover. It is the procedure of realizing the acquirer’s dream of holding a majority stake in a company. An open offer is a must and it cannot be whimsically withdrawn. It can only be withdrawn in case of vis major or death of the acquirer.

Step by step roadmap for open offer

The steps taken for making an open offer before taking over are as follows:

STEP 1: Appointment of Merchant Banker [Regulation 12(1)]

The first and foremost obligation of an Acquiring company with the PAC (Persons acting in concert) is to appoint a Merchant banker who would look after the shares tendered in the open offer. This has to be made before the making of a public announcement. The merchant banker assumes all responsibility associated with the transaction. The merchant banker in no way should be related to the acquirer as well as with the target company.

STEP 2: Opening of a depository account for tendered shares

This can be done before or on the day of the public announcement. The Depository account acts as a bank and holds the securities in de-materialised or electronic form. In this case, the securities are the shares that the acquiring company might obtain through the open offer process.

STEP 3: Prior to making a public announcement the Acquirer along with The PAC has to ensure that proper financial arrangements have been made on part of the Acquirer and the acquirer would be able to uphold and implement the statutory approvals for the open offer as may be necessary.

STEP 4: Public Announcement

The public announcement is the first announcement made by the acquirer disclosing the details of the transaction and the intention to acquire the shares of the target company by the means of an open offer. The public announcement is to be made in all editions of :

- An English National daily with wide circulation.

- A Hindi National Daily with wide circulation.

- A Regional Daily with wide circulation.

The public announcement should contains basic information like:

- Identity of the PAC.

- Nature of the proposed acquisition.

- Consideration and price per share, and mode of payment of consideration.

- Offer price and minimum level of acceptance if mentioned by an acquirer.

The Public announcement has to be made on the date of agreeing to acquire the shares or voting rights or the control over the target company.

STEP 5: The Public Announcement that had been made has to be sent to:

- The Stock Exchanges.

- SEBI, through the merchant banker.

- The target company at their registered office.

Within one working day of the public announcement.

STEP 6: Opening of an escrow account

(Regulation 17)

The Acquirer along with the PAC must open an escrow account, at least 2 days before making the public statement. An amount equal to 25% of the consideration payable has to be deposited for the first ₹500 crores and an additional 10% for any amount over ₹500 crores in the escrow account. Such amount can be kept in the form of cash, bank guarantee, or deposit of freely and frequently traded shares. The bank guarantee will be in favour of the manager to the open offer and he/she will have the power to sell the shares to manage the payment of consideration. A minimum of 1% of the consideration has to be kept in the form of cash with any scheduled commercial bank which the manager to the open offer would use to make payments out of.

An Escrow Account acts as a security deposit for the Acquiring company with its PAC and a guarantee towards the shareholders of the Target company in case of non-compliance or withdrawal on the part of Acquiring company. In case of forfeiture or non-compliance to the obligations under the takeover code after the deduction of expenses,1/3rd of the amount would be moved to the target company, 1/3rd will go to the IEPF and 1/3rd will be distributed pro-rata among the shareholders who have accepted the offer.

The escrow cannot be released 30 days before the completion of the payment to shareholders who have accepted the offer. In case of withdrawal, the money would be returned to the Acquirer. Upon payment of all the considerations, the money would be returned to the acquirer within 30 days.

STEP 7: Detailed Public Statement (DPS)

The DPS has to be made within 5 days of the Public Announcement disclosing all the relevant information to the Open Offer enabling the shareholders to make an informed decision about the order. The detailed public statement has to be published in English, Hindi, and regional language daily with wide circulation where the registered office of the target company is situated and in a regional language daily in the place where the stock exchange having maximum trading of the target company’s share in the preceding 60 days.

STEP 8: Filing of draft Letter Of Open Offer (LOO)

[Regulation 16(1)]

Within 5 working days from the date of the detailed public statement, due diligence certificate along with the non-refundable fee, a draft Letter Of Open Offer (LOO) has to be filed with SEBI, and on the same day, the LOO has to be sent to the target company and the custodian of shares if any of the target company.

The open offer draft letter contains:

- Identity of the PAC

- Nature of the proposed acquisition

- Consideration and price per share

- Offer price and mode of payment of consideration

- Offer price and minimum level of acceptance if mentioned by the acquirer

STEP 9: Within 15 days the SEBI has to submit a receipt on the open offer. If no comments have been made by SEBI on the draft it would be assumed that SEBI has no comments.

STEP 10: Comments from SEBI

Within 7 working days of the receipt of the SEBI comments on the open offer, the final open offer has to be given to the shareholders to decide on the front of what they want to do. If no comments are received not later than 15 days, it has to be deemed that SEBI has no comments.

STEP 11: Adjustments before Tendering

Comments and modification if any upon the open offer has to be given by the directors of the target company 2 days before the tendering period. Revision of price of shares can be made 3 business days before the commencement of tendering period. The revisions have to be intimated to SEBI as well as the target.

STEP 12: Advertisements have to be given 1 day preceding the commencement of the tendering period which should consist of the scheduled activities for the Open Offer, status of the approvals, and procedure for tendering acceptance. Such advertisement has to be published in the same newspaper where the detailed public statement was published.

STEP 13: Commencement of tendering period

As the name suggests during the tendering period the shareholders who want to accept the offer can tender their shares in the open offer. The tendering period has to commence within 12 days from the receipt of the comments from the board and SEBI on the draft letter offer.

STEP 14: Cessation of Tendering Period

The tendering period has to be kept open for a period of 10 working days.

STEP 15: Post-offer Advertisement [Regulation 18(12)]

The acquirer has to issue a post-offer advertisement within 5 working days after the offer stating the number of shares tendered, accepted, and their dates of consideration.

The advertisement has to be published in the newspaper or media where the DPS (Detailed Public Statement) was published.

STEP 16: Opening of Special Escrow Account

For the payment of the amount to the shareholders, a special escrow account has to be opened by the acquirer.

He has to deposit the requisite amount and make the entire sum due and payable to the shareholders and empower the manager to the open offer to operate the special escrow account.

The payment of consideration can be in the form of cash, exchange, or transfer of securities and has to be completed within ten (10) working days of the expiry of tendering period.

STEP 17: Release Of Escrow Funds

The merchant banker will release the remaining escrow fund and the amount in the escrow account would be returned to the acquirer within 30 days from the payment of the consideration.

Example Of Larsen and Tubro taking over Mindtree.

Not long before the pandemic Larsen and Tubro Ltd. (L&T) had acquired Mindtree which marked the country’s first-ever hostile takeover on 26th June 2019 through an open offer process using Regulation 3(1) along with [ Reg. 4 ]. L&L is now a promoter of the IT firm Mindtree with a 60% stake and complete control over the board and management of Mindtree. L&L had bought 9% shares out of 15 % from the open market. According to reports, 120% of the open offer was subscribed while L&L offered to purchase 50.9 million shares of Mindtree from public shareholders.

8.86 Lakh equity shares of Mindtree Ltd were acquired On May 16th, 2019 which increased L&T’s shareholding from 20 to 26.48 percent. The stake was raised by buying an additional 31% of the shares in Mindtree. The latest stock purchase was made at Rs 979.81 each and

The open offer closed on June 28 marking L&L’s control over Mindtree. The shareholders who tendered their shares were given their payments as per the open offer.

Thus given below are some of the shareholders who sold their stakes to L&L who “couldn’t refuse” the offer:

|

Shareholders |

Tendered Shares |

|

Nalanda India Equity Fund |

8.90% |

|

UTI Asset Management Co. Ltd |

2.97% |

|

V.G. Siddhartha and Coffee enterprise |

20.4% |

|

Arohi Asset Management Pte Ltd. |

2.74% |

|

Nalanda Capital |

10.61% |

|

UTI Mutual Fund |

2.97% |

|

Amansa Holding Pvt. Ltd. |

2.77% |

|

Franklin Templeton Asset Management (India) Pvt. Ltd. |

1.06% |

|

Alternative Investment Funds |

1.49% |

Conclusion

Takeovers, hostile or otherwise should follow the parameters and restrictions set out by SEBI. Surviving the competition in the market, acquirers do have to follow certain set procedures The amended SAST code strives at pulling the strings on unregulated and disorganized acquisitions. The open offer is one such method of controlling the market from going haywire. The overarching philosophy of saving the rights of the shareholders in a takeover situation remains intact even under the takeover code.

If an open offer fails nothing happens legally, an open offer may fail due to the death of the acquirer the offer stands canceled and there are no legal implications. Acquisitions or takeovers are complex processes including huge transactions and require a lot of legal compliances. When the patterns of shareholdings change, scrutiny and due diligence are a must and should be correctly done under the umbrella of corporate governance.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications