In this article, Aklovya Panwar discusses the highest paying legal jobs in India.

“All men dream: but not equally. Those who dream by night in the dusty recesses of their minds wake in the day to find that it was vanity: but the dreamers of the day are dangerous men, for they may act their dreams with open eyes, to make it possible.” ~ T.E. Lawrence

India as a country has a very complex social, political and economic system. Since Independence there has been various highs and lows in India’s growth and we have also gone through various reforms in our system for the final goal i.e., development. Development is a very broad term but it is generally related to the stability, happiness and satisfaction of an Individual.

In today’s world of modernisations an individual’s satisfaction and stability can be measured by the amount of money he earns. In the urge of this stability every individual tries to seek for best fields or jobs, one among them is the stream of law where a person can earn a hefty amount by the way of their skills and abilities. The Indian legal profession today consists of approximately 12 lakh registered advocates, around 950 law schools and approximately 4-5 lakh law students across the country. Every year, approximately 60,000 – 70,000 law graduates join the legal profession in India.So now the question arises what are the best option they can opt for?

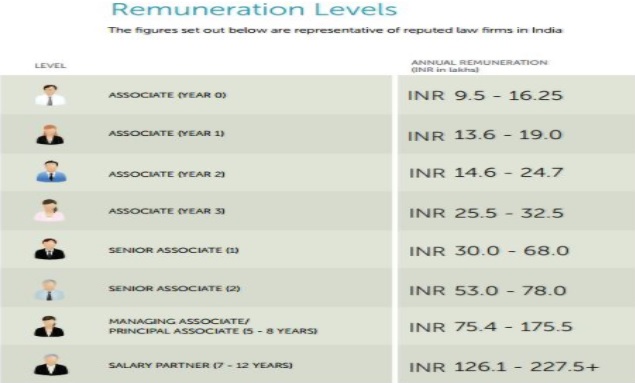

Law Firms

In India, Law firms are characteristically set up as a partnership or sole proprietorship concerns. Most law firms engage lawyers on an exclusive retainership basis. The lawyer in this arrangement is not an employee of the firm but is an exclusive consultant to the firm.

Law firms provide hefty pay amount and are one of the most grossing jobs in this field.

Here is a sample report where the remuneration in the law firms has been shown:

Top law firms in India

Rank

Company Name

Number of partners

Number of lawyers

RSG Profile Score

RSG Client Satisfaction Score

Total Score

1

Amarchand & Mangaldas & Suresh A Shroff & Co

84

655

61

8.7

37.8

2

AZB & Partners

20

295

59

8.5

35.2

2

Khaitan & Co

81

354

55

8.7

35.2

4

J Sagar Associates

79

337

41

8.7

34

5

Luthra & Luthra Law Offices

42

292

30

8.2

30.4

6

Trilegal

23

172

19

8.5

28.2

7

S&R Associates

8

53

8

8.9

27.1

8

Economic Laws Practice

25

129

5

9

26.2

9

Desai & Diwanji

27

187

12

8.5

25.8

10

Talwar Thakore & Associates

4

26

9

8.8

25

Trial lawyers

Trial lawyers are among the highest paid legal professionals in the world. It is a field where the skills and experience of the lawyer matters a lot. It is an opportunity where you can earn good amount of money by way of your performance.

Cyber Law

The advancement of technology comes as a blessing for the human kind but with that, it also costs the epitome of nuances which includes most of the online injuries. In this cyber law act as a remedy. Cyber crimes can contain criminal activities that are traditional in nature, such as theft, fraud, forgery, defamation, and mischief, all of which are subject to the Indian Penal Code. The abuse of computers has also given birth to a gamut of new age crimes that are addressed by the Information Technology Act, 2000. Cyber lawyers are in high demand as India is still exploring its online database limits. One recent example was the famous case of Right to be forgotten.

It varies on the role. The biggest factor is the merit of the law student in question. If you’re hired by a company as an in-house cyber law counsel, the starting salary would be between Rs 50,000 and Rs 60,000 per month.

Intellectual Property

Intellectual Property Laws deal with copyright, trade, and patent. As like the field is unending so does the opportunities. IP lawyers are needed in present time due to spread of awareness regarding possession. So it is another top-notch job for good earning. The starting salary would be between Rs 50,000 and Rs 60,000 per month.

Human Rights lawyer

Human rights lawyers usually get absorbed in government organisations like National Human Rights Commission (NHRC) or State Human Rights Commission, NGOs, social welfare departments, and international organisations such as Amnesty International and Red Cross. The Human rights lawyer are frequently needed in the organisations working for Human Rights. They also helps in the formation of policies.

Starting Salary: Average INR 3,00,000 per annum.

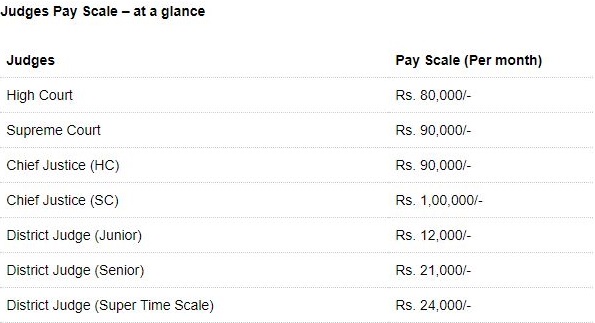

Judges

This is the most hon’ble position in the nation as judges are the providers of justice and this position is earned only by prior dedication and obstinate determination. Judges enjoy high earnings as well as other special privileges, most judges enjoy health benefits, expense accounts and contributions to retirement plans made on their behalf, increasing the size of their compensation packages.

The highest-paid judgeships are those within the Supreme and High court system, while local judges and magistrates earn the least.

Members of Parliament

Member of Parliament is not explicitly, a field for law professionals but if a person have interest in policy making and wants to understand the core execution of our political system then they can contribute their legal knowledge in the same. As One-third of the Union Council of Ministers are law degree holders India paid Rs.176 crore to its 543 Lok Sabha members in salaries and expenses over the last year, or just over Rs. 2.7 lakh a month per Member of Parliament (MP), new official data show.

Professor of Law

Nowadays, this profession is in very high demand because law school professors not only teach they also contribute in the academics by their publications and scholarly articles. Securing a position as a law school professor is competitive, however, qualifications for top candidates include a law degree from a top law school, law review, high-class standing, judicial clerkship experience, law practice experience and publication credits in scholarly journals They have specialisation in their subject by which they help in the formation of various laws and policies by proposing their research, viewpoints and ideas.

Judicial Clerkship

A law clerk or a judicial clerk is a person generally an attorney who provides straight assistance and counsel to a judge in making legal decisions and in writing opinions by exploring issues before the court. It is a perfect opportunity for the freshers as well as the law students because it not only lobs good money but also brilliant exposure of the reality of the law.

Public Prosecutor

As per the revised scale, pay scale has been changed and there is a hike in the salaries of public prosecutors.

POSITION

PREVIOUS SALARY

AFTER REVISED PAY SCALE

Assistant Public Prosecutors

Rs 9,300-34,800

Rs 15,600-39,100

Director (Prosecution)

Rs15,600-39,100

Rs37,000-67,000

additional public prosecutors

Rs.5400

6600

chief prosecutor’s

–

7600

Conclusion

Law is a field of innumerable opportunities and the above-mentioned opportunities are a drop in the bucket. Law is the basis of all other institutions. Every now and then, law is evolving and with that new opportunities are also coming into existence. But lastly, there is only one question to ask, is it about money all the time? So, taking this into concern it is important to understand that every opportunity has its own worth. Money is “a thing” in the constituents of a happy life but it is not “the thing” when we talk of successful and satisfying life. So, just go for the opportunities and knock the door, keeping in mind that apart from money there are a lot of things that can be extracted out of that position.

References

[1]Vision Statement 2011-13 « The Bar Council of India, The Bar Council of India, http://www.barcouncilofindia.org/about/about-the-bar-council-of-india/vision-statement-2011-13/ (last visited Jul 3, 2017).

[2] India Lawyer Compensation,Report,https://www.vahura.com/docs/VahuraSampleCompensationReport.pdf

[4]Rebecca Furtado, Top 10 Law Firms That Pay The Highest Salary In India iPleaders (2017), https://blog.ipleaders.in/top-10-law-firms-that-pay-the-highest-salary-in-india/ (last visited Jul 3, 2017).

[6] Vivek Tripathi, Cyber Laws India Cyber Laws India, http://www.cyberlawsindia.net/ (last visited Jul 3, 2017).

[7] IndiaToday.in, From human rights to cyber law, five top lawyers on the intricacies of studying law. India Today (2016),http://indiatoday.intoday.in/story/the-business-of-law-human-rights-cyber-law-criminal-law-litigation-law-intellectual-property/1/565469.html (last visited Jul 3, 2017).

[11] Press Trust of India, Lawyers dominate Narendra Modi’s cabinet,The Indian Express (2014), http://indianexpress.com/article/india/india-others/lawyers-dominate-narendra-modis-cabinet-2-doctors/ (last visited Jul 3, 2017).

[12] Rukmini S., Government spends Rs. 2.7 lakh a month per MP, The Hindu (2016), http://www.thehindu.com/data/government-spends-rs-27-lakh-a-month-per-mp/article7699415.ece (last visited Jul 3, 2017).

[15] Pns, ‘Higher pay scales to different categories of prosecutors‘ The Pioneer (2015), http://www.dailypioneer.com/city/higher-pay-scales-to-different-categories-of-prosecutors.html (last visited Jul 3, 2017).

In this article, Ashwini Gehlot discusses the procedure for obtaining a Legal Heir Certificate.

Legal Heir Certificate

When the head of the family or a family member passes away then the next legal heir of that person can apply for the legal heir certificate.

This Certificate is generally required for the beneficiaries of a serving or retired employee, who passed away. If that retired person dies, family pension advantages will go to legitimate heirs. Generally, any levy to a man from government or nearby bodies will be paid to lawful heirs on the death of the individual. Such advantages to legitimate heirs might be a provident fund, pension, gratitude etc.

Legal Heir Certificate ordinarily specifies the names, ages, association with the deceased and conjugal status of all surviving family members. For getting Legal Heir Certificate, a death certificate indicating evidence of death is important. This death certificate is issued by the Major Panchayat/Municipality/Corporation/RO of Mandal where the death happened.

To know more about the how to obtain a legal heir certificate in brief, please refer to the video below:

Importance of Legal Heir Certificate

This certificate can be used for insurance claims, retirement benefit claims, pension claims and can also be used for gratuity and PF claims. Although this certificate is not legitimate in the property transfer matters where a person dies without a valid will, court litigation and also in cases of transactions with a financial institution or we can say money related establishments and banks etc. Because in these cases succession certificate (issued by civil courts by making an application) is required.

The legal heir certificate mainly used for acquiring the inheritance of the property which is left behind by the dead person.

Procedure for obtaining a Legal Heir Certificate

Eligibility

Husband/wife or son/daughter or mother of the deceased person can apply for legal heir certificate.

Instructions

Obtaining a legal heir certificate is very easy and not much of a trouble, it is issued by district tahsildar office for the person whose parent/husband/wife died intestate, it is issued to build a relationship for claims related to pension, insurance, administrative/service advantages, retirement benefits of the state and central government offices, government works etc. and to get occupation like compassionate appointments.

The person who is applying for legal heir certificate has to approach the district tahsildar office with the death certificate of the deceased and have to produce a form and also he/she have to make an application and the person has to fill up an application form and make sure that all the information provided by the person is correct and complete and it is also required that the person lodging the application should have all the required information and necessary documents required in the process and it is also required to affix a court fee stamp (INR 2) on the application form and SC/ST are exempted from this fee.

What documents to attach along with the application

Name of the deceased

Death certificate original

Service certificate issued by the head of the department/office in case of serving employee

Ration card and Aadhar card

Pensioner payment slip issued by the office of accountant general in case of pensioner

Family members names and relationship

Applicant’s signature

Date of application

Residential address

An affidavit worth Rs 20 on a stamp paper

click above

After filling the form and with all the necessary details and documents the form has to be submitted to Taluk’s Tahsildar. The person can obtain the legal heir from the Taluk/Tahsildar or district civil court of his/her area.

After the submission, an inquiry will take place for the verification by the local revenue officers as well as village administrative officials. Generally, a statement by the administrative/gov employee who is known to the dead person and his/her family will be registered in the application form. After the verification, the officials will submit their report in the prescribed form.

After the due inquiry, based on the report presented by the revenue officer and village administrative officials the certificate will be issued by the competent authority in which names of all the legal heirs will be mentioned.

Duration- the whole procedure from processing the information to the certificate issuance it will take around 15-30 days.

If the certificate is not issued within a reasonable period then the person concerned can remind the tahsildar and in a case of not getting any response the person can contact the concerned RDO/sub-collector.

Difference between Legal Heir Certificate and Succession Certificate

A lot of people get confused between succession certificate and legal heir certificate most of the times they consider them similar. But just to clarify this doubt here are some major differences mentioned below.

As it is known from this article that legal heir certificate is issued by the Tahsildar from taluka, the succession certificate is issued by the civil court or sometimes high court.

In legal heir certificate the person who can apply for the certificate is son/daughter, husband/wife or parents of the deceased but in the case of applying for succession certificate, only legal heir of deceased can apply.

The time required for issuance of legal heir certificate is 15-30days whereas in the case of succession certificate it can take 6 or sometimes 7 months in toto.

Fee for the issuance of legal heir certificate is Rs 2 for stamp and Rs 20 stamp paper for affidavit and sometimes additional fee like some officials can ask for money but it will be considered as unofficial and for succession certificate 3% or more or less percentage of the total value of property and as an additional fee attorney fee will be charged.

No one is allowed to contest in case of legal heir certificate application and process but in the case of succession certificate, anybody can contest this application within the 45 days from the time of the application being submitted.

Documents required for legal heir certificate is mentioned above and in the case of succession certificate, the important documents are death certificate of the deceased date, place and time of the death, names of all legal heir and their relation with deceased.

As mentioned above the importance of legal heir certificate that it is used for pension, gratuity, insurance, and PF claims and for retirement benefit claims and the succession certificate is used for transfer of possession/of property, is also used for paying debts or security on behalf of deceased or collecting debts or security on behalf of deceased.

Judicial pronouncements on issuance of legal heir certificate

As we know nothing in this universe is perfect, everything has their flaws so is this, there are chances of arising disputes regarding the issuance of this certificate sometimes it can be because of corruption or delay or may be fraud etc. so here are some of the case laws of Indian judiciary regarding this particular issue as mentioned below.

Periyaswamy vs Inspector, Vigilance And … on 23 March 1999[1]

In this case, the accused i.e. revenue officer asked for Rs. 300 as a bribe for sending the inquiry report which is used for the verification of issuance of legal heir certificate. So, in this case, the appellant has sentenced the imprisonment till the rising of the court and have to pay a fine of Rs 1000.

Petitioner’s husband was a Lineman working under the control of the second respondent and he died in harness and intestate on 1.12.2003. Petitioner made many representations to the second respondent for compassionate appointment within 1 year from the death of deceased but her request was rejected on the ground that petitioner is the second wife as per the certificate dated 20.01.2004 and so she is not entitled to the same. Petitioner filed a suit and the court declared her as the legally wedded wife after the judgment the petitioner approached the competent authority to cancel that certificate and issue a fresh certificate after that she approached the fourth respondent for the compassionate appointment, and again her request was rejected on the ground of delay.

Since the first representation made by petitioner was within 3 years of the death of deceased and since then she was continuously pursuing her case so the next representation made by her cannot be treated as a belated application. So, the court held that the representation made by petitioner was well in time i.e. within 3 years.

Vandana Bhimrao Jadhav vs Inhabitant Of Mumbai on 22 October 2013[3]

The respondent in this particular case had not disclosed the names of the other petitioner nos. 2 to 4 as the legal heirs of the deceased when he filed a petition for issuance of legal heirship certificate. So, the court in this matter held that the petitioners are entitled to include their names in the legal heirship certificate issued by this Court in Petition No. 91 of 2009 as legal heirs issued under section 2 of the Bombay Regulation VIII of 1827 in favor of the respondent.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

FEMA regulates all the foreign exchange related matters. The 1999 Act was enacted with a purpose of amending and consolidating all the foreign exchange related laws. So it would facilitate the Foreign Trade and be beneficial to the Indian Economy the 1991 Liberalisation, Privatisation and Globalisation policy could be a motivating factor behind the Government’s step to facilitate foreign trade. The Act deals with regulation and management of foreign exchange by dealing and holding foreign exchange and with export-import of goods and services and so on. It also sheds light upon authorized persons and their roles and also if the provisions of the act are not complied with then it also discusses the contraventions and penalties. It specifically also conveys the jurisdiction of specific court for the matters relating to foreign exchange that does not come under the jurisdiction of civil courts as mentioned under Sec. 34. There are 49 sections in the act it also discusses about the directorate of enforcement and other miscellaneous matters relating to the foreign exchange. [1]

Introduction to reporting requirements

Necessary information required by a governmental body, organization, or employer and is often required within a certain period of time and within a specific format that is known as reporting requirements.[2] Reporting requirements in simpler terms mean a set of facts or information needed for completion of a task in a specified period of time or format. Reporting requirements are very particularly fixated over a theme or topic. There are no specific provisions in FEMA[3] regarding reporting requirements in particular. The FEMA provisions do not directly address the requirements in the Act. There are different reporting requirements for different foreign exchange related matters.

Master directions issued by the RBI

The issue started from January, 2016 on different regulatory matters. [4]: The Master Directions consolidate instructions on rules and regulations framed by the Reserve Bank under various Acts including banking issues and foreign exchange transactions. The process of issuing Master Directions involves issuing one Master Direction for each subject matter covering all instructions on that subject.[5] The medium of press release or circulars are used keep the directions updated with the new changes that take place from time to time.

The master direction has been totally amended and includes different subjects like the Part I talks about the Remittance Facilities, Part II about Liberalized Remittance Scheme, Part III discusses the LO/BO/PO[6] related matters, Part IV about Foreign Investment, Part V about ECB(External Commercial Borrowing), Part VI about Non-resident foreign accounts, Part VII about immovable property, Part VIII about Overseas Direct Investment, Part IX about Trade, Part X about Guarantees and Part XI about the cell effective implementation of FEMA (CEFA)- Compounding. The amendments were made in the direction in the year 2016.[7]

Reporting requirements are specific under the following heads

Indian companies are allowed to access funds from abroad through the below-mentioned methods, (i) External Commercial Borrowings (ECB) (ii) Foreign Currency Convertible Bonds (FCCBs) (iii) Preference shares (iv) Foreign Currency Exchangeable Bonds (FCEBs)

ECB can be accessed under two routes, viz., (i) Automatic Route and (ii) Approval Route.[8]

Borrowings under ECB Framework are subject to reporting requirements in respect of the following

Loan Registration Number (LRN): Any draw-down in respect of an ECB as well as payment of any fees / charges for raising an ECB should happen only after obtaining the LRN from RBI.

Changes in terms and conditions of ECB: All the permitted changes in ECB parameters should be revised with form available at the earliest possible opportunity and it should under no circumstances exceed 7 days from the date of the changes

Reporting of actual transactions: The requirements relating to the borrowers is that they are required to report actual ECB transactions on monthly a basis within the time span of 7 days and the Part V of Master Directions – Reporting under Foreign Exchange Management Act discusses the format of it.

Reporting on account of conversion of ECB into equity: In a situation where partial or full conversion of ECB into equity is done, the reporting to the RBI will have different stipulations as given under the act.

Trade Credit transactions are subject to the following reporting requirements

Monthly reporting: As the name suggests the report is to be given to the authorities on the monthly basis. The Format of Form is available at Annex IV of Part V of Master Directions – Reporting under Foreign Exchange Management Act. Details like approvals, drawal, utilisation, and repayment of Trade Credit approved by all its branches, in a consolidated statement, during a month are required. Each trade credit may be given a unique identification number by the Authorized dealer bank.

Quarterly reporting: this report is to be submitted to the authorities on quarterly basis. Details like issuance of guarantees / Letters of Undertaking / Letter of Comfort by all its branches, in a consolidated statement, at quarterly intervals are required. It should reach to the authorized within the first ten days of the month. The format of this statement is available at Annex V of Part V of Master Directions – Reporting under Foreign Exchange Management Act.[9]

The establishment of BO (Branch Office)/LO (Liaison Office)/PO (Project Office) is subject to certain reporting requirements which are as follows:

The Annual Activity Certificate (AAC) (Annex I) as at the end of March 31 along with the audited financial statements including receipt and payment account are required to be submitted to the designated and authorized authorities before September 30 of every year. In case the annual accounts of the BO/LO are finalized with reference to a date other than March 31, the AAC along with the audited financial statements may be submitted within six months from the due date of the Balance Sheet to required authorities.

AD Category-I bank shall send a consolidated list of all the BOs/LOs/ POs opened and closed by them during a month (as per Annex II), by the fifth of the succeeding month.

Entities from Bangladesh, Sri Lanka, Afghanistan, Iran, China, Hong Kong, Macau or Pakistan which are setting up a BO/LO/PO in India should register with the state police authorities and are required to submit an annual report (as per Annex III) within five working days of the BO/LO/PO becoming functional to the Director General of Police (DGP) of the state concerned in which the BO/LO/PO has established its office; If there is more than one office of such a foreign entity, a separate annual report is required to be submitted to each of the DGP concerned of the state where the office has been established.

Limited liability partnership is subject to the following reporting requirements

Limited Liability Partnerships (LLPs) receiving amount of consideration for capital contribution and acquisition of profit shares is required to submit a report in Form Foreign Direct Investment-LLP through its Authorized Dealer Category – I bank, to the Regional Office of the Reserve Bank under whose jurisdiction the Registered Office of the Limited Liability Partnership making the declaration is situated, within 30 days from the date of receipt of the amount of consideration. The form should be accompanied by certain documents which would allot a Unique Identification Number (UIN). The LLPs should report disinvestment / transfer of capital contribution or profit share between a resident and a non-resident (or vice versa) under the time limit of 60 days from the date of receipt of funds in Form Foreign Direct Investment LLP. All LLPs in India which have received FDI and/or made FDI abroad in the previous year(s) as well as in the current year, should file the annual return on Foreign Liabilities by the 15 of July of every year. Since LLPs do not have 21- Digit CIN (Corporate Identity Number), they are advised to enter other set of digits. The RBI stipulates different formats and specifications which can be found on their official website.[10]

In conclusion we have these specifications as stipulated by the master directions given by the RBI with the FEMA’s authority involved in and they are to be followed by the investors and their non fulfillment may lead to fine or punishment both as stipulated by the act. Considering that our country had learned its lesson with the 200 year rule by the UK and was rather a little hesitant in allowing foreign trade but the circumstances have changed and now we have all the laws and regulations to keep the exchange and trade in control. Foreign investment in general terms a very long and hectic process considering the fulfillment of laws that are to be taken care of and the reporting requirements are just one of those laws or rather stipulation whose fulfillment is absolutely necessary for the smooth working and investing by the potential or current investors in our country.[11]

References

[1]http://lawmin.nic.in/ld/P-ACT/1999/The%20Foreign%20Exchange%20Management%20Act,%201999.pdf (Accessed on 30th March, 2017 at 6:58 PM).

[2] http://www.businessdictionary.com/definition/reporting-requirements.html. (Accessed on 30th March at 7:14 PM).

[10] https://rbidocs.rbi.org.in/rdocs/content/pdfs/13MDR291215.pdf (Accessed on 30th March, 2017 at 8:28 PM).

[11] The provisions mentioned in the article are not with an intention of plagiarism but they are the straight provisions as given under the act and cannot be changed by the author.

The regulatory regime with respect to foreign exchange is majorly governed by the Foreign Exchange Management Act, 1999 and the regulations; power under this Act has been derived from various entries in the Union List. In the earlier scenario, the foreign exchange in India was governed by the Foreign Exchange Regulation Act, 1973 (FERA). However, with the objective to consolidate and amend the foreign exchange related law for the facilitation of external trade and payments and to promote systematic development and maintenance of Forex market in India, the FERA was repealed by the new Act namely Foreign Exchange Management Act,1999. Moreover, the changed circumstances in relation to the foreign exchange market compelled the Government of India to repeal the above Act (FERA) and formulate the new Act, suiting to the requirements of the prevailing environment. The major aim of the Act is the promotion of exports and imports and brings in ease in the transactions pertaining to the external trade.

Under the earlier Act (FERA), it was required to take the permission of Reserve Bank of India either special or general regarding the various regulations as laid under the Act. However, a change has been observed under the new Act (FEMA) for which no permission is required to be taken from the RBI, except under the section 3 of the instant Act. There has been observed a transition from the phase of permissions to the regulations. This changed scenario is depicted in the Preamble of FEMA,1999 which states that the Act aims for consolidation and amendment of the law relating to the foreign exchange, keeping under consideration the following objectives- facilitation of the external trade and payments and promotion of the orderly development and maintenance of the foreign exchange market.

It was noticed that the approach pertaining to the dealing with the foreign exchange transactions underwent a change from the conservation of foreign exchange to the facilitation of trade and payments as well as the development of orderly Forex market. The section 5 of the Act facilitates the external trade by removing the restrictions on drawal of foreign exchange for undergoing the current account transactions as it provided for no need of seeking the permission of the RBI in the cases of the remittances involving external trade. The removal of the restrictions on the current account transactions was important as the notice was given to the International Monetary Fund (IMF) regarding the attainment of Article VIII status. However, the Central Government was given the power to impose restriction in consultation with the Reserve Bank of India for the purpose of securing interests of the public at large. The control on the exports is retained through Section 7.

As already mentioned, FEMA was enacted leading to the replacement of FERA due to the major reason that the latter became obsolete due to the changed scenario with respect to the foreign exchange. The Indian economy was facing the crisis situation in which the foreign exchange became the part and parcel for the survival of the country. There are 49 sections, of which 12 sections are operative in nature while the rest of the sections are contraventions, penalties, appeals, enforcement etc. The new Act (FEMA) has led to the reduction in the restrictions on the foreign exchange transactions relating to the trade in goods and services, with the exception of the power which has been provided to the Central Government to impose restrictions in the interest of the public.

Objectives and Extent of FEMA

As above mentioned, the broad objective of the new Act is to bring out the ease in the Foreign Exchange transactions. The Act is applicable to whole of the India, to the branches, agencies and offices outside India which is owned or controlled by a person resident in India and also covers any contravention committed under this Act by the person outside India. Therefore, this Act is extra-territorial as it applies to person even outside India if he/she falls under the ambit of this Act. Let us highlight the situations in which general permission of RBI is required for undergoing the transactions –

Dealing in or transferring any foreign exchange or security to any person not being an authorised person.

For the purpose of making any payment or for the credit of any person who is residing outside India in any manner.

Receiving from a person resident outside India any payment, not through an authorized person.

The current account transactions can be reasonably restricted as per the prescribed restrictions. The foreign exchange can be sold or drawn by any person to or from an authorized person for a Capital Account transaction.

The Reserve Bank of India may, specify after consulting with the Central Government, lay down the specifications regarding –

The permissible class or classes of Capital Account transactions.

The admissible limit up to which the foreign exchange shall be allowed for such transactions.

However, the restrictions can be imposed by the Reserve Bank of India on the withdrawal of foreign exchange for paying for the sums which are due on the account of authorization of loan or for investments which are direct in nature being made in the ordinary course of business.

The regulations can be imposed by the RBI, through the necessary restrictions or prohibitions in on the following matters –

The person to whom any transfer or issue of any foreign security is made who is a resident outside India.

The person to whom any transfer or issue of any foreign security is made who is a resident in India.

The transfer or issue of any foreign security by any branch, office or agency in India of a person resident outside India.

The borrowing or lending of foreign exchange in any orm or with any name.

The borrowing or lending in rupees between a person resident outside India and person resident inside India in whatever form or by whatever name called.

Any form of the deposits between a person resident inside India and a person resident outside India.

Currency or currency notes if they are exported, imported or are being held.

If the person resident in India transfers any immovable property outside India, other than lease not exceeding five years.

If the person resident outside India acquires or transfers any immovable property in India, other than the lease not exceeding five years.

When any guarantee or surety is provided with respect to any debt or any other liability incurred by a person who is a resident of India and who owes to a person who is resident outside India or by a person resident outside India.

Any transfer of or investment in the foreign currency or security can be made by a person, resident in India who may hold or own the immovable property when such a property is situated outside India when he was residing outside India or he inherited the property from the person residing outside India. Any investment can be made in the Indian currency in immovable property or Indian currency or security which is held, owned or transferred by any person resident outside India in case when such currency, security or property was acquired, held or owed by such a person when he was a resident in India or is inherited from a person who was a resident in India.

Any regulation can be passed by the RBI for the purpose of prohibiting, or regulating the establishment in India of a branch, office or other place of business by a person resident outside India, for undergoing any activity relating to such a branch, office or other place of business. The person who exports goods or services must comply to the following requirements –

He must provide a declaration as per the prescribed form to the RBI or any authority. Such a declaration must contain true and correct particulars, the amount representing the full export value must be included or if such a value cannot be ascertained, the value can be decided by the exporter who may decide considering the prevailing market conditions, who expects will receive the amount on the sale of goods in the market.

He must also furnish any such information as may be required by the RBI for ensuring the realization of the export proceeds by such exporter.

The RBI may give the direction to any exporter to comply with the requirements as it deems with for the purpose of ensuring the full export value or the value as determined by RBI, according to the market conditions. The RBI may also lay down the specifications in the case when any foreign exchange is due or has accrued to any person resident in India where the person will have to take all the reasonable steps to realize and repatriate to India such foreign exchange with the period prescribed. The RBI plays a very important role in managing the transactions with respect to foreign exchange in India.

In this article, Shishira Prakash who is currently pursuing Diploma in Entrepreneurship Administration and Business Law from NUJS, Kolkata, discusses what is a qualified institutional buyer and how are qualified institutional buyers regulated?

Qualified Institutional Buyers (QIB)

Investment in today’ world is made in several different methods. People invest in real estate, gold bonds, debentures, providential funds, fixed deposits, investing in companies through shares and stock and much more. Investing in an Indian company or a foreign company is one of the most common ways used. These investments are made by many kinds of investors in India who are governed by specified sets of rules and regulations in the form of statues like Companies Act, 2013, Company Act rules, and the Securities and Exchange Board of India rules. Due to some difficulties, individuals tend to invest indirectly through investment institutions instead of investing by themselves.

These investing institutions are mainly a collective group of people in who come together and collect the investible amount from various investors and invest them in the investment market.

Even though individuals have limited control when they use these indirect methods to invest, they have an expert handling and recommending the investment which should be made in order to get high returns. These institutional purchasers of securities are deemed financially sophisticated and are legally recognised by exchange boards to need less protection from the issuing companies than most public investors who invest directly.

Definition of Qualified Institutional Buyer

These groups of investors who follow certain regulations and rules formulated by the SEBI are collectively qualified to be known as “Qualified Institutional Buyer” (QIB). SEBI has defined a Qualified Institutional Buyer as follows:

Qualified Institutional Buyers are those institutional investors who are generally perceived to possess expertise and the financial muscle to evaluate and invest in the capital markets. In terms of clause 2.2.2B (v) of DIP Guidelines, a ‘Qualified Institutional Buyer’ shall mean:

Scheduled commercial banks;

Mutual funds;

Foreign institutional investor registered with SEBI;

Multilateral and bilateral development financial institutions;

Venture capital funds registered with SEBI.

Foreign Venture capital investors registered with SEBI.

State Industrial Development Corporations.

Insurance Companies registered with the Insurance Regulatory and Development Authority (IRDA).

Provident Funds with minimum corpus of Rs.25 crores

Pension Funds with minimum corpus of Rs. 25 crores

Public financial institution as defined in Companies Act, 2013;

Regulations

The institutions which fall under any of the above mentioned categories are qualified to be a QIB in India.

SEBI through Guidelines for “Qualified Institutions Placement”- Amendments to SEBI (Disclosure and Investor Protection) Guidelines, 2000 introduced additional mode for listed companies to raise funds from domestic markets in the form of Qualifies Institutions Placement.

The listed companies which are eligible to raise funds in domestic market by placing securities with QIBs are those whose equity shares are listed on a stock exchange nationwide and which are complying with the prescribed regulations of minimum public shareholding of the listed agreements. These guidelines are applicable to any kind of securities in the form of equity shares or any other form of securities other than warrants, which can be converted into or exchanged with equity shares at a later date at any time after allotment of security (but, within six months from the date of allotment). These kinds of shares are referred to as “specified securities” and are fully paid up when they are allotted.

The guidelines are also very specific regarding who can be the investors or allottees to these specified securities. It specifically mentions that they can be issued only to QIBs and such QIBs cannot be promoters or related to promoters of the issuer directly or indirectly. Each and every placement is done to the qualified institutional buyers will be on private placement basis.

The SEBI has also prescribed that the aggregate amount raised through QIBs by an issuers in a financial year cannot exceed five times of the net worth of the issuer at the end of its previous financial year. Regulating the pricing of the specified securities, the guidelines provide that the floor price of these securities shall be determined in a similar manner of that of the GDR/ FCCB issues and shall be subject to adjustment in cases of corporate actions such as bonus issue or the pre-emptive right given to the already existing shareholders of the issuer.

In every placement it is a mandate to allot 10% of the securities to Mutual Funds. It is also mandatory in each and every placement to have at least two allottees for an issue of size up to Rupees two fifty crores and at least five when it exceeds the above specified amount. Further, the issuer is also not allowed to allot more that 50 % of the issue size to a single allottee. Another important provision in favour of the issuer and against the investors is that the investors cannot and are not allowed to withdraw their bids or applications after closure of the issue.

All the Qualified Institutional Placements are taken care of and managed by the merchant brokers who are registered with SEBI. They shall exercise due diligence and furnish and submit a due diligence certificate to Stock Exchange Board informing them that the issue is with compliance with all the provisions and requirements given and mentioned by the SEBI.

Between each placement in case of multiple placements of these kinds of specified securities, there shall be a minimum gap of six months between them. In order to obtain in-principle approval and final permission from the Stock Exchange for the listing of these specified securities the Issuers and Merchant Broker shall submit reports, documents and undertakings, if any as prescribed in this regard in the listing agreement. But, on the other hand it is not mandatory to file any offer document or notice to the Exchange board in case of preferential allotment and QIP. The issuing companies are further allowed to offer a discount of up to 5% on the prices of the QIPs, but this discount can be offered only subject to the shareholders’ approval.

Conclusion

The Securities and Exchange Board of India introduced the concept of Qualified Institutional Buyer at the time when Indian corporates were looking for chances to enter into foreign investments overseas to expand their operations, mainly due to two reasons; one, easy availability of funds in those jurisdictions and two, less stringent regulatory environment compared to India.

This concept has become a common route for raising capital due to a twofold reasoning. Firstly, it is advantageous for the issuing company as one, the amount of time taken to complete a QIP is much more less than through public shareholder as there is no long wait for document approvals by SEBI and the whole process can be completed in a span of 4 to 5 days and two, it is cost effective as there is no need to employ a large team of bankers, solicitors, advocates and auditors to obtain approvals. Secondly, the Qualified Institutional Buyers have the ability and opportunity to buy large stakes in company with the advantage of being able to exit and sell their stocks at any point of time post its listing on the exchange unlike waiting for a minimum period of one years when it is investing in an IPO.

Although due to the above mentioned reasons, companies prefer QIP, there are a few negative sides to it too. As QIPs give the Institutional Buyers an opportunity to hold a large stake in the company, it dilutes the existing stakes of the shareholders. Due to this, the companies with a huge amount of promoter holding prefer this method over the companies in which there are significant number of promoters with low stakes, as a further dilution of stakes could mean risking the management control of the company.

So it’s a kind of bootstrap where, while coming over from a particularly problematic situation company enters another possible problematic condition.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

SME (Small and medium size enterprises) exchange is a platform made by the BSE (Bombay Stock Exchange) in 2012. It has been made by the initiative of the Indian Government along with SEBI. It is a phenomenal framework for the entrepreneurs. It is a popular concept worldwide.

Problems faced by the small and medium enterprises.

There are various problems faced by the small and medium sized enterprises. These are the enterprise which brings in so much of employment all over the country. They add to the national income of our country to a large extent. After Agriculture in our country, SMEs have their place since they have less capital investment. They have a huge role in the export of our country. Also they are diverse in their nature as they are present and contribute to so many sectors of our country including technology, agriculture, clothes, food etc. In spite of so many achievements they have had, there are present a lot of problems due to which the concept of SME exchange has come into play. What are they?

One major problem is capital. There are two ways of raising capital. Either borrowing from bank or funds from promoter. Banking funds are the most common. But for a startup company to bear the cost of that is very risky. If and when the company is doing well, bearing that cost might become easy. But it is not the case initially.

Another big factor is the kind of technology . It is quite obvious that the SMEs would not get hold of the kind of technology that is modern and more efficient because there is always a dearth of capital.

Lack of fund also comes from the fact that large companies do not lend to the SMEs easily.

There are other several problems that have led to the concept of an exchange for these enterprises.

CRITERIA

There are a few criteria for getting a company listed on an SME exchange. They are-

The net worth of the particular company wanting to get listed has to be of one crore minimum. Net worth is the calculation of asset minus liability.

The tangible assets of the particular company has to be one crore minimum. Intangible assets do not count when it comes to getting listed here.

The company in question has to be in operation for more than three years. A single day less than three years would make it unfit for listing.There has to be a profit history of the company for at least 2 years.

When it comes to profit history, no extraordinary income would be counted. The only income that had arisen from regular sources and only distributed profit would be counted.

The particular company at the time of listing should not have been involved in any pending suit.

There has to be compulsory market making for three years.

It has to be a full-time company.

Small and rapidly growing companies should get listed to an SME exchange. The major problem of SMEs being fund, listing is advantageous in several ways.

Firstly, Venture and Angel investment can invest in an SME if it is listed in the exchange. When listing happens, it leads to raising funds automatically.

Secondly, It is very easy and a convenient way of listing. Very contrary to what people generally think that it would be very complex and cumbersome method to the listing and therefore they drop the idea. But surprisingly enough it takes only three months for the plan to get executed, the company to get listed.

Thirdly, In case of listing, a company’s shares gives rise to more shares and hence more money. How does this happen? When a company lists itself, its shares are also listed. And it can use its existing shares to borrow further shares. Also not always money is required. For example, When a company is listed, and the shares of the company goes up, the shares can be used to buy other companies too simply by giving off those shares. No money is required for this. It is like creating one’s own currency. Currency of shares and not the currency created by the government.

Fourthly, Listing a particular company on an SME exchange basically opens up a huge market for that particular company which would not have happened if it had not been listed on the exchange. This happens in the manner that when a company is listed, it gets a lot of exposure . Channels start talking about them and their names comes up in front of people. They get noticed . Newspapers might also mention the name of the company since it is a part of the exchange and that way also popularity or acknowledgement is gained. This is profitable in a few ways. One is the company getting the mention or if it can be called as limelight inturn gets a lot of prestige and respect. This is a very important aspect for a small scale company which would have gone absolutely unnoticed and given no importance had it not been listed. But on being listed it gets respect that people thought only large companies with huge turnovers could have got only. But a small company getting the importance at an early stage brings about immense advantage to it.

Fifthly, continuing from the previous point, the free market that gets created for the company that has been listed leads to vendors and customers, etc coming to the company themselves for working with them. The company did not have to go about searching them everywhere trying to hire them. But they get to notice themselves and a gateway is opened where they come and approach the company themselves.

Sixthly, succession is a tricky affair and can bring about huge confusions and complications and might even at times lead to courts. For a company that has been already listed, it is not that difficult for inheritance, say when the owner dies or the property has to go through a devolution . The sharing of the company interms of succession can be simply done through giving off the shares of the company. It is that simple. There is no need for going through a tricky pathway as when we say the word succession it always makes us think that it might be something extremely confusing and cumbersome.

Seventhly, usually, there are people who are under the impression that when they have started a company of their own it is theirs and there is no good reason for giving it away to someone or something or any sort of platform. But this is not a very practical method of thinking. If a company wants capitals, wants to go far in terms of profits in the long run, wants to make the company larger and larger, then listing needs to be done. Since a small company cannot by magic gain a lot of money and makes its company huge overnight. Or not even in days and years for that matter. A small company has basically nothing apart from an idea, determination , creative thinking, skill etc.

For it to overcome all the odds and rise up especially in a time where there are so many large companies which have such huge turnovers and what not. It is very hard and extremely competitive for small companies since they need to have something to think of competing with the large ones. Forget about winning the competition, they are not even capable of competing. And that is because of very practical reasons.

To establish itself in such a competitive world they have to look for a platform, a base from where they can think of looking higher and farther. In case of listing themselves, wealth can be created out of very little that these companies have. And listing in an exchange does not in any way mean that the particular company wanting to list itself in an exchange is giving away its company to somebody or to a certain place. 75% of the company’s shares is kept with the company itself and 25% goes to the board.

Eighthly, it is very difficult for a small company to find skilled people and hire them. Most times it can be seen that the entrepreneur himself, who has started with the idea does everything on his own. He takes the place of a partner, PR, directors, and is also the one working in every sphere and sector of the company. This is an impractical; way of dealing with a company if the owner actually has dreamt of making his company really big. What listing does is it gives a lot of advantage to the companies who are a part of the exchange. A company gets hold of people who are willing to be partners to the company or go for other posts in the company. This way the company gets a lot of people for its various fileds very easily only which would otherwise have been very difficult.

Ninethly, Another huge advantage of listing a company would certainly be the amount of tax benefits the company would get. So much of tax benefit with basically nothing in return but instead getting hold of a lot of capital and making the company grow to its potential.

In this article, Ritika Sardar who is currently pursuing Diploma in Entrepreneurship Administration and Business Law from NUJS, Kolkata, discusses the restrictions on transferability of shares.

Abstract

The objective of this essay is to provide a thorough analysis of the restrictions and limitations imposed on the transfer of shares. The assignment begins with an introductory overview of the concept of restriction over free transfer of shares, delving into the rationale behind the same. The difference between the applicability of the concept in public and private companies is introduced in this section of the paper.

This is followed by a detailed analysis of the operation of the restrictions in private and public companies, along with relevant statutory provisions and case laws. In the conclusion to the essay, I have provided my own views on the topic along with an overall evaluation of the same.

Restriction of share transfer and logic thereof

Restriction on transferability of shares is one of the flagship points of a private company; a company, in order to exist as a private company, has to provide for such restrictions as it deems fit by way of its Articles of Association (hereinafter referred to as “AoA”), which is one of the three constitutional documents of a company [the other two being the Memorandum of Association (hereinafter called “MoA”) and Certificate of Incorporation (hereinafter called “CoI”)]. The AoA is a document that specifies the regulations for a company’s operations, and they define the company’s purpose and lay out how tasks are to be accomplished within the organisation. This set of rules can be considered a user’s manual for the company because they outline the methodology for accomplishing the day-to-day tasks that must be completed.[1]

This has been statutorily codified in the definition of a private company as per Section 2(68)(i) of the Companies Act, 2013 (hereinafter referred to as the “2013 Act”) which provides that a private company is one which by way of its Articles, restricts the rights to transfer its shares.[2] The intention behind a private company is two-fold: Firstly, to facilitate the business and trade carried on by a small, close-knit group of members by allowing them to avail the benefits of corporate trading and corporate form of business. The structuring of a company affords many benefits as compared to a partnership and also reduces the liability of each member by providing for separation of business from the individual. Secondly, private companies are preferred to public companies because of the sheer volume of corporate filings to be made and requirements to be adhered to by a public company.[3]

The restrictions on transfer of shares in private companies flow from the Partnership Principle, which is the soul and basis of private companies. These restrictions, as stated above, are considered essential in a private company which is usually a group of trading persons bound together by close ties of kinship and/or friendship. These close associations cannot be established with anyone and everyone so easily and therefore, these members seek to keep the shares of such a company within the group. This motivates them to impose various restrictions to thwart the admission of members who may be unfavourable or hostile to the existing members and thereby to check the dilution of control over the company by the current members. These restrictions on transfer of shares help to keep the ‘soul and basis’ of the company intact. The rationale behind these restrictions in a private company has been endorsed by the Courts repeatedly and therefore they have acted as guardians of private companies, enabling them to retain a large degree of control over whom they admit as members.[4]

However, a completely different scenario plays out and prevails in public companies. One of the main reasons for investment in public companies is the free transferability of shares of such companies; there are no restrictions and anyone who follows the laws regulating share transfer can purchase shares of such a company. The shares of a public limited company are highly liquid and pose no impediments for a holder looking to sell them. This principle has been enshrined in Section 58(2) of the 2013 Act[5] which provides that shares and interests of a public company shall be freely transferable. This is one of the key identifying attributes of a public limited company in India.[6]

Thus, as can be seen from above, based on the motive behind the form of organisation and purpose to be fulfilled, the treatment of restrictions on share transferability differs; while it is sine qua non for a private company, the opposite (it is prohibited) is followed in a public company.

Restriction in transferability of shares vis-a-vis Private and Public Companies

Despite what is said above and at the risk of repetition, it is necessary to point out that the restrictions on transferability of shares of a company or lack thereof are almost entirely dependent on whether the company is a public or a private one. This having been said, various interpretations have been rendered by the Courts as to what is and isn’t permissible by way of a restriction and also whether in a public company, shareholders are absolutely prohibited from dealing with their own shares as they please. These facets of the concept have been elaborately dealt with below:

Share transferability restriction in Private Companies

As stated above, it is essential for a company seeking to be a private company to impose these restrictions; it is one of the defining features of a private company. Restriction on transfer of shares in private companies mainly takes two forms: right of pre-emption in favour of other members and powers of the Board of Directors (hereinafter referred to as “BoD”) to refuse to register the transfer of shares.[7]

Right of Pre-Emption

Pre-emption rights are usually such as ‘right of first offer’ and ‘right of first refusal’. The restriction basically embodies the principle that if a shareholder of a private company wishes to sell some shares, the existing shareholders have a right to be offered these shares first and on their refusal or failure to act within the given time, the shares can be sold to a third party. The motive behind this restriction is to prevent dilution of the promoter and other major shareholders’ stake in the company. This right of pre-emption is usually provided in shareholders’ agreements entered into between the various stakeholders in the company.

The procedure to be followed in such situations is as follows: the transferor gives a notice in writing to the company of his intention to sell his shares, which is forwarded to other members of the company along with the time limit for them to respond. The price of these shares is determined by the company’s directors or auditors. Normally, provisions for this are contained in the company’s AoA. On the failure of the other shareholders to respond within the stipulated time, the transferor is free to sell the shares to a third party.[8]

Click Above

Powers of BoD to refuse to register transfer

The Articles of a private company commonly vest the BoD with discretion regarding the acceptance of a transfer of shares. This power vested in the Board is fiduciary in nature i.e., it must be employed in good faith and for the benefit of the company and not for some inappropriate purpose.[9] As per Section 58 of the 2013 Act, the BoD shall communicate the refusal within 30 days from the date on which the instrument of transfer, or the intimation of such transmission, as the case may be, was delivered to the company and shall assign reasons for such refusal. This refusal can be appealed against to the National Company Law Tribunal (hereinafter referred to as “NCLT”) which shall pass such orders as it deems fit. [10] Several judgements have been pronounced regarding the scope of the Company Law Board (the predecessor of the NCLT and hereinafter referred to as “CLB”) to hear appeals against refusal to register transfer under Section 111 of the Companies Act, 1956 (this Section corresponds to Section 58 under the 2013 Act).

For example, In Harinagar Sugar Mills v. Shyam Sunder Jhunjhunwala and Ors.[11]the Supreme Court stated that while exercising its appellate jurisdiction under Section 111, the CLB has to decide whether in exercising their power the directors are acting, oppressively, capriciously, or corruptly or in some way mala fide.[12] Another ground on which the NCLT can exercise its jurisdiction is when it finds that the BoD has exercised its power of refusal based on irrelevant considerations, grounds which are not specified in the Articles. Following the reasoning of Lord Greene MR in ReSmith and Fawcett Ltd.[13], the High Court of Calcutta in Master Silk Mills (P) Ltd v. D.H. Mehta[14], held that the BoD’s refusal to accept a transfer in favour of another company whereas the Articles empowered them to exclude only undesirable persons, was beyond their authority. The Court held that such a blanket ban on admission of other companies as a shareholder was beyond the authority vested in the board by the Articles.[15]

Case Laws Relating to Restriction in Private Companies

Because the 2013 Act (like the 1956 Act) is silent on the issue, several judgements have been rendered over the years in order to lay down the law regarding the type and extent of restrictions that can be placed in the AoA. The pivotal position of law is laid down in the case of V B Rangaraj v. V B Gopalakrishnan and Others.[16]. On the question of whether shareholders can, amongst themselves, enter into an agreement which is contrary to or inconsistent with the Articles of association of the company, the Supreme Court of India held, that only restrictions laid down in the Articles of the company are permissible. A restriction which is not specified in the Articles is therefore not binding either on the company or on the shareholders.[17]

It is interesting to note that the Principal Bench of theCLB has pronounced that even though a private company, being a subsidiary of a public company is defined as a public company in the 1956 Act, all the provisions in the Articles of association to maintain the basic characteristics of a private company in terms of Section 3(1)(iii) will continue to govern the affairs of such a company. One of the basic characteristics of a private company in terms of that section is the restriction on the right to transfer the shares and the same will apply even if a private company is a subsidiary of a public company.[18]

The restrictions on transferability, so essential to the character of a public company, are however not to be construed as a ban or a prohibition on the transfer of shares. The Courts have consistently held that the restriction upon transfer means any restriction that will give some control to the company over transferability of shares. It was held in Chiranji Lal Jasrasaria and Anr. v. Mahabir Dhelia and Ors.[19] that a restriction which amounts to a prohibition on transfer of shares or which precludes a shareholder altogether from transferring is invalid. Moreover, a prohibition on the transfer of shares will amount to violation of Section 82[20] (which corresponds to Section 44 of the 2013 Act) of the 1956 Act and Section 6[21] of the Transfer of Property Act, 1882.[22]

Based on the above observations made and decisions rendered by judicial authorities, the following principles may be discerned regarding restrictions on transfer of shares in private companies:

The right to transfer is subject to restriction contained in the Articles; in case of two possible interpretations of the restrictions, the one that is less restrictive should be adopted.

The power to refuse the transfer of shares cannot be exercised arbitrarily or for any other collateral purpose and can only be exercised for a bonafide reason in the interest of the company and the general interest of the shareholders.

While there may be restrictions on the transferability of the shares, there cannot be an absolute prohibition on the right to transfer of shares.[23]

Scenario prevalent in Public Companies

Though shares of a public company are widely accepted to be freely transferable, the question of whether this means that shareholders of such a company are absolutely prohibited from dealing with their movable property (as per Section 44 of the 2013 Act) as per their wishes, is frequently posed. The question of whether transfer restrictions imposed by agreement on shares of a listed company are enforceable has been a vexed one. Numerous decisions of the Supreme Court as well as High Courts had expressed somewhat different views on the nuances of the issue. However, some stability was brought about in 2010 by a decision of a division bench of the Bombay High Court in Messer Holdings v. Shyam Madanmohan Ruiaand Ors[24]., which effectively ruled that restrictions expressed in an agreement between shareholders do not violate of the 1956 Act and that they can be enforced inter se among shareholders. In doing so, the Court diverged from the ruling of a single judge in Western Maharashtra Development Corpn. Ltd. v. Bajaj Auto Limited,[25] wherein a pre-emption clause in a shareholders’ agreement was held to be in violation of Section 111A[26] of the 1956 Act.[27]

The division bench held,

“The concept of free transferability of shares of a public company is not affected in any manner if the shareholder expresses his willingness to sell the shares held by him to another party with right of first purchase (preemption) at the prevailing market price at the relevant time. So long as the member agrees to pay such prevailing market price and abides by other stipulations in the Act, Rules and Articles of Association there can be no violation. The fact that shares of public company can be subscribed and there is no prohibition for invitation to the public to subscribe to shares, unlike in the case of private company, does not whittle down the right of the shareholder of a public company to arrive at consensual agreement which is otherwise in conformity with the extant regulations and the governing laws. That means that it is open to the shareholders to enter into consensual agreements which are not in conflict with the Articles of Association, the Act and the Rules, in relation to the specific shares held by them; and such agreement can be enforced like any other agreement. That does not impede the free transferability of shares at all.”[28]

This has now been codified and statutorily provided in the proviso to sub-Section (2) of Section 58 of the 2013 Act which provides that any contract or arrangement between two or more persons in respect of transfer of securities shall be enforceable as a contract.

Conclusion

Given the rationale behind the establishment of a private company, the restrictions imposed on the transfer of shares seem reasonable, especially considering that the proposed transferee has an option to move the Tribunal in case the BoD appears to have exercised its powers of refusal capriciously or in a mala fide manner. These restrictions help maintain the sanctity of the private company and help the founders/promoters retain majority control and thereby steer the company in the desired direction.

With respect to a public company, keeping in mind that the shares belonging to a person are his movable property and can be transferred in accordance with Section 6 of Transfer of Property Act, 1882, the Court has tried to strike a balance between the conflicting principles of this aforementioned ownership and the free transferability of shares that characterises a public company and provides liquidity to its stock. As a result of the effort, the Court correctly ruled that as long as the agreement to transfer complies with the AoA of the Company and relevant statutory provisions governing the transfer, shareholders of a public company are free to deal with their shares as they please and can enforce an agreement for such transfer.

In my humble opinion, the kinds of restrictions imposed and liberties granted for each kind of company are befitting to them and will enable them to achieve their respective goals.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Timely and adequate access to capital is imperative for the growth of any business. The stock markets serve as an important nexus between investors with surplus funds and companies requiring capital. It has always been an aspiration for entrepreneurs, promoters and venture capital backed companies is to access the capital markets through an Initial Public Offer (“IPO”).

Apart from the distinct advantage of being able to tap large pools of capital from retail and institutional investors at the desired valuation, an IPO provides greater recognition to a company, unlocks greater value for its shareholders and employees holding stock options by providing much needed liquidity and require such company to adopt stringent corporate governance practices due to enhanced regulatory intervention.

Alternatives available to listed companies for raising capital

A publicly listed company may need to tap the capital markets more than once in order to meet its business objectives, after its initial capital raised through an IPO is dried up. The Companies Act, 2013 along with the rules framed there under (“Act”) and the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009 (“ICDR”) are the principal laws governing issue of capital by Indian companies. Under the Act and ICDR, the following options are available to a listed company for raising subsequent capital:

Issuance of securities to its existing shareholders by way of Rights Issue.

Making a Follow on Public Offer (“FPO”) (think of it as IPO 2.0).

Preferential Issue of securities to a select group of investors, including its promoters.

Making a Qualified Institutional Placement (“QIP”) to a select group of investors known as Qualified Institutional Buyers (“QIB”).

While an FPO or a Rights Issue may seem lucrative, the process for either of the alternatives is almost as time and effort consuming as it is in case of an IPO, requiring months of planning, stringent compliances, enhanced disclosures and incurrence of significant costs. Such stringent requirements primarily exist to prevent any wrongdoings by companies and promoters since public money is getting tapped. Thus, a Rights Issue or an FPO may not be a viable option for a company which is in immediate need of long term capital. In such a case a Preferential Issue to a select group of individual or institutional investors or a QIP to a QIB is the most viable option. Both the aforesaid options are cost and time effective and have proved to be a significant tool for companies wanting to attract private capital.

A Preferential Issue is an issue of specified securities by a listed company issuer to any select person or group of persons on a private placement basis, in terms of Chapter VII of the ICDR. In a Preferential Issue, securities are allotted only to a pre-defined set of investors or existing promoters of a company, subject to the applicable requirements as regards pricing, disclosures and lock-in. A QIP can be considered as a special case of a Preferential Issue where eligible securities are allotted only to QIBs. In contrast to a Preferential Issue, shares issued under a QIP are not subject to a lock-in, can be issued at an attractive price taking into consideration only the most recent price implications and involve comparatively less disclosures to be made.

What is a Qualified Institutional Placement?

The Securities and Exchange Board of India (“SEBI”) issued a circular on May 8, 2006 under the erstwhile SEBI (Disclosure and Investor Protection Guidelines) 2000, allowing listed companies to raise private capital domestically by way of QIPs. Prior to this juncture, Indian companies used to excessively depend on foreign capital by issuing securities such as American Depository Receipts and Global Depository Receipts, which led to an undesirable export of domestic equity capital markets, which was a major concern for SEBI.

A QIP issuance involves allotment of eligible securities being equity shares, non-convertible debt instruments along with warrants and convertible securities other than warrants by a listed company, to Qualified Institutional Buyers, on private placement basis. In addition to the provisions applicable to companies raising capital under the Act, QIP issuances by listed companies are governed by the provisions of Chapter VIII of ICDR. Unlike an IPO or an FPO, only QIBs can participate in a QIP issuance. The main premise behind a QIP issuance is that it’s relatively easy for a company to convince a clutch of big ticket investors for raising money than to convince the entire public at large in case of an IPO or an FPO, thus resulting in time, cost and process efficiencies.

Who is a Qualified Institutional Buyer?

The term QIB is defined under Regulation 2(1)(zd) of the ICDR which, inter alia, include mutual funds, Foreign Institutional Investors, insurance companies, scheduled commercial banks, multilateral and bilateral financial institutions, pension funds and provident funds with minimum corpus of Rs. 25 crore, public financial institutions and others. QIBs exclude promoters and persons belonging to the promoter group. Thus, it can be seen that QIBs are mainly large institutions who are well informed and sophisticated players in the stock markets, requiring relatively less protection from SEBI as compared to the average retail investor. Since these investors are capable to making well informed decisions and generally perform their own due-diligence, it seems logical to subject QIPs to less stringent regulations, making it a speedy process for issuer companies.

What are the conditions for a Qualified Institutional Placement?

Special Resolution by shareholder

A listed company is required to obtain prior approval of its shareholders by way of special resolution for making a QIP. The QIP has to be completed within a period of 12 months from the date of passing the aforesaid special resolution. An issuer cannot make a QIP until the next six months, once a QIP issuance is completed.

The class of securities for which QIP is proposed should be listed with a recognized stock exchange for a period of at least one year prior to sending the notice of the extra-ordinary general meeting where the approval of the shareholders is being sought. Further, the issuer should be in compliance with the requirement of minimum public shareholding stipulated by SEBI which is currently 25%. It may be pertinent to note that companies which had not met the minimum public shareholding criteria in the past were not allowed to increase their public shareholding by way of a QIP and had to opt for Preferential Allotment, until the introduction of Institutional Placement Programme by SEBI.

Appointment of a Merchant Banker

An issuer is further required to appoint a SEBI registered Merchant Banker to manage the issue and carry out due diligence. The Merchant Banker is responsible for seeking in-principle approval for listing of the eligible securities to be issued under QIP and furnishing a due diligence certificate to the stock exchanges stating that the QIP issuance confirms to the requirements stated under Chapter VII of the ICDR.

Filing a Placement Document