This article has been written by Pruthvi Ramakanta Hegde. In this article, the author covers the difference between general and particular lien with relevant examples. Also, the meaning of each type of lien and judicial approach with regards to it is also discussed.

Table of Contents

Introduction

In any financial transaction, securing the party’s interest is one of the important aspects. It becomes even more important when a loan is advanced and there might be a risk of non-payment. In such circumstances, there are certain remedies available under the law. One of the remedies is the concept of “lien”. The risk of non payment and non performance of the duties can be reduced by this concept.

In the concept of lien, a person or entity has the right to retain possession of another’s property. This right continues until the debt or obligation is fully satisfied. The concept of lien is governed as per the provisions of the Transfer of the Property Act, 1882(hereinafter referred to as ‘TP Act’) and the Indian Contract Act, 1872. The lien is divided into two types that includes general and particular lien. Both kinds of the lien aim to protect and secure the payment and performance of specific obligations. However, they are different in their scope, application and rights they confer on the creditor.

Before discussing the difference between general lien and particular lien, let’s first understand the meaning of lien.

Meaning of lien

The term lien is not defined under the Indian law. However, we all know that many enactments have discussed the concept of lien. One such enactment is the Indian Contract Act 1872, and the Sale of the Goods Act, 1930. In general terms we can say that a lien means keeping the possession of the property of the person until the loan owed by such person is cleared.

In other words, a lien is a legal claim on property or assets that acts as security for a debt. Accordingly, the person who lent the money, or someone with a legal decision (such as a court-appointed receiver), has a right to hold or take the asset until the debt is repaid.

Main purpose of a lien

One can simply state that the main purpose of a lien is to ensure the loan or obligation is fulfilled.

For instance, when a person takes out a mortgage to buy a house, the bank or lender places a lien on the property. The lender has a legal claim to the house as collateral for the loan. If the borrower fails to repay the mortgage, the lender can enforce the lien by foreclosing on the property and selling it to recover the loan amount.

According to Cambridge Dictionary, lien means holding the property belonging to others until they have fully paid the debt amount which they owe. Generally lien is divided into two types as per the Contract Act. They are general and particular lien. These types of lien are recognised under Section 171 and Section 170 of the Indian Contract Act, 1872 respectively.

Let’s now move forward and discuss the key distinctions between general and particular lien.

Differences between general lien and particular lien

Meaning

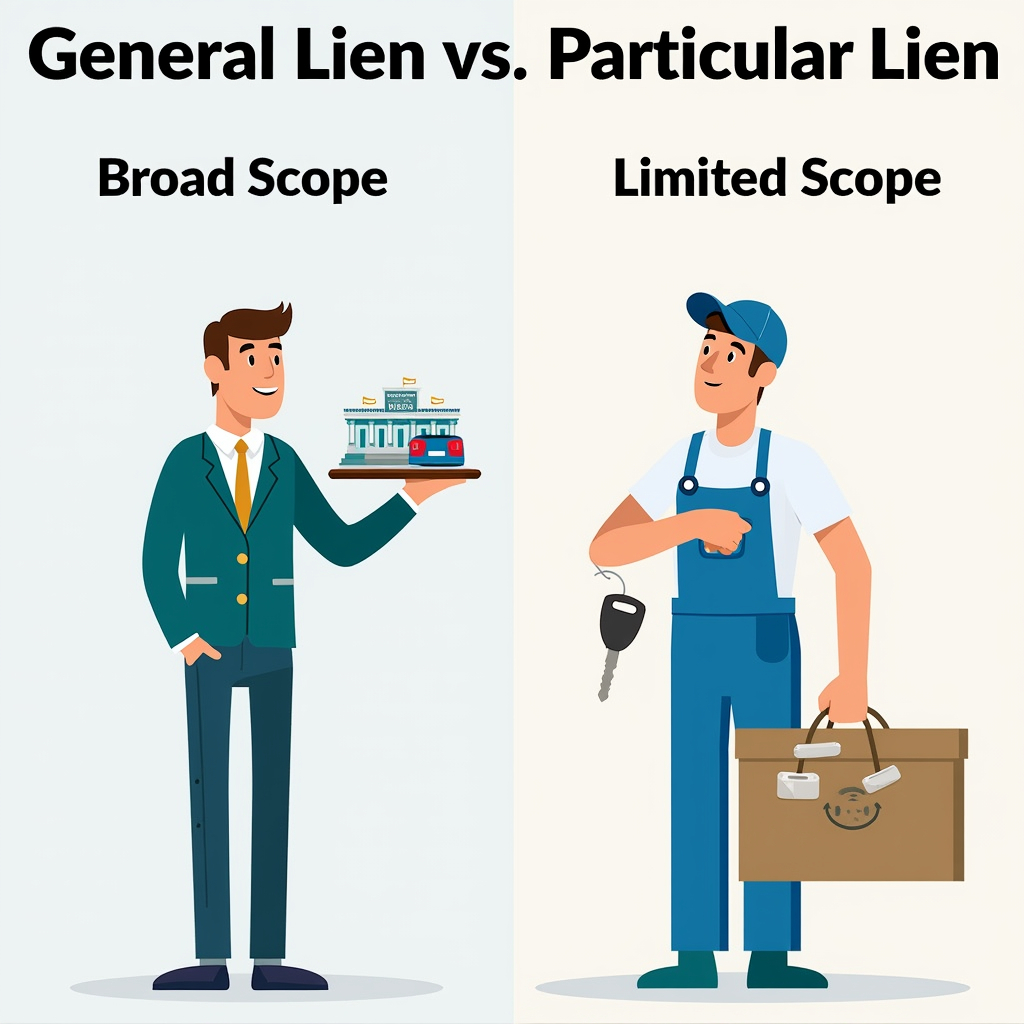

General lien

General lien means a legal right exercised by the certain professionals by retaining the property of the others until a debt or obligation is settled by them. Moreover, in general lien creditors can retain any property in their possession until any outstanding debt owed by the debtor is paid. Unlike a specific property, a general lien is not limited to a specific property.

For example, bankers can exercise this right over the assets of their clients for all outstanding fees. This is not just fees related to a specific item of work.

Particular lien

A particular lien is a legal right that allows a person, usually a creditor, to retain possession of a specific property until a particular debt or obligation related to that property is settled. This type of lien only applies to the specific property for which the debt arose.

For example, if a mechanic repairs a car, they may have a particular lien over the car. It means they can hold onto the car until the repair bill is paid. The lien is limited to the car and it does not extend to other assets of the owner.

Scope

General lien

The scope of a general lien is broad and extensive. It covers all property and assets that belong to the debtor. This includes not only the assets they currently own but also any future assets they may acquire. The creditor has the right to keep the debtor’s property until all the entire debt is repaid. Thereby, this lien gives the creditor a great level of protection.

Particular lien

A particular lien is more limited in scope as compared to a general lien. It applies only to specific property or assets directly related to the debt or service in question. The creditor can retain possession of the specific asset until the payment for the particular service is fulfilled. Unlike a general lien, a particular lien does not cover all of the debtor’s assets. It only covers the specific item or property that is connected to the debt. Particular liens are restricted to specific assets that directly relate to the debt or service.

Examples

General lien

To clarify the idea of a general lien, the following examples can be considered:

If a customer has an overdraft, the bank may use a general lien on all assets and funds belonging to the customer. This means the bank can hold onto the customer’s assets until the overdraft is completely paid off.

When a person does not pay their taxes, the government can place a general lien on the taxpayer’s property. The government may then seize and sell these assets to recover the tax debt.

In certain cases, lenders can acquire a general lien on a business’s assets as security for a loan. This allows the lender to retain possession of the business’s property until the loan is fully repaid.

Particular lien

Here are a few examples that highlight how a particular lien operates:

If a mechanic repairs a vehicle and the customer fails to pay for the service, the mechanic can place a lien on the vehicle. The mechanic is entitled to hold onto the vehicle until the customer pays for the specific repair work.

An artisan, such as a jeweller or tailor, can hold onto a customer’s item (e.g. jewellery or clothing) if payment for services or labour provided is not made. This lien only applies to the specific item that was worked on.

A transporter or shipping company can exercise a lien on goods they have delivered if the customer has not paid the shipping charges. The lien only covers the particular goods that were transported.

Legal recognition

General lien

Section 171 of the Indian Contract Act, 1872 talks about the general lien. However, this Section does not define what is general lien. As per the Section, certain professionals like bankers, factors, wharfingers, attorneys of a High Court, and policy brokers have a special legal right called general lien. If someone gives their property to these professionals for any reason, in such situations these professionals have the right to keep those goods until all the debts are fully paid. This right applies to the total amount the person owes, not just the specific payment related to those goods.

From the above Section it can be understood that a general lien means right to hold onto someone else’s property until a debt or claim is paid. General lien gives certain people the right to hold on to goods until the full payment has been made to them. Such people can keep the properties even if the debt has nothing to do with those properties.

For example, if someone gets a bank loan and gives them their valuables as collateral. The bank can keep their valuables not just until the loan is satisfied but also for any other debts they owe to the bank. It might be like fees or another loan.

Also, a wharfinger, who is a person that stores goods at a port, has the right to keep the stored goods until all dues related to storage and other services are paid.

This right to hold goods is an absolute right for these professionals, unless there is an agreement explicitly stating something different.

M. Mallika vs. State Bank of India & And Anr. (2006)

Facts

In the case ofM. Mallika vs. State Bank of India & And Anr. (2006), the appellants took loans and filed complaints against the State Bank of India. They argued that the bank failed to return their title deeds despite the fact that they had cleared the loan amounts. The bank, however, contended that the appellants still had outstanding dues as guarantors for other loans.

Issue

The main issue of this case was whether the bank has the power to keep the title deeds in accordance with the general lien provided under Section 171 of the Contract Act.

Judgement

The National Consumer Disputes Redressal after hearing both parties’ arguments held that the bank is entitled to exercise a general lien over the title deeds. In addition to that, the court also explained that although Section 60 of the TP Act permits a mortgagor to reclaim documents upon full payment. On the other hand, Section 171 of the Indian Contract Act, 1872 permits the bank to retain documents as a security for any unpaid debts.

Krishna Kishore Kar vs. United Commercial Bank And Anr. (1981)

Facts

In the case of Krishna Kishore Kar vs. United Commercial Bank And Anr. (1981), the plaintiff, Krishna Kishore Kar, had deposited a margin money amounting to Rs. 1,83,500 with United Commercial Bank. This deposit was meant to secure various transactions and debts. However, the plaintiff later settled all dues with the other defendant, related to those debts. Despite the settlement, the bank retained the margin money, by claiming a general lien over it.

The lower court ruled that a portion of the margin money was to be refunded to the plaintiff. Nonetheless, the bank continued to assert its right to retain the margin under a general lien.

Issues

Whether the bank could claim the plaintiff’s margin money under a general lien, even after the plaintiff had settled his dues?

Whether a general lien could be applied to the margin money deposited by the plaintiff despite an express contract defining its purpose and limitations?

Judgment

The Calcutta High Court held that the bank could not claim the margin money under a general lien. It was observed that while a general lien grants bankers the right to retain a customer’s assets until debts are cleared, it is not applicable in all cases. Specifically, when an express contract is in place that defines the purpose and scope of the deposited funds.

This contract limits the bank’s ability to apply a general lien. In this case, the margin money deposit was governed by an express contract that specified its purpose and restricted the application of the general lien. Therefore, since the plaintiff had already settled the dues related to the margin money, the bank had no legitimate claim over it. The court ordered that the bank must refund the margin money to the plaintiff.

Particular lien

Section 170 of the Indian Contract Act, 1872 does not specifically define the term “particular lien”. However, it describes the concept of a particular lien. Section 170 talks about a situation where a bailee has done work by using his/her labour or skill on the goods. In such situations, the bailee has the right to retain the goods until they are paid for the specific services which they provided with respect to those goods.

From the above Section, one can understand in general that a particular lien means it is the right of a person to retain the possession of the specific goods until payments are made for the services which were provided. This kind of lien applies to the particular goods but does not apply on any general balance of accounts or any other debts.

For instance, in order to cut and polish a rough diamond, ‘A’ gives it to the jeweller and the jeweller does the work. The jeweller can hold on to the diamond until A pays for the services. Here the jeweller’s right is limited to the diamond given only, as the services were provided in relation to that particular diamond.

If A gives cloth to B (tailor), to make a coat from it. But B promises to give A three months’ credit, then B cannot hold on to the coat until payment is made. This is because there was an agreement for credit, the tailor has no right to keep the coat. It can be understood that one can keep up the goods only when there is no explicit agreement between the parties.

Enforcement

General lien

A general lien gives the creditor the right to retain any property in their possession until all debts owed by the debtor are paid. It does not matter whether the property relates to the specific debt or not. In the general lien, the creditor may retain possession of multiple items of property. In this lien, property is not just the one that is related to the particular debt. The general lien applies across all assets in the creditor’s possession until the debtor’s general obligation is paid in full.

For example, a banker may exercise a general lien over all securities or funds held on behalf of a client if the client owes the bank any money.

Particular lien

A particular lien applies only to the specific item of property that is directly related to the debt or obligation. The creditor can retain possession of the specific property until the associated debt is paid. This lien can be enforced when the debtor refuses to pay the debt amount, the lienholder may be able to sell the specific property to recover the debt. But this typically requires following legal procedures or obtaining court approval, depending on the jurisdiction. The lienholder cannot claim any other property of the debtor for unrelated debts.

For example, if a borrower pledges gold to secure a loan, the lender can retain possession of the gold until the debt is cleared.

Advantages

General lien

Creditors have more protection with a general lien. This is because they can seize any of the debtor’s assets to recover the debt, not just specific items.

Creditors do not need to prove that the property is directly connected to the debt. They can make it simpler to enforce compared to a particular lien.

In cases where a debtor has both general and specific liens on their property, the general lien usually takes priority and is settled first.

General liens are less common than specific liens and the rules about them may change depending on the location.

Particular lien

The creditor knows exactly which property they can take to settle the debt, as it is tied to a specific asset only.

Since the creditor does not need to go through all the debtor’s assets, it is quicker to enforce compared to a general lien.

It is considered more fair because the creditor can only take the property directly connected to the debt. Thus it protects other assets.

With a particular lien, the debtor’s other assets that are not related to the debt are safe.

If there are multiple liens on the debtor’s property, a particular lien is usually settled before a general lien.

Disadvantages

General lien

Creditors may find it challenging to locate and seize specific assets to cover the debt. This is because this lien applies to all of the debtor’s possessions.

The wide range of assets that can be seized under a general lien. This may leave the debtor with very few resources. Thus it makes it hard for them to cover basic living expenses.

Creditors may face more time and expense in enforcing a general lien. It becomes time-consuming especially if legal help is needed to identify and seize assets.

Particular lien

The lien only covers the specific asset or property it is attached to. So it does not protect other debts or assets.

If the asset is lost or damaged, the creditor may not recover the full amount they owed.

The asset’s value might decrease over time, which could make it harder for the creditor to collect the full debt amount.

If the debtor fails to repay, the creditor might not be able to get the full payment owed.

Taking legal action to seize the property takes a lot of time and money for the creditor.

When the property is sold, a particular lien holder may not get paid first if other liens take priority.

Judicial pronouncements

General lien

Bank of Bihar vs. State of Bihar & Ors (1971)

Facts

In the case ofBank of Bihar vs. State of Bihar and Ors (1971), the bank is the appellant which provided advances to the Jagdishpur Zamindari Co. Ltd. (defendant no. 2) under a cash credit system. As a way of security, the company pledged the sugar bags to the bank. These sugar bags were stored in warehouses, and banks had the keys to such warehouses.

In 1949, the state of Bihar seized 1,818 bags of sugar from the warehouse. It was done as per an order issued by the Rationing Officer and the District Magistrate Patna. The bank, as a pledgee, held that the sugar as security against its loan to defendant no. 2.

Later sugar was sold, and the sale proceeds were deposited in the government treasury. The Cane Commissioner attached the amount under the Bihar and Orissa Public Demands Recovery Act, 1914 for sugar cess arrears owed by the Bhita Sugar Factory. This factory had a business arrangement with defendant no. 2. The bank sued the State of Bihar and the Jagdishpur Zamindari Co. Ltd., for the purpose of either to return the sugar or compensation for the value of the seized sugar.

Issues

The main issue was whether the bank, as a pledgee, has a right to exercise general lien over the seized sugar or not?

Judgement

Initially the Trial Court decided in the favour of the bank. It stated that the bank’s rights as a pledgee were not taken away by the government while seizing the sugar. The court further ordered the state of Bihar to pay Rs. 93,910 with interest to the bank. However, when the case was appealed, the Patna High Court disagreed with the Trial Court decision. It ruled that the bank had no right to claim the sugar or the money made from its sale. This is because the action by the government by seizing property was lawful. Similarly, such money obtained from selling those seized assets was used to pay off outstanding debts related to the sugar cess.

While on appeal before the Supreme Court it disagreed with the decision of the Patna High Court. The decision of the Supreme Court was in favour of the bank. It said that the bank had the right to exercise the lien by keeping sugar as a security for the loan amount. The government’s seizure did not take away the bank’s right to the sugar. Therefore, the government had to compensate the bank for the value of the seized sugar.

The City Union Bank Limited vs. C. Thangarajan (2003)

Facts

In the case of The City Union Bank Limited vs. C. Thangarajan (2003), the City Union Bank filed a suit in 1986 to recover Rs. 2568.15 from Kumaraswamy, Chellapappa, and Thangarajan. It is based on a promissory note executed for a Rs. 4,000 loan which was taken in 1983. Thangarajan denied borrowing money and stated that he had no dealings with the bank regarding the loan.

Thangarajan, a respected Tamil Pandit, filed a suit against the Bank to recover Rs. 11,053, including interest on a fixed deposit (FD) and damages of Rs. 10,000 for reputational harm. He had deposited Rs. 10,000 in 1985, but when he attempted to withdraw the amount through Vijaya Bank, the City Union Bank dishonoured the request, and claimed a lien over the FD due to Thangarajan’s alleged loan liability.

Issue

The main issues were:

Whether Thangarajan was liable for the loan along with the other defendants?

Whether the bank could exercise a general lien on Thangarajan’s FD for recovery of the alleged loan?

Whether Thangarajan was entitled to damages for reputational harm?

Judgement

The Trial Court found that Thangarajan had signed the promissory note, and that made him liable for the loan. However, the court also ruled that by filing a separate suit for recovery of the loan, the bank had waived its lien over the FD. The court awarded Thangarajan Rs. 13,055 for his FD and Rs. 2,000 as damages for the harm to his reputation. Both the bank and Thangarajan appealed. But the appellate court upheld the Trial Court’s decision, and held that the bank could not exercise a general lien without an express contract or authorisation from Thangarajan.

M.Shanthi vs. Bank of Baroda (2017)

Facts

In the case of M.Shanthi vs. Bank Of Baroda (2017), the petitioner took a loan of Rs. 47 lakhs from the Bank of Baroda in 2013. The petitioner lent property documents as security for those loan amounts. She was regular with payments until 2015, when she faced financial difficulties. Further she was ready to pay the loan amount and she wanted to get her property back. Meanwhile, the bank refused and claimed the right to keep the documents. They further argued that she was also a guarantor for another loan amount which was related to CMS Educational Trust. This trust had a large outstanding amount.

Issue

The issue in this case was whether the bank could legally keep the petitioner’s property documents for a loan she had guaranteed, even though it was not related to her own loan. Further whether the bank could use a general lien to hold the documents after her personal loan was repaid.

Judgment

Orissa High Court observed that as per Section 171 of the Indian Contract Act, 1872 bankers have a right to retain any goods bailed to them as security for a general balance of account. This right of lien applies unless there is an express contract excluding it.

The court held that a bank can only exercise the right of lien on the properties that were been given to it by its own customer. However, the bank does not have the right to keep goods or property that belong to someone else, even if the customer is involved in the transaction.

The lien can only be enforced when the balance due relates to the customer’s own account, not the account of other parties, even if the customer is a guarantor. In cases involving partnerships, banks cannot exercise a lien on the private account of one partner for the debts owed by the partnership. The court ordered the bank to release the outstanding dues to the petitioner along with interest.

In this case, the court ruled that the bank had no legal right to keep the petitioner’s gold ornaments. The bank could not rely on its bye-laws or Section 171 of the Indian Contract Act, 1872 in order to hold onto the gold after the petitioner had fully paid off her loans for which the gold was pledged. The court found that the action taken by the Bank was unfair. Therefore, the court cancelled the notice sent by the Bank. Thus the court ordered them to return the gold ornaments to the petitioner immediately. Both parties were told to bear their own legal costs.

Particular lien

Vijay Kumar vs. Jullundur Body Builders And Others

Facts

In the case ofVijay Kumar vs. Jullundur Body Builders And Others (1981), the petitioner, Vijay Kumar, entered into a business relationship with a bank as a guarantee facilitated through fixed deposit receipts (FDRs). The FDRs were provided to a bank as security for a specific bank guarantee.

The dispute arose when the bank attempted to exercise a general lien over the FDRs. Even though the original guarantee had been discharged, it was done in order to cover an unrelated overdraft account balance.

Issues

Whether the bank has the right to claim a general lien instead of particular lien over the Fixed Deposit Receipts when they were specifically pledged for a particular purpose?

Judgement

The court held that while banks generally possess a lien under Section 171 of the Indian Contract Act, 1872, this right can be overridden by a specific contract between the parties. In this case, the FDRs were pledged for a particular purpose which had already been satisfied.

Thus, the bank could only claim a particular lien over the FDRs and not a general lien for other unrelated debts. Thus, the court held the bank’s claim to use the FDRs for settling the overdraft account was invalid.

Summary of difference between general lien and particular lien

Parameters

General lien

Particular lien

Definition

Under this lien it gives the right to a creditor to keep any goods owned by someone else until they pay a due amount.For example, a bank can exercise this lien to various documents if a customer has unpaid loans.

Under this type of lien the person can keep the specific goods until payment for those goods is received. For example, a tailor makes a custom suit for a customer. The tailor has the right to keep the suit until the customer pays for it.

Scope

This applies to all types of goods which are not paid. It does not matter what the debt amount is. A bank can use this right across the different types of loans.

This type of the lien is only applicable to certain items. This lien is confined to those specific goods. This lien is confined to specific goods because it is based on the principle that the lien holder has a legal right to retain possession of particular items in order to secure payment for those items.

Automatic vs. agreement

This right is not automatically given; it usually requires a written agreement between the parties.

This right comes automatically as per Indian Contract Act, 1872. Here in this type of lien right automatically comes without any special agreement.

Right to sell

The holder of a general lien does not have the right to sell the goods to recover unpaid debts. They can only keep possession of the goods until the debt amount is paid.

In a particular lien, the holder usually cannot sell the goods. But they can sell some rights under special circumstances.

Common users

Banks and financial institutions often use this type of lien. Also wharfingers and policy brokers can exercise this lien. These entities can retain possession of specific goods or documents until payment is made for their services.

Service providers, like repair shops or storage companies, often use this lien. Additionally, other parties such as bailees , agents, pledgees, partners, unpaid sellers, and finders of goods also utilise this lien.

Debtor claims

This lien allows claims against multiple debtors. For instance, if a business owes money across different loans, the bank can hold their assets.

This lien is limited to only one debtor. It means that the lien only applies to the individual or entity.

Enforcement

The holder can sell any of the debtor’s assets to recover the full amount owed, regardless of the specific goods.

The lien can only be enforced by selling the specific items but not the debtor’s other assets.

Termination

A general lien remains in effect until all debts owed by the debtor to the lien holder are settled.

A particular lien is terminated once the specific debt related to the particular goods is paid.

Conclusion

General lien and particular lien are both ways for creditors to protect themselves. General lien lets the creditors hold the debtor’s property until all debts are paid by the debtor though if those debts are not directly connected to the property. The general lien is commonly used by banks. On the other hand, a particular lien only applies to a specific item of property that is linked to a particular debt.

General liens are broad and cover all debts between the parties. In general liens, multiple financial transactions may occur over time. This approach provides security for creditors by retaining assets of the debtors until all amounts owed are cleared by them. However, particular liens on the other hand focus mainly on a single, specific debt. This makes them limited in scope. However, both types of liens are important in their own approach.

Frequently asked question (FAQs)

Can a lien be exercised on the personal property?

Yes, lien can be placed on personal properties such as cars, jewellery, or equipment.

What is the difference between the lien from a mortgage?

In a mortgage, for the loan amount property is used as collateral. A mortgage is also a type of lien. But in a lien, it can apply to various types of property and debts. It is not only confined to mortgages. A mortgage is also a kind of property in which the owner gives someone a legal claim on their property as security for a loan. A lien, on the other hand, is a legal right to hold or claim the property, because of an unpaid debt.

What is the effect of selling the property with a lien?

If a property with a lien is sold by the person, the lien holder’s interest needs to be paid by that person. In other words the lien holder can still claim the property even after the sale.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

This article has been written by Tanya Dua pursuing a Diploma in Patent Law & Analysis (USPTO): Searches, Specifications, Prosecution, Litigation and Licensing from LawSikho.

Table of Contents

Introduction

The discovery of a drug occurs when there is a disease or condition for which suitable medicinal conditions are unavailable. Initially, the discovery occurs at the academic level by setting up data that can possibly be useful in curing the disease. This helps scientists to set up a base for producing suitable medicine for curing the disease.

What is AI

AI, i.e., artificial intelligence, is a boom in human mankind. It is a combination of human ability and technology, or it is when technology is modified in a way that makes it work just like a human brain. Still, it is not just limited to the brain of a single human being; it is a cluster of thousands of human brains at a given point in time.

For a few decades, AI was limited just to computers, but as time passed, it has now been totally incorporated into our lives. Nowadays, AI is used for every big and small activity, from helping with household chores to operating a person and predicting the future, just with the specific data and instructions given to it. AI is designed in a way that for every single research project, AI combines the data of thousands of researchers to provide a single output.

AI has made medical terminologies way easier due to the ability of AI to give precise and accurate outcomes by analysing the stored data and commands given, as well as the ability of AI to reach places that are way more difficult for humans to counter with. Several branches of AI have been involved in the different actions that take place in every aspect of life. Branches of AI include machine learning, robotics, computer vision, etc.

The potential of artificial intelligence in drug development

Artificial intelligence (AI) has revolutionised various industries, and its potential in drug development is immense. AI offers a range of tools and techniques that can enhance the efficiency and effectiveness of drug discovery and development processes.

Drug discovery:

AI can analyse vast amounts of biological data, including genomic information, protein structures, and disease pathways, to identify potential drug targets. This process is much faster and more efficient than traditional methods, which often rely on manual labour and serendipity.

Machine learning algorithms can predict the structure-activity relationships of compounds, enabling the rapid identification of lead molecules. This is a critical step in drug discovery, as it helps to narrow down the field of potential candidates for further testing.

Virtual screening techniques powered by AI can sift through large libraries of compounds to identify those most likely to bind to a specific target. This process is much faster than traditional high-throughput screening methods, which can take weeks or even months.

Drug design:

AI algorithms can design new molecules with desired properties, such as high affinity for a target, specificity, and low toxicity. This is a complex and challenging task, but AI is well-suited to it due to its ability to handle large amounts of data and to learn from experience.

Generative models can create novel molecular structures not found in nature, expanding the chemical space for drug discovery. This is a powerful tool for discovering new drugs that are more effective and have fewer side effects.

AI can also optimise existing drugs to improve their potency, efficacy, and safety. This is a valuable tool for drug companies, as it can help them to extend the lifespan of their products and to improve the lives of patients.

Clinical trials:

AI can analyse clinical trial data to identify patterns and trends that may not be readily apparent to human researchers. This can help to improve the design of clinical trials and identify potential problems early on.

Machine learning algorithms can predict patient outcomes and responses to treatment, enabling personalised medicine approaches. This can help to ensure that patients receive the most effective treatment for their individual needs.

AI can also be used to design more efficient clinical trials, reducing the time and cost of drug development. This is a critical factor in bringing new drugs to market faster and at a lower cost.

Drug safety:

AI can analyse large volumes of safety data to identify potential adverse effects and drug interactions. This is a critical task, as it helps to ensure the safety of drugs for patients.

Natural language processing techniques can extract information from medical literature and electronic health records to identify safety signals. This can help to identify potential problems early on, before they cause harm to patients.

AI can also be used to develop predictive models for drug toxicity, allowing for proactive risk management. This can help to prevent adverse events and to ensure the safety of drugs for patients.

Drug manufacturing:

AI can optimise manufacturing processes for drugs, reducing costs and improving quality. This can help to make drugs more affordable for patients and improve the efficiency of the drug supply chain.

Machine learning algorithms can monitor production lines for anomalies and potential quality issues. This can help to identify problems early on, before they cause significant damage.

AI can also be used to automate quality control processes, ensuring the consistency and safety of drugs. This can help to ensure that patients receive high-quality drugs that are safe and effective.

Overall, AI has the potential to transform drug development by making it faster, more efficient, and more effective. As AI technologies continue to advance, we can expect even greater innovations in drug discovery, design, clinical trials, safety monitoring, and manufacturing.

Steps involved in drug discovery

Identification of target and then validating

The first step involved in drug discovery is identifying the target. The target here refers to the site that is the root cause or involved majorly in causing the disease. Once the target is identified, it becomes easier for the scientists to evaluate the type of drug that will bind the site efficiently.

The phenomenon known as “Lock and Key” is involved in binding the drug with the site of action. This phenomenon states that just like a lock can be opened with a single type of key, in the same way, the drug that will be more effective will be the one that properly fits and binds with the site of action.

So, it is very important to have the right drug, as it depends upon the drug to enhance or inhibit the ability of the target.

Identification of the right drug can be done by:

Firstly, testing the compounds, which can be helpful.

Then evaluating the previously known drugs that could cure the new disease discovered.

Manipulating the drug according to the information gained while examining the disease.

Preclinical research

After the formulation of the drug, it becomes important to check the toxicity level of the drug. There is a high possibility of toxicity for human beings. The preclinical research can be conducted by both methods: In-vitro and In-vivo

In-vitro: In this process, the study is performed inside the laboratory on the cells, tissues, or other parts of an organism.

In-vivo: In this process, the study is performed on living organisms, specifically laboratory animals, which may include genetically modified mice, frogs, cats, fishes, etc.

Toxicity level can be evaluated by the above methods, and it also includes giving a high dosage of the drug to animals to check the changes and responses taking place in the animal’s body, behaviour, and functioning.

After the data is obtained from the above observation, it is provided to regulatory authorities to conduct clinical trials on human beings.

Further, after the toxicity levels, other important factors are also determined, like:

Amount of drugs appropriate for human use.

How the drug is absorbed, distributed, metabolised, and excreted.

Method by which the drug must be administered in the body, i.e. orally or by injecting.

Effects of drugs on different groups of people (Age, Sex, Gender)

The environmental factor is also taken into consideration.

How the drugs will react under the influence of the other drugs.

Clinical trials

After the trials on the animals, the next step involved in drug discovery is clinical trials, which refer to the study or trials that involve human beings. To conduct trials appropriately, some protocols have been set. On the other hand, the researchers go through the previous data available, and then they decide:

Who and how many people can participate?

How long will it take to achieve all the data required?

The dosage and method by which the drug must be given?

What data needs to be collected, reviewed, analysed, and reported?

Regulatory approval

After the successful clinical trial, the drug is then made to enter the market for usage. The final data is a combination of the data collected previously (by preclinical trials) as well as real-world evidence, and then it is filed with a marketing authorisation submission for approval for public use.

The report must include:

Proposed labelling;

Saftey updates;

Drug abuse information;

Patent information;

Any data from the studies that may have been conducted outside the country;

Institutional review board compliance; and

Direction of use.

Post-market safety monitoring

The actual picture of any drug forecast when it has been released in the market and has been used by people for a few years now.

This monitoring helps in obtaining data on the following:

Modifications that are required based on the results.

What serious side effects can take place?

Modifications of dosage if needed

If it counteracts with any other type of medications

What other alternates are available in the market?

FDA (Food and Drug Administration) is responsible for safeguarding public health, so it closely keeps an eye on the companies to monitor the safety of the drugs properly, using the FDA Adverse Event Reporting System database.

Artificial intelligence in drug discovery

AI can be used in various steps for the discovery of the drug:

AI in the identification of target: Several approaches are involved:

With the involvement of AI in drug discovery, AI models such as machine learning make it easy to go through a large number of genomic data points at a time, which eventually makes it easier to reach the appropriate drug in a short span of time.

It becomes easier with the help of AI to remove the complexity of the interactions, like protein-protein interaction, to help ease the identification of target sites.

AI covers a large range of compounds that could have a chance of binding to the target and, as an outcome, can quickly predict the most accurate compound.

AI is also helpful in confirming the role of the target in the evolution and progression of the target.

It has become possible to have personalised drugs from patient to patient based on their genomic and clinical data.

AI in preclinical research

The datasets used by AI, like machine learning, help in predicting the toxicity levels of a compound using pre-existing data.

AI is used in making models that, to a large extent, mimic human anatomy, which makes it easier for scientists to test compounds, set dosages, determine the effects of compounds, etc.

It helps in predicting the pharmacokinetics of the drug, i.e., absorption, distribution, metabolism, and excretion, which ultimately leads to the prediction of how the drug will behave upon entering the human body.

It is due to this that the need for testing drugs on animals has been reduced.

AI in clinical trials

Using AI, it has become easier to analyse the patient’s genomic, clinical, and medical data before testing any drug on them. So, in return, it became easier to choose the right candidate for clinical trials.

During the trial method also, AI is useful in the modification of the amount, type, and precautions needed to be taken during the period of trials itself.

Clinical trials have always been a time-consuming process, but due to AI, it has become a fast process due to the ability to automate drug integration and report generation.

It also helps to know the long-term side effects of the drugs.

The accuracy of the drug development has been increased.

The quality of the drug formation has been improved.

AI in regulatory approval

Due to the updating of time at every interval, it has become easier to submit the analysis that has been done throughout the trials.

AI can predict missing information, summarise all the data, and can automatically detect errors.

Provides insights that are useful for the regulatory bodies to improvise and make decisions regarding.

It also ensures that the drug generated is correct according to the standards.

AI in post-market safety monitoring

Helps in monitoring the long-term effect of the drug.

AI can keep a record of all the patient data, from medical conditions to life insurance and smart appliances (which are used to monitor day-to-day activities) and alert the patient much before an incident takes place.

AI helps in tracking the records of patients with drug-executing companies.

AI can also detect the activities of a patient through their social media and search history related to drugs in any way.

It helps in keeping a record of patient problems and feedback across the globe.

Can also predict the interaction between any other medication.

Challenges of using AI

Artificial intelligence (AI) has the potential to revolutionise drug discovery, but several limitations and challenges need to be addressed:

Data requirements:

AI models require vast amounts of high-quality data for training and validation.

Collecting, cleaning, and preparing this data is time-consuming and expensive.

Data acquisition can be particularly challenging for rare diseases or conditions with limited patient populations.

The data used in datasets may not be representative of the real world, leading to biased or inaccurate results.

Data bias:

The data used to train AI models can be biased due to factors such as demographics, socioeconomic status, or underlying health conditions.

Biased data can lead to models that make unfair or inaccurate predictions.

For example, if a dataset is predominantly composed of data from a specific population group, the model may not perform well when applied to other populations.

Lack of interpretability:

AI models often lack interpretability, making it difficult to understand how they arrive at their predictions.

This lack of transparency can make it challenging to identify and correct errors in the models and to ensure they make decisions based on relevant factors.

The inability to interpret model predictions can also hinder regulatory approval processes.

Continuous data updates:

AI models need to be continuously updated with new data to maintain their accuracy and effectiveness.

This can be a significant challenge, especially in rapidly evolving fields like drug discovery.

Failure to update models regularly can lead to outdated or inaccurate predictions.

Privacy concerns:

AI-based drug discovery often involves processing large amounts of sensitive patient data.

Ensuring the privacy and security of this data is critical to maintaining public trust and avoiding ethical violations.

Robust data protection measures and compliance with privacy regulations are essential.

Infrastructure and knowledge gaps:

Effective use of AI in drug discovery requires advanced computational infrastructure and specialised knowledge in both AI and drug discovery.

Many industries lack the necessary resources and expertise to fully leverage AI for drug development.

This can hinder the adoption and implementation of AI-powered drug discovery tools and platforms.

To overcome these challenges and fully harness the potential of AI in drug discovery, ongoing research and collaboration are needed to:

Develop more robust and interpretable AI models.

Mitigate data bias through careful data selection, preprocessing, and validation.

Ensure data privacy and security through robust data protection measures and compliance with ethical guidelines and regulations.

Provide the necessary infrastructure and training to researchers and professionals to enable widespread adoption of AI in drug discovery.

Conclusion

The intersection of AI and drug discovery has revolutionised the lives of human beings. Due to the large datasets used by AI, the discovery of drugs has become easier, cost-effective, highly accurate, decreased level of toxicity, and highly tailored. Although even after so many positive effects of AI, there are some negative effects, like computational errors, over-reliance, ethical issues, etc.; if these issues are resolved, AI can transform drug discovery to a whole new level.

This article is written by Sakshi Kuthari. It discusses in detail Article 44 of the Indian Constitution, its historical background, significance, and the constitutional provisions relating to Article 44. The advantages and challenges involved in implementing the Uniform Civil Code are also enshrined along with the landmark judgements.

Table of Contents

Introduction

The Constitution of India comprises 395 Articles (after 106 Constitutional Amendments done in the Constitution there are now 448 Articles in number) each with its own importance and distinct role in serving the Indian population. The Indian Constitution grants fundamental rights and outlines various procedures that the authorities must follow. Among them, Article 44 stands out as the only provision that remains entirely theoretical, without any practical application to date. Article 44 provides for a Uniform Civil Code applicable to all Indian citizens, aiming for uniformity across the nation.

This Article was inserted to standardise laws relating to personal matters such as inheritance, marriage, divorce, and adoption in order to create consistent standards amidst India’s diverse culture. Despite Article 44 being part of the Indian Constitution for several decades, the Uniform Civil Code has not yet been implemented. The importance of Article 44 is discussed in this article, which explores in detail how its execution could positively impact equality and reduce religious bias and discrimination.

What is Article 44 of the Indian Constitution

Part IV of Article 44 of the Indian Constitution mandates that the State endeavour to establish a Uniform Civil Code for all citizens across the country. Article 44 aims to protect the rights and practices of different sections of the population. The Uniform Civil Code seeks to create a single, consistent set of laws governing personal matters such as marriage, divorce, inheritance, and property for all individuals, regardless of their religious beliefs or community affiliations. It represents an effort taken by the State to harmonise the diverse personal laws that currently exist among India’s various religious communities, including Hindus, Muslims, Christians, and others. The Uniform Civil Code acknowledges India’s rich diversity in religion and culture and highlights the nation’s commitment as a secular state to ensure equality and justice for all its citizens. The State faces various challenges because of various different personal laws that apply to different religious groups. These differing laws can lead to inconsistencies in legal rights, particularly in family-related matters.

History of Uniform Civil Code

The concept of a Uniform Civil Code dates back to the Colonial period, beginning with the principle of ‘lex-loci’, which translates to ‘law of the land’. In 1840, a report known as the Lex-Loci Report emphasised the need for a unified code of Indian laws relating to contracts, marriage, crimes, and evidence. However, the report also suggested that the personal laws of Hindus and Muslims should be excluded from this codification. The Report of 1840 and the Queen’s Proclamation of 1859 reinforced this stance by stating that religious matters would not be codified, and that personal laws should continue to be governed by religious and community-specific rules. During this time, criminal laws were codified for the entire country. In 1828, Lord William Bentick, the first Governor General of India, intervened in Hindu religious practices. On December 4, 1829, he issued Regulation XVII, declaring the practice of sati illegal and punishable by the courts. Additionally, female infanticide was made illegal. Later, Lord Dalhousie and Ishwar Chandra Vidyasagar passed the Hindu Widow Remarriage Act, 1856.

On 23 November, 1948, the Constituent Assembly of India had an engaging debate regarding the draft of Article 44, which provided for the Uniform Civil Code. During the discussion and subsequent voting, both the supporters and opponents of the provision presented detailed arguments. It was evident that many Muslim members appeared deeply apprehensive, which likely contributed to the fact that those opposing the provision were predominantly from Muslim backgrounds. They contended that a Uniform Civil Code would infringe the freedom of religion, potentially disrupting the harmony within the Muslim community, and that it would interfere with the personal laws.

It was argued by the supporters of the provision that a Uniform Civil Code was important because it would maintain national unity and uphold the secular values of the Constitution. It was contended by one of the members of the Drafting Committee that this provision would impact not only the Muslim community but also the Hindu community. It was also further emphasised that securing the rights of women would not be possible without a Uniform Civil Code.

At the conclusion of the debate, it was clarified that the Uniform Civil Code was not an entirely new concept; India already had a common civil code. The proposed code would merely extend its coverage to marriage and inheritance, areas that were left unaddressed. Despite the heated debate, the Draft Article was adopted on the same day, without any amendment.

Significance and implementation of the Uniform Civil Code

India’s rich cultural diversity encompasses individuals from various backgrounds, each with distinct beliefs and practices. Achieving consistency amidst this diversity is crucial, and implementing the Uniform Civil Code can play a key role in this process. By creating a consistent legal framework for all citizens, the Uniform Civil Code strengthens the concept of secularism enshrined under the ambit of the Indian Constitution and contributes to national unity. Currently, many constituencies are fragmented along religious and community lines, leading to vote-bank politics based on religion. The introduction of a Uniform Civil Code could reduce such religious-based political practices.

The Uniform Civil Code was introduced in the year 1950; its actual implementation would represent a major advancement in India’s progress, helping to overcome religious and other obstacles to nation-building. It is essential for both Indian citizens and lawmakers to recognise that fully implementing Article 44 will promote secularism in the country. The aim of a Uniform Civil Code is not to interfere with or prohibit religious practices but to establish a consistent set of laws applicable to all citizens, ensuring equal treatment irrespective of an individual’s religion. Additionally, the Uniform Civil Code could enhance the efficiency and effectiveness of the judicial system, particularly in resolving disputes relating to religious matters.

At present, personal laws often include provisions that undermine women’s rights or create gender inequalities. For example, practices such as the Muslim tradition of Parda, the marriage of girls below the age of 15 years according to the Mohammedan law, and inequalities in succession rights disadvantage women. The enforcement of the Uniform Civil Code would address these disparities, providing women with equal status and rights in society, particularly in communities with stringent practices.

Constitutional provisions relating to Article 44

The Constitution (Forty-second Amendment) Act, 1976, introduced an important term, “secularism.” The Indian cultural diversity and various religious practices existing in India make it essential to grant people the freedom to practise and propagate any religion of their choice. However, the Indian Constitution also provides for ‘equality before law’. In a country where freedoms of speech and expression, as well as religious practice are guaranteed, the existence of separate laws and rules for different religions raises the question of the Uniform Civil Code. The Uniform Civil Code includes several key provisions of Part III of the Indian Constitution, which are as follows:

No discrimination on the grounds of religion, etc.

Under Article 15 of the Indian Constitution, the State is prohibited from discriminating against any citizen of India solely on the basis of religion, race, caste, sex, place of birth, or any of these factors. In family-related matters, India has a system of personal laws, i.e., Hindu law for the Hindus, Muslim law for the Muslims and so on. For the Hindus, Section 5(i) of the Hindu Marriage Act, 1955, provides a law for monogamous marriage, but Muslim personal laws allow Muslim men to marry any number of wives. This was upheld solely in relation to the charge of discrimination based on ‘religion’. In the case of Srinivasa Aiyar vs. Saraswathi Ammal (1952), the Hon’ble Madras High Court pointed out that the Hindus have been enjoying for a long time their own indigenous system based on Hindu scriptures in the same way as Mohammedans were subject to their own personal laws.

Section 10 of the Divorce Act, 1869 states that a Christian husband can get divorce from his wife on the grounds of adultery committed by his wife. On the other hand, a Christian wife to get divorce from her husband has to prove not only the adultery of her husband but also something more, such as incest, bigamy, rape, cruelty, or dissertion. In the case of Mrs. Pragati Varghese And Etc. vs. Cyril George Varghese And Etc. (1997), the Hon’ble Bombay High Court held that Section 10 is discriminatory in nature on the ground of sex and is, thus, violative of Article 15(1). Further, a Christian woman cannot seek divorce on the grounds of cruelty and desertion, while women under Hindu law can seek divorce under Section 13(1)(ia) of the Hindu Marriage Act, 1955 (on the ground of cruelty) and Section 13(1)(ib) of the Hindu Marriage Act, 1955 (on the ground of desertion). This discrimination is based merely on the ground of religion, and this is violative of Articles 14 and 15 of the Constitution of India.

In the case of Danial Latifi vs. Union of India (2001), the validity of the Muslim Women (Protection of Rights and Divorce Act), 1986, was challenged on the ground that the Act, when compared with Section 125 of the Code of Criminal Procedure, 1973, is discriminatory against Muslim divorced women. However, the Hon’ble Supreme Court rejected this contention. The Hon’ble Supreme Court held that the purpose of both laws is the same, i.e., to address situations where a divorced woman is likely to be led into destitution and vagrancy. The Mohammedan law codifies and regulates under Section 3(1)(a) of the Muslim Women Protection of Rights and Divorce Act, 1986 provisions relating to maintenance. It provides that in addition to entitlement of mahr and maintenance to the Muslim wife during the Iddat period, the husband is also under an obligation to make a ‘reasonable and fair provision’. ‘Reasonable and fair provision’ means the needs of the divorced woman, the means of the husband, and the standard of living the woman enjoyed during her married life. Personal laws are established based on various religious practices and rituals, resulting in different sets of rules and regulations for people of different religions, even though they are all part of India.

Both Article 15 and 44 of the Constitution are inclined towards promoting gender equality. Article 15 aims to eliminate discriminatory practices based on personal attributes and Article 44 addresses the potential inequalities arising from the coexistence of diverse personal laws. The aim of the implementation of Uniform Civil Code is to unify these diverse regulations into a single set of laws, ensuring that all the citizens follow the same rules while respecting their right to practise their religion. It will also complement the equality and non-discrimination principles outlined in Article 15 by ensuring that personal laws do not lead to unequal treatment of individuals based on their religion or community.

Freedom to practise or profess religion

Article 25 safeguards individuals’ religious beliefs but does not protect practices that may be in conflict with public order, health, or morality. Article 25(1) of the Indian Constitution guarantees to every person, and not just the citizens of India, the ‘freedom of conscience’ and ‘the right freely to profess, practice, and propagate religion’. This right is subject to public order, health, morality, and other provisions relating to the fundamental rights.

Under Article 25(2)(a) of the Indian Constitution, it is provided that the state is not restricted from making any law regulating or restricting any economic, financial, political, or other secular activity that may be associated with religious practice. Under Article 25(2)(b), the state is not prevented from making any law providing for social welfare and reform or for opening Hindu religious institutions of a public character to all classes and sections of the Hindus.

Thus, it can be noted that the rights guaranteed to individuals and religious denominations under Article 25 are not absolute. They are subjected to maintenance of public order, etc. The religious rights of individuals and religious denominations under Article 25 are not absolute. It is subject to maintenance of public order, health, and morality.

India, as a secular country, still has different personal laws for various communities regarding civil matters, which contradicts the equality principles enshrined under Article 14. Implementing the Uniform Civil Code would promote equality by applying a uniform set of civil laws to all citizens, regardless of their religion, ensuring that everyone is treated equally before the law. The relationship between Articles 25 and 44 involves reconciling the need for a common legal framework with respect to the diverse religious practices.

Freedom to manage religious affairs

Article 26 of the Indian Constitution grants special protection to the religious denominations. In this article, the term ‘religious denomination’ means a religious sect having a common faith and organisation and designated by a distinctive name. Article 26 provides that every religious denomination thereof has the right to:

establish and maintain institutions for religious and charitable purposes;

govern its own religious affairs;

own and acquire movable and immovable property; and

administer such property in accordance with the law.

This right is subject to public order, morality, and health.

Article 25 guarantees particular rights to all persons, and Article 26 is confined to religious denominations or any section thereof. Article 26 thus guarantees collective freedom of religion.

To form a religious denomination, three conditions have to be fulfilled:

It is a collection of individuals who have a system of beliefs that they regard as useful for their well-being;

They have a common organisation; and

Collection of these individuals constitutes a distinctive name.

Article 26 grants religious denominations the right to manage their own religious affairs and institutions.

Article 44 aims to standardise personal laws through a Uniform Civil Code. By implementing a Uniform Civil Code, the various different religious practices existing in different religions will be resolved by putting in order the personal laws of different religions following the principles of equality.

Advantages and challenges in implementing the Uniform Civil Code

Advantages of implementing the Uniform Civil Code

Some of the advantages of implementing a Uniform Civil Code in India:

National unity will be strengthened by bringing all the Indian population, regardless of their caste, religion, or tribe, under a single Uniform Civil Code. It contribute to national unity by ensuring that all citizens of India are treated equally, replacing diverse personal laws, etc.;

It helps to minimise the influence of vote bank politics that various political parties practise during elections. A Uniform Civil Code would standardise laws, reducing the scope for any type of targeted promise made by politicians and making it harder for politicians to use personal law-based appeal to gain votes;

Article 15(3) of the Indian Constitution allows the state to make special laws for women because, till today, personal laws are still mostly misused due to patriarchal societal norms and improper legislation. The freedom to practise and profess any religion under Article 25 cannot justify in any way the infringement of basic human rights of women. Many personal laws relating to marriage, divorce, succession, and inheritance among various communities remain unjust and discriminatory towards women. The existence of these sexist laws has led to the incorrect treatment of women by a male-dominated society. By enforcing a Uniform Civil Code, the condition of Indian women will be enhanced, their rights will be protected, and the elimination of discriminatory personal laws will take place. This will in turn promote gender equality and advance the goal of equal rights for women throughout the territory of India.

The Preamble of the Indian Constitution declares India to be a secular nation. The implementation of a Uniform Civil Code across India ensures that all Indian citizens, regardless of whether they follow Hinduism, Islam, Christianity, or Buddhism, are governed by the same set of civil laws. It also helped to eliminate religious discrimination and align with the core principles of secularism. It is important to note that the Uniform Civil Code would not infringe on individuals’ freedom to practise their religion but help to eliminate discrimination on the basis of religion and bring together all citizens under a single civil legal framework;

The fundamental right to practise any religion permits each religion to independently manage its own personal matters. However, this religion-based classification contradicts the right to equality guaranteed by Article 14 of the Indian Constitution. Implementing a Uniform Civil Code would promote equality by applying a consistent set of civil laws to all citizens, irrespective of their religion, thereby ensuring equal treatment before the law;

The various personal laws of different communities are undermining India by creating inequalities. These varying and often conflicting personal laws contribute to inequalities. Introducing a Uniform Civil Code would address these conflicts and inconsistencies, promote national integration within India, and support the concept of “One Nation, One Flag, and One Law”;

The personal laws of any religion are the traditional regulations governed by religious practices, with many existing laws that originated centuries ago and hold an orthodox character. Many of these laws are outdated and are not in consonance with contemporary society. Implementing a Uniform Civil Code would address the issues related to these outdated laws by either eliminating or restricting them, modernising our civil law system.

Challenges in implementing the Uniform Civil Code

Article 44 of the Indian Constitution is still not implemented due to various challenges, which are as follows:

India’s diversity encompasses a wide range of religions, cultures, and traditions, which presents a significant challenge in implementing a Uniform Civil Code. The challenge lies in balancing this variety while providing a consistent legal framework. Thus, it is challenging for the beliefs and sentiments of every section of society when establishing a standard law that brings together all these diverse groups;

Many people in India lack understanding about the Uniform Civil Code and often fear that its implementation would infringe their religious sentiments and restrict religious practices. The primary goal of the Uniform Civil Code is to promote equality by ensuring that all Indian citizens are treated equally within society;

A key challenge for the central authorities is to reassure every religious group and community that the implementation of the Uniform Civil Code will be conducted in good faith and with a bona fide intention, without imposing the will of the majority on the minorities;

The diverse range of religions in India often leads to the politicisation of this issue, complicating efforts to implement the necessary changes. This results in several obstacles in the process of enacting the Uniform Civil Code;

By implementing a Uniform Civil Code for all the communities and religions, it could result in facing opposition from certain political parties, undoubtedly limiting the smooth development and enforcement of the Uniform Civil Code;

The implementation of a Uniform Civil Code in India will necessitate amendments to various constitutional provisions. This process will require substantial political consensus and effort, which can be difficult to obtain;

Creating a comprehensive Uniform Civil Code that addresses personal laws related to marriage, divorce, inheritance, and other matters while ensuring fairness and equality is a legally complex task;

One of the key goals of the Uniform Civil Code is to promote gender equality. However, this objective may face resistance due to entrenched traditional and patriarchal norms in different communities;

Even if the Uniform Civil Code is enacted, ensuring its effective enforcement and implementation, especially in remote and culturally conservative areas, can be a challenging and lengthy process;

As India is a signatory to various human rights conventions, ensuring that the implementation of the Uniform Civil Code aligns with these international obligations adds another layer of complexity;

There may also be an increase in legal disputes as personal laws would be standardised. Given the existing significant backlog of cases in India, this could aggravate the situation.

Is there a need of Uniform Civil Code

The need for implementing a Uniform Civil Code is rooted in the principles of the Preamble of the Indian Constitution, which provides for ensuring to the people of India equality, liberty, fraternity, and secularism. The different religious practices done by people of different religious communities bring disparities and discrimination, particularly against women. The Uniform Civil Code will eliminate all kinds of disparities prevalent in different personal laws and ensure equality for all citizens. It will also help India fulfil its international obligations regarding human rights and gender equality. The Parliament of India made an attempt to bring into effect the Uniform Civil Code in India by introducing a Bill in the year 2019.

Uniform Civil Code Bill, 2019

The Uniform Civil Code Bill, 2019 was introduced in the Lok Sabha on 25 October, 2019. The Bill seeks to create and establish the National Inspection and Investigation Committee for the preparation as well as implementation of the Uniform Civil Code throughout India. Section 4 of the Bill provides for the National Inspection and Investigation Committee. The Committee will be responsible for taking any measures necessary for the codification and implementation of the Uniform Civil Code throughout the Indian territory. The Committee shall ensure the following:

The Uniform Civil Code Bill, 2019 is intended to apply throughout India;

The Bill uniformly governs laws related to marriage, divorce, succession, adoption, guardianship, and the partition of land and assets for all citizens, without discrimination;

It aims to uphold the right to equality guaranteed under Article 14 and prohibits discrimination based on religion, caste, or gender, as outlined in Article 15 of the Indian Constitution; and

Additionally, the Bill seeks to replace existing personal laws, which are based on religious texts and traditions, with the Uniform Civil Code.

Advantages of the Uniform Civil Code Bill, 2019

The Bill ensures that all citizens are governed by the same legal framework, i.e., promoting equality and fairness;

The Bill contains a single set of laws. This would simplify legal process, thereby reducing complexity and confusion that arises due to multiple personal laws practices;

The Bill bridges the gap between different communities, bringing a sense of national identity and unity;

The Bill tries to bring into effect gender equality.

Disadvantages of the Uniform Civil Code Bill, 2019

Resistance from communities with deep-rooted personal laws and traditions might not readily follow the provisions of the said Bill;

The complexities involved in harmonising personal laws is challenging because it would require significant legal and administrative changes. It might lead to legal ambiguities;

The Bill does not fully accommodate the diverse needs and practices of all communities;

The Bill could become a politically charged issue, leading to polarised debates.

Portuguese Civil Code, 1867

The Uniform Civil Code in the state of Goa is based on the Portuguese Civil Code, 1867. In Goa, Hindus, Muslims, and Christians are all subject to the same uniform laws regarding marriage, divorce, and succession. The Goa, Daman, and Diu Administration Act, 1962, enacted after Goa became a union territory in 1961 (now a state), authorised the application of Portuguese Civil Code, 1867, in Goa, with provision for amendments and repeals by the relevant legislative authority.

Features of the Portuguese Civil Code, 1867

The Uniform Civil Code of Goa has the following features:

The Uniform Civil Code of Goa allows an equitable distribution of wealth and income between the spouses and their children, irrespective of their gender;

It is mandatory to register the birth, marriages, and deaths of each and every individual. It also prescribes various provisions relating to divorce;

The Indian Muslims whose marriages are registered are under a restriction to practise polgamy and triple talaq;

All the assets acquired by either of the spouses at the time of marriage are considered joint property. Upon divorce, each spouse is entitled to receive half of the property. In the event of death, the surviving spouse inherits half of the deceased’s property;

The parents cannot be completely disqualified to inherit from their property. There exists a law in favour of the children to inherit at least half of their parent’s estate, with the inherited property being divided equally among them.

Defects of the Portuguese Civil Code, 1867

There exist under the Goa Uniform Civil Code certain limitations. They are as follows:

Catholics in Goa are provided with specific privileges, i.e., exemption from registering the marriage and the authority of Catholic priests to dissolve marriage. The Catholic couples can solemnise their marriage in church by obtaining a ‘No Objection Certificate (NOC)’ from the Civil Registrar. In contrast, individuals of other religions in Goa must depend exclusively on civil registration as proof of their marriage. If a marriage between the Catholic couple is not consummated, a church tribunal can declare it null and void. However, non-Christians must seek a divorce through the courts and cannot use non-consummation of marriage as a basis for divorce;

The Uniform Civil Code of Goa allows a specific form of polygamy for Hindus in Goa but does not extend the Shariat Act, 1937, to Muslims in Goa. Rather, Muslims are governed by both the Portuguese law and the Shastric Hindu law. The law does not allow bigamy or polygamy for any group, including Muslims, except that a Hindu man is permitted to remarry if his wife does not give birth to a child by the age of 21 years or a male child by the age of 30 years. Any divorce granted by ecclesiastical (Church) authorities is considered valid for civil purposes, whereas non-Catholics can obtain a divorce only through a civil court. It is necessary for the husband to formally divorce his wife to remarry. This in turn has led to Muslim men entering into secret relationships and deserting their dependent wives. If a woman considers her own religious law as the sole authority on marriage and divorce, she may consider herself isolated by the legal system, as her divorce will not be legally recognised and prevent her from remarrying;

In the cases of divorce, a husband has a right to divorce his wife if she is caught having an affair. This right is, however, not granted to the wife. The wife has only a right to claim a separation due to her husband’s infidelity if it has caused a scandal in the public. A divorce can only be obtained by the wife if her husband brings his mistress into their home or when her husband abandons her. Christian Catholics who solemnise their marriage in the church are not subject to the civil divorce laws. Individuals belonging to the other religions can seek divorce for any reason, except for the Hindus, who can only obtain a divorce if their wife has committed adultery; and

In cases involving property, both the husband and wife have joint ownership of assets, but the husband has to manage it. However, the husband still does not have the right to sell the house without his wife’s consent. It is made sure that the property is equally divided amongst the couple, but this applies only if each spouse’s family owns property. If the husband does not hold ownership rights in the property, the division of property during a divorce would result in the wife receiving half of nothing.

The first part addresses laws related to marriage and divorce;

The second part covers succession laws, which are further divided into intestate and testamentary succession;

The third part pertains to live-in relationships; and

The fourth part deals with provisions for repeals. The Act applies throughout Uttarakhand and also to residents living outside Uttarakhand.

Features of the Uniform Civil Code of Uttarakhand, 2024

Some of the important provisions of the Uniform Civil Code of Uttarakhand, 2024 are as follows:

The Uniform Civil Code puts a complete ban on polygamy, nikah halala, iddat, triple talaq, and child marriage;

It provides for establishing a uniform marriageable age for women and men across all religions. The minimum age for marriage of a woman is 18 years, and in the case of a man, the age of 21 years. In case of a breach of such condition, an imprisonment of 6 months is imposed and/or a fine of Rs. 25,000 is payable;

The Code necessitates to register a marriage solemnised between the couple within 60 days of marriage, or a fine of Rs. 10,000 is payable in case of non-registration of marriage solemnised after the implementation of the Uniform Civil Code of Uttarakhand;

In case of a dissolution of marriage taking place in contravention of the Uniform Civil Code rule, it is punishable with up to 3 years of imprisonment;

It is necessary for live-in couples to register their relationship within one month. The Registrar has the authority to validate their relationship legally;

The children born of a live-in relationship are to be considered legitimate;

At the time of termination of a live-in relationship, it is necessary for the couple to bring this notice to the concerned officials;

If the male live-in partner abandons the female live-in partner, the women can seek maintenance through the appropriate court;

Both parties to the marriage have been given an equal right to dissolve their marriage through a decree of divorce, and a divorce can only be granted through the proceedings of the court;

For succession laws, the Uniform Civil Code designates the primary heirs as the parents, children, and spouse;

At the time of divorce or a domestic dispute between the couple, custody of the child up to the age of 5 years will always be awarded to the mother;