This article is written by Adv. Vijay Shekhar Jha.

Table of Contents

Understanding circular trading

Circular Trading refers to issuing invoices in transactions among multiple companies (more specifically entities registered under GST) without the actual supply of goods. This is done with the intention to illicitly receive input tax credit (for brevity “ITC”) as available in the GST regime. Thus, Circular Trading is a type of circuitous transactions where a registered entity (mostly companies) attempts to create a flow of sham transactions with the connivance of other entity/ies by producing fake invoices.

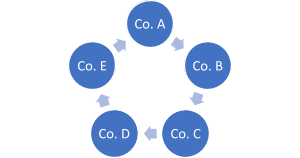

In this regard, pictorial transactions illustrated below show the simple circuitous transactions that are generally entered by companies involved in circular trading. The diagram below depicts the situation where Company A to E are engaged in Circular Trading and where there only circular flow of invoices and documents so as to claim ITC without involving the supply of goods/services.

Diagram 1: Transactions involved in a circular trading

To better appreciate this concept, it would be apt to advert to Section 16 (2) of the CGST Act, 2017 which stipulates the conditions that need to be satisfied for claiming ITC under GST regime. The relevant portion of Section 16(2) has been reproduced below for easy reference:

(2) Notwithstanding anything contained in this section, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless:

(a) he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

(b) he has received the goods or services or both.

Explanation — For the purposes of this clause, it shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise;

(c) subject to the provisions of section 41, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilisation of input tax credit admissible in respect of the said supply; and

(d) he has furnished the return under section 39.

(Note: The conditions (a) to (d) as elucidated above needs to be fulfilled cumulatively for claiming ITC under GST regime.)

From the bare perusal of condition (b), as reproduced above, it follows that the person who is claiming ITC must also have received the goods or services or both. In absence of physical possession of the goods, as per Section 16(2)(b) of the Act, ITC cannot be claimed. It is at this point that the concept of circular trading arises, where an entity claiming the ITC though may fulfil other conditions, however, do not have the possession of the good(s).

Provisional attachment in cases involving circular trading

Under GST regime, provisional attachment has been discussed under section 83 of the CGST Act, which provides that:

- Provisional attachment to protect revenue in certain cases:

(1) Where during the pendency of any proceedings under section 62 or section 63 or section 64 or section 67 or section 73 or section 74, the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue, it is necessary so to do, he may, by order in writing attach provisionally any property, including bank account, belonging to the taxable person in such manner as may be prescribed.

(2) Every such provisional attachment shall cease to have effect after the expiry of a period of one year from the date of the order made under sub-section (1).

From the perusal of Section 83 of the CGST Act, it is clear that this provision can only be invoked to protect the interest of the Government Revenue. Thus, cases where ITC has been wrongly claimed by the accused entity, however, if it does not cause any harm to the interest of the Government Revenue i.e. the situation is ‘Revenue Neutral’, no provisional attachment of property of such entity (including Bank Account) can be caused. This view is further reinforced by the decision given by the Indian Courts (esp. Hon’ble Gujarat High Court) in the following cases:

In H M Industrial Pvt Ltd vs. Commissioner, CGST and Central Excise[2], Hon’ble Gujarat High Court held that:

- Under section 83 of the CGST Act, the Commissioner is empowered to order provisional attachment for the purpose of protecting the interest of the Government revenue. In the facts of the present case, while a liability of Rs.14.62 crores had been estimated at the time when the order under section 83 of the CGST Act came to be passed, the present estimate is Rs.16.24 crores. Thus, the petitioner, upon conclusion of any proceedings that may be taken pursuant to the proceedings under sections 67, 73 or 74 of the CGST Act, may be liable to pay such amount. Admittedly, the petitioner has already reversed input tax credit to the tune of Rs.13,28,00,000/. In the opinion of this Court, considering the amount paid by reversing input tax credit, the interest of the Revenue is sufficiently secured. Therefore, the provisional attachment of the above referred bank accounts of the petitioner is no longer justified.

- For the foregoing reasons, the petition succeeds and is, accordingly, allowed. The respondent is directed to forthwith release the provisional attachment over the petitioners bank accounts being current accounts bearing No.02950500013045, 02950200000772 maintained with the Bank of Baroda, Kapadwanj, accounts No.917020026366404 and 917040037200382 maintained with the Axis Bank, Nadiad and accounts No.50200024114832 and 50200033690085 maintained with HDFC Bank, Kapadwanj as well as accounts No.02950600021450, 02950600021591, 02950600021899, 02950600022187, 02950300039429 and 02950300040500 maintained with the Bank of Baroda. Rule is made absolute accordingly.”

In the case of M/s Patran Steel Rolling Mill v. Assistant Commissioner of State Tax, Unit 2[3], Co-ordinate Bench of the Hon’ble Gujarat High Court pertinently observed that:

“6. From the facts as emerging on record, it appears that the tax liability of the petitioner in terms of the goods seized as well as the transporter’s statement, the same would not exceed Rs.13,00,000/. The petitioner has already deposited a sum of Rs.17,00,000/- with the respondent. Insofar as the amount assessed towards the penalty is concerned, in the absence of any proceedings having been undertaken under the provisions of the GGST Act as well as any penalty having been imposed, in the opinion of this court, the respondent authorities were not justified in resorting to such a drastic coercive measure of attachment of the bank accounts and seizure of goods, which results in bringing the business of the petitioner to a grinding halt.

7. Subsection (1) of section 83 of the GGST Act provides that where the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue, it is necessary so to do, he may, by order in writing attach provisionally any property, including bank account, belonging to the taxable person. On a plain reading of the said provision, it is evident that before resorting to such drastic action, the Commissioner is required to form an opinion that it is necessary to do so to protect the interest of the revenue. For the purpose of arriving at such an opinion, the Commissioner should first form an opinion that the petitioner would not be in a position to pay the tax dues after the assessment proceedings are over. In the facts of the present case, the petitioner firm is a going business and the petitioner has readily deposited a sum of Rs.17,00,00/which covers more than the tax liability that may be assessed. It is not the case of the respondents that the petitioner is a fly by night operator or that it does not have the means to pay the dues that might be assessed at the end of assessment proceedings, which at present have not even been commenced. There is nothing to show that the respondents would not be in a position to recover any amount that the petitioner may ultimately be held liable to pay. In these circumstances, without recording any such satisfaction, the respondent could not have formed the opinion that it was necessary to resort to provisional attachment to protect the interest of the Government revenue. The impugned order of attachment, therefore, cannot be sustained. It is clarified that the fact that the petitioner has deposited a sum of Rs.17,00,000/- during the course of the search proceedings shall not be construed as an admission of such dues on the part of the petitioner.

8. Before parting, the court deems it fit to caution the concerned authorities that while exercising powers under section 83 of The GGST Act, the authorities should try to balance the interest of the Government revenue as well as a dealer to ensure that while the interest of the revenue is safeguarded, the dealer is also in a position to continue with his business, because it is only if the dealer continues with the business that he would generate more revenue. The authorities should keep in mind that bringing the business of a dealer to a halt does not in any manner serve the interest of the revenue. Therefore, while taking action under section 83 or 67(2) of the GGST Act, the concerned authorities should take care to ensure that equities are maintained and while securing the interest of the revenue, they should attempt to see that the dealer is in a position to continue with the business. This court does not intend to lay down any absolute proposition that in no case drastic action should be taken, but that the respondents should consider the background and history of the dealer as well as his financial position to ascertain as to whether or not he would otherwise be in a position to pay the dues that may be assessed upon the culmination of any assessment proceedings that may be initiated. If the dealer is a fly by night operator or a habitual offender or does not have sufficient means to pay the dues that may arise upon assessment, such action may be justified. Such drastic powers under section 83 of the Act should not be exercised as a matter of course, but only after due application of mind to the relevant factors.”

The Hon’ble court had the occasion to consider Section 83 of the State GST Act, 2017 at length in the case of Valerius Industries vs Union of India[4], wherein the Hon’ble Court after an exhaustive discussion on the subject, summarized its final conclusions as under:

[1] The order of provisional attachment before the assessment order is made, may be justified if the assessing authority or any other authority empowered in law is of the opinion that it is necessary to protect the interest of revenue. However, the subjective satisfaction should be based on some credible materials or information and also should be supported by a supervening factor. It is not any and every material, however vague and indefinite or distant, remote or far fetching, which would warrant the formation of the belief.

[2] The power conferred upon the authority under Section 83 of the Act for provisional attachment could be termed as a very drastic and far reaching power. Such power should be used sparingly and only on substantive weighty grounds and reasons.

[3] The power of provisional attachment under Section 83 of the Act should be exercised by the authority only if there is a reasonable apprehension that the assessee may default the ultimate collection of the demand that is likely to be raised on completion of the assessment. It should, therefore, be exercised with extreme care and caution.

[4] The power under Section 83 of the Act for provisional attachment should be exercised only if there is sufficient material on record to justify the satisfaction that the assessee is about to dispose of wholly or any part of his / her property with a view to thwarting the ultimate collection of demand and in order to achieve the said objective, the attachment should be of the properties and to that extent, it is required to achieve this objective.

[5] The power under Section 83 of the Act should neither be used as a tool to harass the assessee nor should it be used in a manner which may have an irreversible detrimental effect on the business of the assessee.

[6] The attachment of bank account and trading assets should be resorted to only as a last resort or measure. The provisional attachment under Section 83 of the Act should not be equated with the attachment in the course of the recovery proceedings.

[7] The authority before exercising power under Section 83 of the Act for provisional attachment should take into consideration two things: (I) whether it is a revenue neutral situation (ii) the statement of “output liability or input credit”. Having regard to the amount paid by reversing the input tax credit if the interest of the revenue is sufficiently secured, then the authority may not be justified in invoking its power under Section 83 of the Act for the purpose of provisional attachment.”

Very recently, the Hon’ble Court in Pranit Hem Desai vs Additional Director General &Ors[5] held that:

- Section 83 of the State GST Act empowers the Assessing Authority to make a provisional attachment of any property of the assessee during the pendency of any proceeding for the assessment or reassessment of any turnover, even though there is no demand outstanding against the assessee, if he is of the opinion that it is necessary to do so to protect the interest of the revenue. This provision has been made, in our opinion, in order to protect the interest of the revenue in cases where the raising of demand is likely to take time because of the investigations and there is apprehension that the assessee may default the ultimate collection of the demand. In other words, Section 83 gives a power to be exercised during the pendency of any proceeding for assessment or reassessment, so that the assessee may not fritter away or secrete his resources out of the reach of the Commercial Tax department when the assessment or reassessment is completed. The expression “for the purpose of protecting the interest of the revenue” occurring in Section 83 of the Act is very wide in its meaning. Further, the orders of provisional attachment must be in writing. There must be some material on record to indicate that the Assessing Authority had formed an opinion on the basis thereof that it was necessary to attach the property in order to protect the interest of the revenue. The provisional attachment provided under section 83 is more like an attachment before judgment under the Code of Civil Procedure. It is a liability on the property. However, the power conferred upon the Assessing Authority under Section 83 is very drastic, far reaching power and that power has to be used sparingly and only on substantive weighty grounds and for valid reasons. To ensure that this power is not misused, no safeguards have been provided in Section 83. One thing is clear that this power should be exercised by the Authority only if there is a reasonable apprehension that the assessee may default the ultimate collection of the demand that is likely to be raised on completion of the assessment. It should, therefore, be exercised with extreme care and circumspection. It should not be exercised unless there is sufficient material on record to justify the satisfaction that the assessee is about to dispose of the whole or any part of his property with a view to thwarting the ultimate collection of the demand. Moreover, attachment should be made of the properties and to the extent it is required to achieve the above object[6]. It should neither be used as a tool to harass the assessee nor should it be used in a manner which may have an irreversible detrimental effect on the business of the assessee.

Whether circular trading is an offence under the GST regime?

Under GST regime engaging is ‘Circular Trading’ is an offence under Section 132 (1)(b), (c) of the CGST Act, 2017. And, as per Section 132 (5) of the Act, it is both cognizable and non-bailable offence. For convenience, relevant portion of Section 132 has been reproduced below:

- Punishment for certain offences:

(1) Whoever commits any of the following offences, namely:

(a) * * *

(b) issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilisation of input tax credit or refund of tax;

(c) avails input tax credit using such invoice or bill referred to in clause (b);

* * *

(5) The offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) and punishable under clause (i) of that sub-section shall be cognizable and non-bailable.

In this regard, it is important to advert to answer to Question 30 at the page 431 of the ‘FAQs on GST’ issued by CBIC[7]. Relevant portion of the same has been reproduced below:

- Q. 30 What are cognizable and non-cognizable offences under CGST Act?

Answer: In Section 132 of CGST Act, it is provided that the offences relating to taxable goods and /or services where the amount of tax evaded or the amount of input tax credit wrongly availed or the amount of refund wrongly taken exceeds Rs. 5 crores, shall be cognizable and non bailable. Other offences under the act are non-cognizable and bailable.

Thus, from above, it is clear that whosoever engages in the circular trading of worth exceeding Rs. 5 crores may be arrested even without warrant. Therefore, it becomes essential to get aware of the position that the Indian Courts have adopted so far on the issue of bail pre & post arrest where a person has been accused of an offence of indulging in ‘Circular Trading’.

Pertinent cases on the issue of bail pre & post arrest

At this juncture, it will be pertinent to take note of following cases which lucidly envelops the varying views of the Indian Courts while tackling the issue ‘whether bail/anticipatory bail can be granted in cases involving circular trading?’

- On imposing the onerous conditions while granting bail

The Hon’ble Calcutta High Court in Sanjay Kumar Bhuwalka vs. UOI[8] decided the case in favour of the Petitioner whereby a sum of Rs.50 Lac was fixed as the bail bond amount with a condition to deposit Rs.39 crores to the Government Exchequer, since it was a cognizable offence and posed a serious threat to the economy of the country. It was thus held that the applicant cannot be put behind the bars during the entire investigation and the trial in the complaint. Thus, directions were issued for release on bail, subject to onerous conditions, as noticed above.

However, the Hon’ble Apex Court in Sreenivasulu Reddy vs. State of Tamil Nadu[9] was found averse to the practice of imposing onerous conditions for granting bail and held that the order directing the applicant seeking bail to deposit a sum of Rs.35 crores out of Rs.50 crores (total outstanding liability) by a bail order should not be a condition for granting bail as such condition would lead to effect of recovery of demand from the accused.

Relying upon various Supreme Court cases, Hon’ble P&H High Court in Ranjit Singh vs. State of Haryana[10] held that the direction issued by Additional Session Judge of furnishing bail bonds of Rs.50,00,000/- with one surety of like amount along with the direction to pay the outstanding liability of Rs.1,94,78,017/- along with interest was an onerous condition on right of the Appellant to get bail (considering the amount was below Rs. 5 Crore, thus, offence alleged to have been committed was bailable offence). Consequently, the Hon’ble Court set aside the condition of payment of Rs.1,94,78,017/- along with interest and reduced bail bonds of Rs.50 lakhs with one surety to Rs.25 lakhs (which was ordered to be in the form of immovable property).

- Passing on of ITC of worth exceeding Rs. 5 Cr without the supply of goods in a non-bailable offence

In Ashok Kumar vs. Commissioner CGST and Central Excise[11] the Appellant firm after availing the ITC of Rs.63.50 crores without any actual receipt of goods had also passed on the said ITC of Rs.63.50 crores to six firms, out of which five firms were closely held entities of the Appellant Firm inasmuch as proprietor or partner or a Director were common and were related to each other. Investigation also revealed that the above referred five firms had availed and passed on the said credit of Rs.63.50 crores to 360 other firms located in various parts of the country. In the recorded statement Managing Partner of the Applicant firm had accepted that the none of his firms had received goods from M/s Bajrang Traders (purported original supplier) on which invoices they had availed ITC of Rs.53.63 crores; and that none of his firms had made payment to M/s Jai Bajrang Traders. This statement was never retracted. Thus, the Managing Partner of the Applicant firm apprehending arrest filed an application seeking ‘Anticipatory Bail’ u/s 438 of the CrPC before Hon’ble Bombay High Court. In the said application the Appellant had also submitted that as per the scheme of the GST Act Section 122 to 138 of the Act are not applicable to “assessment” proceedings and Chapter-XIX and Chapter-XII are distinct and application of the provisions thereunder are distinct and not subject to each other.[12] Rejecting these arguments of the Appellant, Hon’ble Bombay High Court held that the contention of Revenue Department that fraudulent ITC claim of Rs.63.53 crores was a matter of grave concern and required thorough investigation was well-founded and in view of the fact that many of the vehicle numbers presented by the Appellant were bogus and vehicle’s registration date was later then the lorry receipt dates and in the larger interest of the public declined to exercise discretion under Section 439 of the CrPC and dismissed the application. This decision of the Hon’ble Bombay High Court was also affirmed by the Apex Court.[13]

References

[2] Special Civil Application No.1160 of 2019 decided on 21st February 2019] = 2019-TIOL-460-HC-AHM-GST

[3] 2018-TIOL-2937-HC-AHM-GST

[4] 2019-TIOL-2094-HC-AHM-GST

[5] 2019-TIOL-2129-HC-AHM-GST

[6] In this regard the Hon’ble Court relied on the decision of the Hon’ble Bombay High Court in Gandhi Trading v. Asst. CIT 3 reported in (1999) 239 ITR 337

[7] 3rd Edition: 15th December, 2018

[8] 2018 (362) ELT 568

[9] VII 2000 (2) CCR 96

[10] 2020-TIOL-1492-HC-P&H-GST

[11] 2020-TIOL-1388-HC-MUM-GST

[12] On this issue, two divergent views have been taken by High Courts. The divergence in the views of High Courts is best illustrated in the recent decision of the Hon’ble Madras High Court given in following two cases:

Hon’ble Madras High Court in Mahendra Kumar Singhi 2019 (5) TMI 310 held that prosecution can be launched prior to assessment and rejected the application for anticipatory bail of petitioners. However, just five days later, another bench of the same High Court in Jayachandran Alloy (P) Limited 2019 (5) TMI 895 –Madras High Court has held that Section 132 applies only after completion of assessment and not prior to that. The bench stated this is clear from the usage of the word ‘commit’ under Section 132 which mandates the revenue to fix the act of committal of the offence first before punishment is imposed.

[13] 2020-TIOL-150-SC-GST-LB

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications