This article has been written by Hemal Shah pursuing the Diploma in US Corporate Law and Paralegal Studies from LawSikho. This article has been edited by Amitabh Ranjan (Associate, LawSikho) and Dipshi Swara (Senior Associate, LawSikho).

Table of Contents

Introduction

Cryptocurrencies have been around for a long time, but they’ve sprung into popular acceptance and use from the last decade, serving as not just alternate means of payment for people, but also as time and cost-saving solutions for a wide range of business applications. Following the creation and popularity of cryptocurrencies such as Bitcoin, Litecoin, Ethereum, and others, hundreds of other cryptocurrencies emerged. Legacy financial services corporations like Goldman Sachs and JPMorgan, as well as digital titans like Facebook, have taken note of the technology and have begun creating their own cryptocurrencies in-house.

The United States has a generally favourable attitude toward the usage of Bitcoin and other cryptocurrencies, despite the fact that few official laws have been implemented. The Department of Treasury, Securities and Exchange Commission (SEC), Federal Trade Commission (FTC), Internal Revenue Service (IRS), and Financial Crimes Enforcement Network (FinCEN) have all differed in their definitions of “cryptocurrency,” as well as their stances on how regulation should be implemented.

Demarcation of cryptocurrency and blockchain

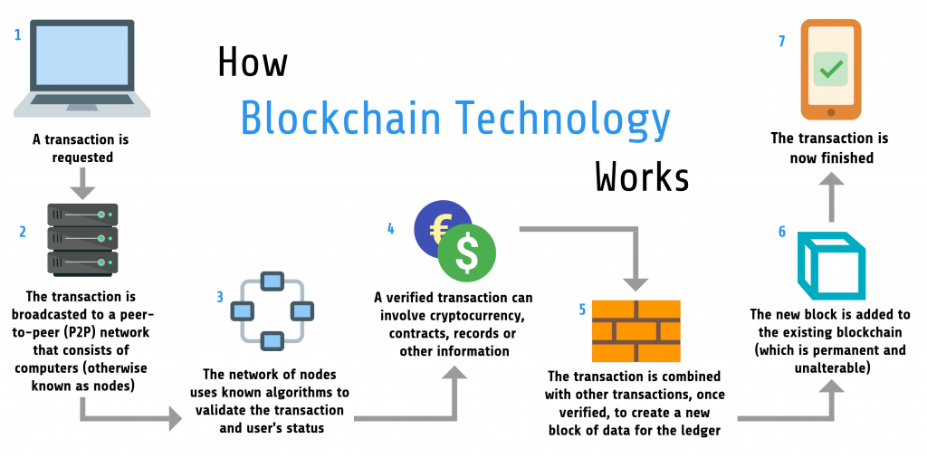

Blockchain

A blockchain is a decentralised ledger that records all peer-to-peer transactions. Participants can confirm transactions without the requirement for a central clearing authority using this technology. Fund transfers, trade settlement, voting, and a variety of other concerns are all possible uses.

Cryptocurrency

The terms “crypto” (data encryption) and “currency” combine to make cryptocurrency (medium of exchange). As a result, a cryptocurrency is a digital means of exchange (similar to traditional money) that employs encryption to maintain transaction security. Cryptocurrency is a digital currency that may be used instead of cash or credit cards.

Cryptocurrency is a form of digital or virtual money, to put it simply. It may be used like normal money, such as dollars, pounds, euros, yen, and so on. However, the cryptocurrency has no tangible equivalents in the shape of bills or coins that can be carried about; it only exists in electronic form.

Cryptocurrency a new mode of payment in the corporate world : Corporates keen on decentralisation

Bitcoin and other digital assets are being used by an increasing number of businesses throughout the world for a variety of investment, operational, and transactional purposes. There are unknown hazards, as with every frontier, but there are also incentives. According to Mathew McDermott, global head of digital assets at Goldman Sachs, crypto firms have had to “raise the bar” and ensure that their services are of “institutional grade,” allowing corporations to feel more comfortable dealing with crypto assets.

Companies that are focused on technology have been among the first to invest a portion of their balance sheet in digital currency. Square made a $50 million bitcoin investment in October 2020. Earlier this year, Tesla put $1.5 billion in bitcoin on its financial sheet. MicroStrategy purchased $475 million in bitcoin in the fourth quarter of 2020.

According to Anthony Day, blockchain partner at IBM Global Business Services, UK and Ireland, working with cryptocurrencies presents a problem for corporate treasurers because accounting standards were “not established with digital assets in mind or assets that are not physical in nature.” “The different regulatory and reporting systems for multinationals range substantially from country to country.”

“The realm of cryptocurrencies and digital assets has enormous promise for changing the way we transfer wealth and invest as organizations,” says IBM’s Day. “Programmability’s efficiency and automation might revolutionise cross-border trade, complicated supply chains, and intracompany settlement and reconciliation.”

Basic advantages of using cryptocurrency

Secured transaction

Due to constant frauds and manipulation in data, individuals have always strived to make the transactions extremely secured. Blockchain technology’s private keys and enhanced security helps businesses keep the transaction safe and secured. In addition, once the transfer is complete, it cannot be undone.

Privacy protection and business recognition

Privacy has always been the utmost concern for individuals online and with the march of technology, the privacy issue has been lying at the bay. In the modern world, if an organisation chooses to accept cryptocurrency, it has the attention of the individuals who want to stay anonymous with their identity and their respective transactions. On the other hand, these organisations are considered to be marching hand in hand with technology.

Decentralisation

For years, the organisations have been barred by the rules and the laws laid by the government of different countries. The transitions in the crypto are extremely private without any direct control of any legislature. The risk of assets and bank accounts being seized due to political instability is a clear and present concern for e-commerce firm owners in some nations. However, due to the decentralized structure of cryptocurrencies, this is not feasible. The money is kept in several locations across the world and may be recovered when needed.

Frictionless and cheap

Cryptocurrencies are also significantly less expensive in comparison. Cryptocurrency’s security feature eliminates the need for a third-party processor to validate and verify transactions. As a result, the obligatory transaction costs are reduced. There are, however, several decent third-party programs that can assist those who require a little direction or a tool to handle this aspect. However, even then, the costs are generally 1%.

Instant payment

For any online transaction that took place, there have been instances of it being time-consuming and extremely complicated. Cryptocurrency offers instant payment and barely any complications with its unique keys that are offered to each owner. The payment also converts the currency of your choice, thus eliminating the volatility risk.

Regulatory laws for carrying out cryptocurrency business in the USA.

There is no consistency in the treatment of firms dealing in virtual currencies (also known as “cryptocurrencies”) such as Bitcoin between states. When these entrepreneurs consider whether or not to operate within a state, one of the first questions they ask is whether or not current state money transmitter regulations apply to the selling or exchange of virtual currencies.

Some states have issued guidance, opinion letters, or other information from their financial regulatory agencies on whether virtual currencies are “money” under existing state rules, while others have enacted fragmentary legislation to specifically include or exclude digital currencies from existing definitions. The few states that have attempted to enact comprehensive regulations, such as New York’s much-maligned “BitLicense” scheme, have seen a mass departure of blockchain and virtual currency businesses from states that try to treat all virtual currency operators the same as traditional money transmitters, which are better equipped to deal with an overly restrictive regulatory framework.

The Financial Crimes Enforcement Network (FinCEN) does not consider cryptocurrencies to be legal tender, but it does consider cryptocurrency exchanges to be money transmitters since cryptocurrency tokens are “other value that substitutes for cash.”

The Internal Revenue Service (IRS) does not consider cryptocurrencies to be legal money, but rather describes it as “a digital representation of value that acts as a medium of exchange, a unit of account, and/or a store of value,” and has provided tax guidelines in this regard.

FinCEN

Cryptocurrency exchanges are lawful in the United States and are governed by the Bank Secrecy Act (BSA). In reality, this implies that bitcoin exchange service providers must get the necessary FINCEN license to execute an AML/CFT and Sanctions programme, keep relevant records, and report to the authorities.

In response to FATF recommendations issued in June 2019, FinCEN has stated that it expects cryptocurrency exchanges to comply with record-keeping obligations and the “Travel Rule” by disclosing information about the originators and recipients of cryptocurrency transactions.

The United States classifies virtual currency exchanges in the same legal category as traditional AML/CFT gatekeepers, financial institutions, and money transmitters, and so applies the same laws, including those included in the Bank Secrecy Act revisions enacted in 2021. (which has established its own version of the Travel Rule).

Money transmitter license

The Money Transmitter License is necessary if the firm plans to serve as an intermediary in transactions involving the exchange of cryptocurrencies for real money (cryptocurrency – fiat).

If a firm wishes to serve as an intermediary in transactions involving the exchange of one cryptocurrency for another (cryptocurrency – cryptocurrency), it must get an MSB (Money Service Business) License and review the criteria set out by each state’s legislation.

SEC (Securities and Exchange Commission)

The SEC’s method to determine whether a digital asset offered in a token sale is a security is based on the criteria laid out in SEC v. W.J. Howey Co. (the Howey Test). The Howey Test assesses whether an asset is an “investment contract,” one of the securities laws specified categories of instruments.

According to the criteria, an investment contract entails a monetary investment in a shared company in which the investor is taught to expect returns, and which is obtained from one or more third parties’ entrepreneurial or management activities. It makes no difference whether the business is speculative or non-speculative, or whether there is a sale of property with or without intrinsic value, if the criteria are passed. In a nutshell, the fundamental theme of this study is to concentrate on the economic realities of the arrangement in question.

Regulatory laws for carrying out cryptocurrency business in India

The difficulty to determine the legal status of cryptocurrencies is a major challenge in their regulation. Courts in various countries have classified cryptocurrencies as property, commodities, non-traditional currency, payment instruments, or money, depending on the interpretation of the legislation and the context.

The words “currency” and “money” are not defined under the Reserve Bank of India Act, 1934, the Banking Regulation Act, 1949, the Payment and Settlement Systems Act, 2007 (PSSA), or the Coinage Act, 2011.

The words “currency”, “currency notes”, “Indian currency”, and “foreign currency” are defined under the Foreign Exchange Management Act (FEMA). The IMAI decision acknowledged that the RBI might notify cryptocurrencies that fit under the category of “other comparable instruments” under the FEMA’s definition of “currency.” Since, India does not have a defined set of regulations for cryptocurrency, here are some regulations that companies need to adhere to before they commence the cryptocurrency business in India:

SEBI

Initial coin offerings may be regarded as a “security”, and therefore may fall under the regulatory purview of the Securities and Exchange Board of India (SEBI). The Securities Contract Regulation Act of 1956 (SCRA) does not include cryptocurrencies in its definition of “securities,” yet it may be regarded as security owing to the word’s comprehensive character, which covers “other marketable security.” If cryptocurrencies are created, distributed, and sold in a centralised manner, they might be called a “security.”

Commodity derivative

The SEBI’s September 2016 circular, which should be read in conjunction with the Ministry of Finance’s September 2016 and October 2019 circulars, does not expressly include cryptocurrencies in the list of notified products for the purposes of the SCRA’s phrase “commodity derivative.” However, under the aforementioned announcement, the central government may opt to classify cryptocurrencies as commodities. Indian crypto exchanges have lately petitioned SEBI rather than the RBI for regulation, claiming that crypto assets are commodities rather than money.

Direct tax

The 1961 Income Tax Act does not expressly address the taxation of cryptocurrencies. If considered an investment or business revenue, however, the sale of cryptocurrencies may be taxed as “capital gains.”

Indirect tax

If cryptocurrencies are classified as goods, they may be considered a “taxable supply” and hence subject to goods and services tax (GST). This understanding is reflected in a recent proposal to levy an 18 percent GST on bitcoin transactions.

Conclusion

The future of cryptocurrency is still very much up in the air. Critics see nothing but risk, while supporters see nothing but infinite possibility. It is critical that authorities build appropriate regulatory frameworks that foster the acceptance of cryptocurrencies and the growth of crypto-based trade, as well as procedures to preserve the financial system’s integrity, security, and stability.

Prudent regulation necessitates a thorough knowledge of the blockchain technology that underpins cryptocurrencies, as well as its potential to transform the global financial system. A realistic worldwide regulatory framework for cryptocurrencies requires cross-jurisdictional coordination and government-industry partnership.

References

- https://www.pwc.com/us/en/industries/financial-services/fintech/bitcoin-blockchain-cryptocurrency.html

- WEF_Navigating_Cryptocurrency_Regulation_2021.pdf (weforum.org)

- What we can expect from future cryptocurrency regulation worldwide | ZDNet

- Cryptocurrency as defined under draft bill – What Cryptocurrency Bill means for Indian buyers | The Economic Times (indiatimes.com)

- https://www.pwc.com/us/en/industries/financial-services/fintech/bitcoin-blockchain-cryptocurrency.html

- https://trade-leader.com/articles/cryptocurrency

- https://www.dummies.com/personal-finance/what-is-cryptocurrency/

- https://www2.deloitte.com/us/en/pages/audit/articles/corporates-using-crypto.html

- https://keap.com/business-success-blog/sales/e-commerce/cryptocurrency

- Legal status of cryptos in India | Developing a regulatory framework (law.asia)

Students of LawSikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications