This article is written by Abhinay Bhattacharya, pursuing a Diploma in Intellectual Property, Media and Entertainment Laws from LawSikho.

Table of Contents

Introduction

The work of a professional in any industry comprises of ups and downs and day to day challenges. Any unforeseen event can cause a person huge damage and loss. Thus, for such instances a contingency plan goes a long way.

Let us study the case of Rajeev Sharma for a distinct perception. Rajeev is an automotive designer and expert and is the Managing Director of a Graphic Designing and Architectural firm Blue Clouds. His work includes drawing model drafts, designing blueprints, creating base structures, product designing, consultancy and many more.

One of his clients, BNE, a car and automotive giant, hired the Blue Clouds services for the design and production of their new Streamline sports series car. The design was fancy and was totally distinguishable from the other cars in the market. The promotions and advertisements of the new car were done on the basis of the design layout and gradually Blue Clouds gained huge popularity and fame for their par excellence design.

After few months, one of their former clients, Newtin, sued Blue Clouds claiming that they have copied the design of the headlights, doors and roof from the model cars of Newtin and have duplicated them in the new cars of BNE.

The Blue Clouds argued that the similarity was minimal and a mere coincidence which naturally happens in this industry. But the court declared this as a copyright infringement and ordered Blue Cloud to compensate for the same.

Blue Clouds, having a Professional Liability Insurance policy, was protected from paying huge monetary losses not only for the damages but also for all the legal expenses incurred during the court proceedings.

Professional Liability Insurance (E&O Insurance) at a glance[i]

What is professional liability insurance

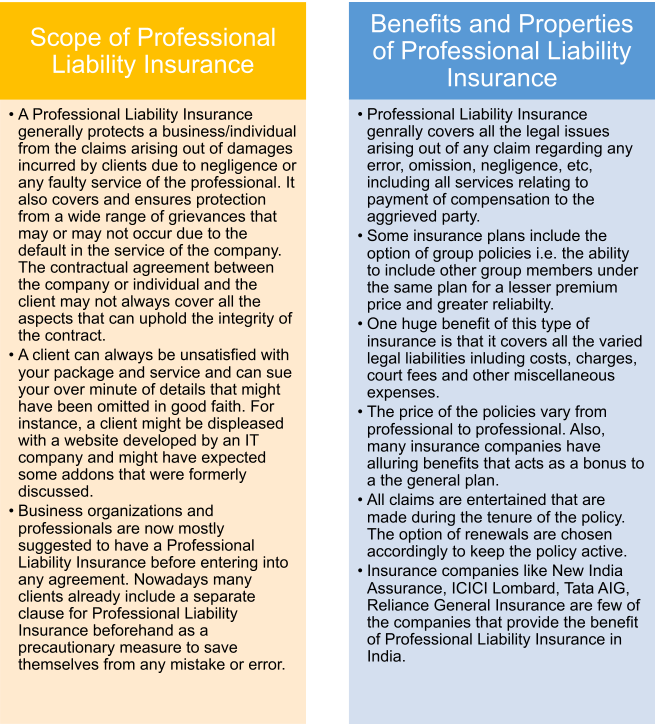

Professional Liability Insurance (or Professional Indemnity Insurance) is a type of insurance cover that is mostly used by business professionals and consultants. This type of insurance provides protection to the professionals against claims made by clients for any error or default in service by them. Professional Liability Insurance (PLI) covers any unforeseen or involuntary loss occurred to the client by the services of any individual and safeguards them from paying huge amounts of money from their own pockets.[ii] The relationship between a professional and his client can be jeopardized by any such event of monetary loss and can easily disrupt the fiduciary bond. Thus, this necessity is particularly afforded by every business organization and individual for the protection against any error or omission that has occurred unwillingly during disposal of their services.

Scope and Benefits of Professional Liability Insurance[iii]

Copyright infringement clause in professional liability insurance

In India, the concept of PLI is rarely used by individuals. Mostly medical professionals acquire such insurances as they are more prone to negligence or error and the risk and claim are equally huge. However, the Indian Contract Act, 1872 does define the term ‘Indemnity’ as a promise by one party to save another in case of any loss caused by the promisor or another person.[iv]

The PLI although not much popular among the leading industries in India but is surely a prerequisite before entering into any contract. The existing insurance policies in India cover wide range of professionals including doctors, lawyers, businessmen, designers, decorators, engineers and many more.[v]

Nowadays, the PLI policies already include a clause covering the claims arising due to intellectual properties.

-

Copyright Infringement: An Insight

The mere presence of any image, literary work, music, software, design, etc., which is freely available over any platform like the internet, newspaper, display boards, magazines, posters, brochures and other media, doesn’t make it exploitable according to our whims and fancies.[vi]

Without the permission and license of the owner of the image, literary work, etc., copy, use or reproduction of such an intellectual property for our own benefit would amount to infringement of copyright under The Copyright Act, 1957. Sections 13 and 14 of The Copyright Act, 1957 clearly state the meaning and purview of the term copyright and what all subsists under it. Section 51 of this act explains the provisions when there is an infringement of copyright. [vii]

The owner or licensor of the copyright on knowledge of such infringement can most probably sue the infringer and compensate a hefty sum of money. But in case you have a PLI policy then the scenario is totally different and favourable.

To know more about copyright please visit

-

Professional Liability Insurance: A Saviour

If an individual or company has acquired a PLI policy then the insurance company will protect the policy holder and cover all the claims that are arising due to error, omission, negligence or mistake.[viii]

In case there is a violation of copyright, the insurance will defend the policy holder against any such claim made that falls under the norms of the policy. There are two ways by which a business organization or individual would make the most out of these policies:[ix]

- The insurance company will be liable to defend the policyholder in every cost. It will look after the claims, expenses, dues, etc. made by the third party. The insurer also looks after the charges incurred during defending the policyholder in any court proceeding and covers all the costs and expenditures suffered.

- The insurer will cover the damages and indemnify the third party on behalf of the policy holder thus making good the loss.

-

Exclusions

The Insurance Company has all the right to refuse from compensating any loss made by the policyholder if such a claim is against the regulations of the policy, viz.:

- When the copyright infringement is intentional by the policyholder and not by any mistake, error, or good faith.[x]

- Claims arising out of any criminal act or violation of a criminal law.

- On account of breach of contract by the policyholder due to any reason as mentioned in the terms of the contract like wilful non-compliance, intoxication, act of god, etc.

- Nuclear perils and War, Contractual Liabilities, etc.[xi]

Scope of Professional Liability Insurance including Copyright Infringement[xii]

Existing laws and precedents governing professional liability insurance on copyright infringement

The face of Professional Liability Insurance is getting a new perspective in India. The legal industry is also shaking things up with an inclination to liability insurances. Nowadays, the top legal firms are spending millions on these insurances for their associates and is one of the major reasons for their spike in expenses after salaries.[xiii]

Although, in India this concept has now gradually started gathering moss, but still the potential picture lacks significant and notable hue. The notion got unwrapped after the Satyam Scam in 2009 when an accounting firm was held liable for its services to Satyam Computer Services Limited.[xiv] This shook the foundations of many firms in India and made them rethink their strategies. As needs are paving ways to demand, the inception of PLI in India has begun to firm its roots.

The laws in India regarding PLI in respect to Intellectual Properties (Copyright, Trademark, Trade dress, etc.) is still vague and flexible whereas the US have developed such regulations and principles and are now operating on such policies accordingly. The model of US is a perfect example to be harnessed in India which we shall look upon.

Risk faced by lawyers globaly and the cost of premiums paid for PLI[xv]

The Insurance Companies nowadays are amending their policies according to their benefits. The copyright claims by the policyholders result in thousands of dollars of damages which put a huge risk to the insurance companies as thousands of copyright infringement suits are being filed on a daily basis.[xvi]

Many insurance companies now have modified their clauses keeping in mind the ‘Advertising Injury’ aspect of the copyright claims. The companies have now revised the ‘Advertising Injury’ definition in their policies in such a manner that it mostly precludes the usual infringement acts.[xvii]

Likewise, now the Insurance Company policies consist of an exclusion clause to rule out the major Intellectual Properties in case of a claim of copyright infringement. Insurance Companies are now trying to evade the claims by changing their norms which is under their right, but in contrary poses a risk to the policyholders.[xviii]

-

Exclusion by courts: A Broad Interpretation

Not all Liability Insurance policies cover the aspect of Intellectual Property under their purview. Although there are several policies that are available for coverage, but many policies particularly state the exclusions of Intellectual Properties (Copyright, Trademark, Patent, etc.) within them.

Courts have interpreted the exclusions and categorized them broadly on the basis of the clauses mentioned in the policies. In the case of Finn v. National Union Fire Insurance Company of Pittsburgh, the policyholder Uniscribe Professional Services provided printing services to a law firm. The law firm had handed over the confidential documents to the printing firm for analysis. A relative of an employee of Uniscribe had leaked the confidential documents on the internet. Consequently, the law firm sued Uniscribe.[xix]

To settle the claim Uniscribe looked up to the Professional Liability Insurance company as a remedy. The insurer rejected the claim and stated that the policy excluded any claim arising out of Trade Secret. The Supreme Court stated that the plain language of the clause in the policy excluded the coverage of negligence of trade secrets committed by the third party. Moreover, the term ‘arising out’ should be read expansively and interpreted broadly.

In another case of Lemko Corporation v. Federal Insurance Company, claims against the theft of a copyrighted material made by the policyholder was refused by the insurer stating that the exclusion clause of ‘arising from Intellectual Properties’ in the policy barred the coverage of the insurance. The policyholder argued that many other claims apart from copyright in the complaint cannot be rejected on the same basis. [xx]

The District Court agreed with the insurer and held that the provision of ‘arising from’ has to be read broadly which engulfs all the claims.

The precedents of the courts still remain ambiguous at large and a definitive rule is a need of the hour.

-

Coverage in the face of Exclusions: A Silver Lining

There are cases where the courts have considered the prospects of coverage and have refrained from precluding the claims on negligence in respect to Intellectual Properties.

In the case of Hartford Fire Insurance Company v. Vita Craft Corporation, the insurance company Hartford Fire Insurance, alleged that the claims arising out of infringement of patent and negligence of trade secret were barred from coverage. Also, the insurer contended that the claims were arising from intellectual property that was excluded from the policy. The policy holder contended that there were claims for false allegations also that were not considered by the insurer.[xxi]

The US District Court ruled out that the policyholder was correct and stated that the insurer did not establish the fact that the exclusion of Intellectual Properties barred coverage and thus, the coverage was not under ambit of exclusion.

Similarly, in the case of MedAssets, Inc. v. Federal Insurance Company, the insurer contended that misappropriation of trade secrets was not liable for coverage and therefore the insurer Federal Insurance was under no burden to defend the policyholder for the same. [xxii]

The US District Court refuted the submission of the insurer and held that although ‘misappropriation of trade secrets’ was not under coverage but the ‘negligence in confidential information’ was barred from exclusion.

The views of the courts are surely a stepping stone for building a reliable structure of PLI laws.

Conclusion

The Professional Liability insurance acts as a guardian to the both the business organizations and individuals as it helps them from the liability of the claim and payment of huge compensations. The professionals are always at stake when dealing with such big client companies and the luxury of PLI acts as a messiah during these crises.

As the copyright infringement cases are on a rise, the monetary costs are also steeping with every claim. In order to safeguard themselves it is now a high time for individuals and professionals to make themselves aware of this insurance benefit and its perks. A setback in the daily course of business can hinder with the triumph to glory.

In India the concept of PLI is still emerging and now it’s a priority to develop strict laws and regulations that help the professionals during hard times. At present, with a lack of proper rules and precedents, the race has far more hurdles to be crossed. The model guidelines of the courts of US and UK regarding the interpretation of the laws of PLI assist our lawmakers and contribute to the framing of laws in India and are to be adhered to and implemented accordingly with time and necessity.

References

[i] Image courtesy: https://www.plancover.com/blog/errors-and-omission-insurance-even-the-most-successful-companies-require-it

[ii] https://www.policybazaar.com/corporate-insurance/articles/what-is-professional-indemnity-insurance/

[iii] Scope: https://securenow.in/insuropedia/professional-liability-insurance-protect-us-copyright-infringement-lawsuits/

Benefits: https://www.policybazaar.com/corporate-insurance/articles/what-is-professional-indemnity-insurance/

[iv] https://www.indiacode.nic.in/handle/123456789/2187?locale=en

[v] https://www.latestlaws.com/articles/analysis-of-professional-indemnity-insurance-in-india/#_ftnref13

[vi] https://securenow.in/insuropedia/professional-liability-insurance-protect-us-copyright-infringement-lawsuits/

[vii] https://www.indiacode.nic.in/handle/123456789/1367?locale=en

[viii] https://securenow.in/insuropedia/professional-liability-insurance-protect-us-copyright-infringement-lawsuits/

[ix] Id

[x] Id

[xi] https://www.turtlemint.com/general-insurance/articles/what-is-professional-liability-indemnity-insurance/

[xii] Image courtesy: https://www.slideshare.net/TrustedUnion/professional-liability-insurance-coverage

[xiii] https://www.livemint.com/Politics/fktltXhbtOrYenVJakZzHJ/Malpractice-insurance-catches-on-in-India.html

[xiv] Id

[xv] Id

[xvi] https://www.ipwatchdog.com/2016/06/13/insurance-exposed-risk-copyright-claims/id=70002/

[xvii] Id

[xviii] Id

[xix] https://www.ipwatchdog.com/2019/11/06/understanding-insurance-coverage-intellectual-property-claims/id=115632/

[xx] Id

[xxi] Id

[xxii] Id

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Great Article. Keep Up The Good Work. Love to read such Great Content which provides quality Knowledge as well as interesting facts.