This article is written by Pragya Agrahari of Amity Law School, Lucknow. This article provides a detailed analysis of Section 80GG of the Income Tax Act, 1961, that is, tax deductions on rent paid. It covers all the major aspects of this Section consisting of conditions to claim such deductions, how to calculate deductions, steps to file a declaration form, etc.

This article has been published by Sneha Mahawar.

Table of Contents

Introduction

The government provides us with a variety of public goods and services, and in order to balance its budgetary power, it is crucial to secure revenues, which largely come from the taxes the citizens pay to the government. Therefore, it is equally important to secure the willingness of the citizens to pay taxes and encourage investments in certain areas. In order to do so, it provides citizens with various incentives in the form of tax benefits like tax deductions, tax exemptions, etc. There are a total of 19 types of tax deductions the government provides on a variety of public goods and services. One of these is the tax deduction on house rent, which was provided under Section 80GG of the Income Tax Act, 1961, which will be discussed in detail in this article.

Section 80GG of the Income Tax Act

Section 80GG under Chapter VI-A of the Income Tax Act, 1961, provides tax benefits in the form of tax deductions on house rent paid by the individual. Under this Section, one can claim a deduction on the rent paid for the house by him. Here, ‘deduction’ means the reduction provided in the amount that will be subtracted from the total annual taxable income of an individual as an income tax. It usually applies to salaried individuals or self-employed individuals who are residing in rented accommodations and are not provided with the House Rent Allowance (HRA) from their employers. However, this tax exemption depends upon a variety of other factors like the amount of your salary, the city in which you are living, the house in which you are residing, the type of employee you are, the rent amount, etc.

The rationale behind the insertion of Section 80GG

This Section was inserted by the Finance Act, 1998 into the Income Tax Act, 1961. The main idea behind its insertion was to relieve the individuals who were not provided with any rent allowance and were living in rented houses. The deductions provided by the government on the rent paid for the rented houses reduce their total tax liability and make their lives much easier.

Conditions to claim tax deductions

Anyone meeting the following conditions can claim the deductions under this Section.

Claim by individual

Only an individual or an individual from a Hindu Undivided Family (HUF) can claim a deduction under this Section. It means a company or any other enterprise cannot claim any such right.

Individuals should be salaried employees or self-employed

Only individuals who get a salary from their employers or are self-employed are eligible to get these deductions under this section. It means if one has no source of income, he/she cannot avail of the benefit provided under this section.

Not be getting HRA or RFA

The most important condition to getting the benefits of this Section is that an individual should not be getting any special allowance to meet his/her expenditure for payment of rent for his/her accommodation. It means that if one is already provided with House Rent Allowance (HRA) or Rent Free Accommodation (RFA), he/she cannot claim the benefit of tax deductions on rent paid.

Not own any residential accommodation

The person who is seeking to avail themselves of this tax deduction should not own any residential accommodation at the place where he/she usually resides or carries out his/her business, profession, or duties of his/her office. Even his/her spouse, minor child, or, in the case of a Hindu Undivided Family (HUF), the members of his/her family should not own any such property at any such place. The individual should also not own any residential accommodation at any other place in his/her own occupation, provided that its value has been determined under clause (a) of sub-section 2 or clause (a) of sub-section 4 of Section 23 of the Act as self-occupied property.

Exceptions under Section 80GG of the Income Tax Act

There are some circumstances under which one cannot claim benefits under this Section. These are as follows:

- One cannot claim deductions on rent paid if he/she owns a house in the same city or place as his/her residence or workplace,

- One cannot claim deductions on house rent if he/she is already claiming benefits for an owned house as ‘self-occupied property’.

Deductions provided under Section 80GG of the Income Tax Act

The quantum of deductions on the rent paid available under this Section is as follows:

- Deduction of excess of 10% of his total adjusted income towards the payment of rent.

- Provided that such deduction will be granted to the extent that such expenditure does not exceed

- 5000 rupees per month or 60000 per year, or

- 25% of his total annual income, whichever is less.

Calculation of deductions (Examples)

Example 1

Suppose your friend Paritosh, who lives in Bangalore in a rented apartment, pays a rent of ₹10,000 per month. So, his total yearly rent will be ₹ 1,20,000. His total income is ₹ 5,00,000 per annum and he is not getting any HRA from his employer. How much deduction will he get on the rent paid?

On the basis of the above information:

- Excess of 10% of his total income with respect to rent payment= (Yearly rent – 10% of total income)= ₹1,20,000- ₹50,000= ₹70,000

- Extent of deduction as per the provision= ₹60,000 (₹5000 per month)

- 25% of total income= ₹1,25,000

Here, the lowest value of these three will be considered a deduction amount as per the Section. Hence, the deduction amount will be equal to ₹ 60,000.

Example 2

Suppose your friend Aisha, who lives in Chennai in a rented flat, pays a rent of ₹80,000 on a yearly basis. Her total income is ₹2,00,000 per annum and she is not getting any HRA from her employer. How much deduction will she get on the rent paid?

On the basis of the above information:

- Excess of 10% of his total income with respect to rent payment= (Yearly rent – 10% of total income)= ₹80,000- ₹20,000= ₹60,000

- Extent of deduction as per the provision= ₹60,000 (₹5000 per month)

- 25% of total income= ₹50,000

Here, the lowest value of these three will be considered a deduction amount as per the Section. Hence, the deduction amount will be equal to ₹50,000.

Example 3

Suppose your friend Shalu, who lives in Hyderabad in a rented house, pays a rent of ₹60,000 on yearly basis. Her total income is ₹1,80,000 per annum and she is not getting any HRA from her employer. How much deduction will she get on the rent paid?

On the basis of the above information:

- Excess of 10% of his total income with respect to rent payment= (Yearly rent – 10% of total income)= ₹60,000- ₹18,000= ₹42,000

- Extent of deduction as per the provision= ₹60,000 (₹5000 per month)

- 25% of total income= ₹45,000

Here, the lowest value of these three will be considered a deduction amount as per the Section. Hence, the deduction amount will be equal to ₹42,000.

Rule 11B of the Income Tax Rules, 1962

Rule 11B of the Income Tax Rules, 1962, prescribes the conditions to be fulfilled by the assessee before claiming a deduction under Section 80GG of the Act for the rent paid for furnished or unfurnished accommodation, that was used for his/her own residence. It makes it mandatory for an individual to file a declaration under Form 10BA to claim benefits under this section.

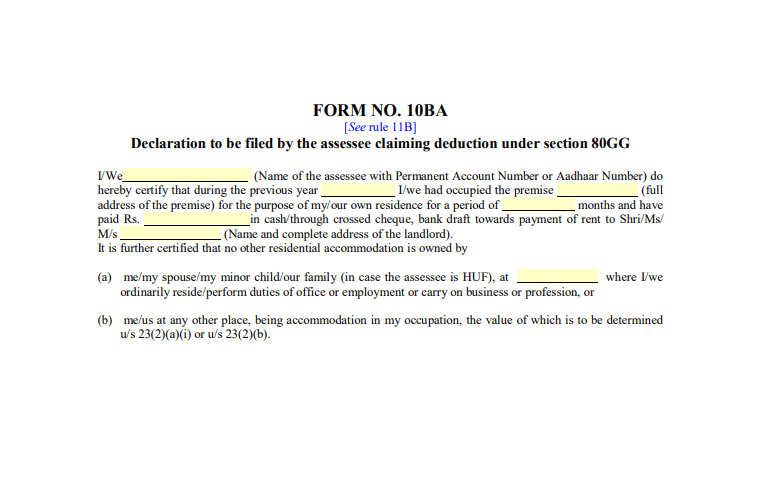

Form 10BA

In order to get benefits under Section 80GG, one has to fill out the declaration under Form 10BA with the necessary details related to rental property. It is a declaration containing all the details related to the rented premise in which the assessee resides and ensures that he/she does not own any other accommodation property, or, in the case of HUF, any members of his/her family.

The necessary information required to file the declaration is as follows:

- Name of the assessee,

- Permanent Account Number (PAN) or Aadhaar Number,

- Year of occupying the rental accommodation,

- Tenure of residency (in months),

- Full address of the rental premise,

- Rent amount with the mode of payment,

- Name and address of the landlord and landlord’s PAN (in case of rent amount> ₹1 lakh),

- The declaration that the assessee or his spouse or minor child or his/her family (in case of HUF) do not own any other residential accommodation.

Online filing of Form 10BA

One can also file the declaration under Form 10BA through an online procedure. Here are the steps you need to follow:

- Go to the Income Tax e-Filing portal ‘https://www.incometax.gov.in/iec/foportal/’,

- Login with PAN, or Aadhaar Number,

- Go to ‘e-File’ and choose ‘Income Tax Forms’ from the drop-down list and again choose ‘File Income Tax Forms’,

- Go to the ‘Others’ tab and select ‘Form 10BA’,

- Choose ‘Assessment Year’ and click ‘Continue’ and then ‘Let’s get started,

- Fill in the required ‘House property details’ and then fill in the ‘Declaration’ and click ‘Preview’,

- Verify your details and then ‘Continue’.

Conclusion

The government provides many deductions to reduce their tax liabilities on taxable income, from Section 80A to Section 80U of the Income Tax Act, 1961. But people are not aware of most of these provisions. One such provision is Section 80GG. Section 80GG strives to give relief to many individuals who are working as employees in any institution or are self-employed and living in big metropolitan cities with high-rent accommodations. It helps them reduce their taxable income on the rent paid for such accommodations. The only condition to be fulfilled is that they should not be getting HRA from their employees. In order to claim such benefits, one is required to file a declaration under Form 10BA in any way, whether offline or online.

Frequently Asked Questions

Can property owners claim benefits provided under Section 80GG of the Income Tax Act?

Property owners can also claim tax benefits under Section 80GG, provided that the property owned should be in the same city or place as his/her residence or workplace and he/she must be paying rent for the accommodation in which they currently reside. In such a case, the other property will be deemed “let-out property.” But if they are living in a rented apartment and own a property in the same city as well, they will not be eligible to claim a deduction under Section 80GG.

What is ‘total income’ as per Section 80GG?

‘Total income’ as per this Section means income excluding both long-term and short-term capital gains under Section 111A, income under Section 115A or Section 115D, and deductions under Section 80C to Section 80U.

Can non-resident individuals claim benefits under Section 80GG?

Yes, this Section is equally applicable to both resident and non-resident individuals.

Can an individual who is living with his parents claim deductions under Section 80GG?

Yes, an individual who is living with his parents can claim deductions under Section 80GG. But he has to sign a formal rent agreement with his parents showing his expenditure on rent. The consequence will be that his parents now have to show this income while filing an income tax declaration. But this will not be applicable if he is the co-owner of the property along with his parents.

References

- https://groww.in/p/tax/section-80gg

- https://tax2win.in/guide/claim-deduction-under-section-80gg-for-rent-paid

- https://www.bajajfinservmarkets.in/markets-insights/income-tax/income-tax-exemptions-deductions/section-80gg.html

- https://www.bankbazaar.com/tax/section-80gg-of-income-tax-act.html

- https://cleartax.in/s/claim-deduction-under-section-80gg-for-rent-paid

- https://www.coverfox.com/personal-finance/tax/section-80gg/

- https://housing.com/news/deduction-on-rent-paid-under-section-80gg/

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications