In this blog post, Hari Manasa Mudunuri, Student of University College Of Law, Osmania University and pursuing a Diploma in Entrepreneurship Administration and Business Laws by NUJS, describes the standard terms and policy for lending to SMEs by banks.

Introduction

SME means Small & Medium Enterprises, or sometimes also called the MSMES- Micro, Small & Medium Enterprise. The SME sector is a fast growing sector in India. They have succeeded in providing employment, have a relatively low cost of capital, provide complementary services to the Industrial sector. Their contribution to the GDP is about 8% and 40% of exports. SMEs allow for inclusive growth in the economy.

However, the SMEs in India face some problems, which could arise due to the smaller scale of production, technological backwardness, marketing deficiencies, lack of proper sales & distribution channels, increased competition, arm twisting by MNCs, shortage of capital, etc.

Given the population perspective and potential for employment generation, the government has recognized the need to improvise, protect and uplift the small players in the market too. The central government enacted the Micro, Small & Medium Enterprises Development (MSMED) Act, 2006 to give impetus to the growth of the industry. The Act provides mechanisms to structure the sector to address any governance or operational issues faced by the SMEs. These enterprises can raise the finances through bank loans, friends or relatives, sister concerns, equity funding, trade, credit, subsidy on capital by the government, money lenders, NBFCs, etc.

General Objectives Of SME Loans

- To improve flow of credit and hassle free credit to the MSME Sector

- To formulate liberal norms of lending to the MSME sector, to ensure availability of adequate and on time credit.

- To devise an organizational structure at all levels for handling the MSME credit portfolio in a focused manner.

- To comply with guidelines received from the RBI.

- Hassle-free credit to Micro and Small Enterprises.

- Cluster-Based approach for financing MSE.

- Increased Coverage under credit guarantee scheme of CGTMSE.

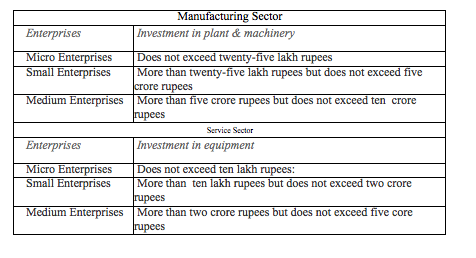

Definition

The Micro, Small & Medium Enterprise Development Act, 2006, has defined the term Micro, Small and Medium Enterprises into two classes:

- Manufacturing Enterprises

- Service Enterprises

(The limit on investment in plant and machinery/equipment for manufacturing/service enterprises, as follows):

RBI Guidelines

The RBI has issued a master circular containing the guidelines for commercial banks about the SME loans in India. The commercial banks include domestic as well as foreign banks operating in India. The Guidelines are.

- Advances to SME sector shall be calculated in computing achievement under the overall Priority Sector target of 40% of Adjusted Net Bank Credit (ANBC) or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher. [Where priority sector means a sector which impacts a large (weaker) section of the population.]

- Banks are advised to achieve a 20% year-on-year growth in credit to MSEs and a 10% annual growth in the number of micro enterprise accounts.

- To make sure that optimum credit is made available to micro enterprises, banks need to ensure that at least 60% of MSE advances should go to the micro enterprises. The target for lending to Micro Enterprises within the MSE sector will be calculated concerning the outstanding credit to MSE sector as on preceding March 31st.

Common guidelines/instructions for lending to MSME sector

- Banks are given instructions to compulsorily accept all applications from MSEM borrowers in India and to issue an Acknowledgment of Loan Applications.

- Collateral: Banks are instructed not to accept collateral security for loans up to Rs.10 lakh extended to the MSE sector. In case the MSE unit has a good track record, banks may extend the limit of allowance of a collateral prerequisite for loans up to Rs.25 lakh (after authorized approval).

- Composite Loan: Banks may sanction a composite loan limit of Rs.1 crore so that MSE entrepreneurs can avail of their working capital and term loan requirement through Single Window.

- Specialized MSME branches: Public sector banks have been instructed to have minimum one specialized branch in every district. Further, banks have been allowed to classify their MSME banking branches having 60% or more of their advances to MSME sector so as to encourage them to come up with more specialized MSME branches for providing improved service to this unit as a whole. The provisions of the Interest on Delayed Payments Act, 1998 to Small Scale and Ancillary Industrial Undertakings are applicable for payment.

- Bank loans to SMEs are Classified Under Priority Sector by the ACT as:

- Direct Finance:

- Manufacturing Enterprises – The MSEs engaged in the manufacture or production of goods to any industry specified in the first schedule to the Industries (Development and Regulation) Act, 1951. The manufacturing enterprises are defined regarding investment in plant and machinery.

- Loans for food and agro-processing- Loans for food and agro processing will be classified under Micro and Small Enterprises, provided the units satisfy investments criteria prescribed for Micro and Small Enterprises, as provided in MSMED Act, 2006.

- Service Enterprises -Bank loans up to 2 crores per unit to Micro and Small Enterprises engaged in providing or rendering of services and defined regarding investment in equipment under MSMED Act, 2006.

- Export credit to MSE units -(both manufacturing and services) for exporting of goods/services produced by them.

- Khadi and Village Industries Sector (KVI) -All loans sanctioned to units in the KVI sector, irrespective of their size of operations, location, and amount of original investment in plant and machinery. Such loans will be eligible for classification under the sub-target of 60 percent prescribed for micro enterprises within the micro and small enterprises segment under priority sector.

- Indirect Finance:

- Loans to persons involved in assisting the decentralized sector in the supply of inputs to and marketing of outputs of artisans, village and cottage industries.

- Loans to cooperatives of producers in the decentralized sector viz. artisans village and cottage industries.

- Loans sanctioned by banks to MFIs for on-lending to MSE sector as per the conditions specified in RBI circular

- Direct Finance:

- MSME Loan Policy covers all credit facilities to Micro and Small Enterprises (manufacturing and services) and other issues such as assessment of credit, margin norms, security requirements, coverage under Credit Guarantee Scheme, etc.

Guidelines on MSE Finance

All credit facilities to Micro Small Enterprises will be assessed as under. The sanctioning authority will consider all genuine requirements and it would be ensured that SME should not suffer for want of adequate credit.

Working capital requirements

Small (Manufacturing) Enterprises sector: Working Capital requirements of borrowers availing limit up to Rs.2 crore from Bank in the village and tiny Sectors ( now micro enterprises) are to be assessed as per TURN OVER Method.

Working capital requirements of Small Enterprise units to be assessed at 20% of the Projected Annual Turn Over up to a limit of Rs.5crore. If the credit requirement based on production / processing cycle is higher than the one assessed by the turnover method, the same may be sanctioned. Working Capital requirements of Small borrowers in the trade sector availing limits up to Rs.5crore are to be assessed by the turnover method.

General Traders including Stockist: The stockist procures stocks against payment, for resale. They would own the inventory, and their working capital requirements are large. While the past trends of holding levels can be taken as indicators, flexibility in lending norms will be required as the trading activity is subject to fluctuations depending upon the volatility in the market. The credit requirements will be assessed by past indicators and future projections as at present. The current ratio should normally be 1.10. Collaterals should cover the entire exposure to the extent of 50% minimum subject to the borrower maintaining adequate paid stocks to cover the limit. In the case of Trading accounts normally there will not be any long-term debts and therefore, TOL/TNW ratio to be considered. TOL/TNW ratio up to 4:1 shall be accepted. However, in deserving cases relaxation up to 6:1 may be permitted by RLCC (DGM) and above

SME Loan Procedure in Andhra Bank

As per the RBI guidelines and the Central Act, all the 27 nationalized banks provide loans to SMEs. In this paper, I choose to analyze the SME loan procedure in Andhra Bank.

Andhra Bank provides a basket of schemes for the SMEs. They designed the schemes based on the diversity of the entrepreneurs engaged in the business and also design the schemes conformable with the schemes introduced by the GOI for improving the overall inclusive growth of the economy. The following schemes are the schemes aimed at providing credit facility to the SMEs which factored, by and large, the overall requirements of the SMEs:

- Financing to MSEs- against property

- Term finance

- Non-fund based limits

- Artisan credit card scheme

- AB power tools (Shakthi)

- Technology up-gradation fund scheme

- Credit guarantee fund for small industries

- PavalaVaddi Scheme (4 % interest)

- AB doctor Plus

- Composite loan scheme

- Open cash credit

- AB Laghuudhyami credit card

- PM Employment Guarantee generation program

- National equity fund scheme of SIDBI

- Credit linked capital subsidy scheme for technology up gradation

- ALEAP &CGTSI for women

- Joint or Co- financing scheme

[divider]

References:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications