")

This article has been written by Siddha Lahoti pursuing a Remote freelancing and profile building program from Skill Arbitrage.

This article has been edited and published by Shashwat Kaushik.

Introduction

Tea is one of the most popular and widely consumed beverages in the world. The major tea growing countries in the world are India, China, Sri Lanka, Kenya and Indonesia. These five countries manufacture 77% of world tea and 80% of global export. Today, India is the world’s largest producer of tea, with two primary regions, Assam and Darjeeling. In the mid-19th century, the British introduced tea plants from China, and since then, tea has been the most significant industry in India, Nepal and Sri Lanka.

Supply chain of tea

India is the largest consumer of tea. Indian tea manufacturing is a lengthy process that starts with tea producers in tea gardens. The tea processors are tea factories where withering, rolling, fermenting, drying, blending and packaging are carried out. The tea is then sent to auctions, logistics and finally the retailers. The tea growing states in India are Assam, West Bengal in the north east and Tamil Nadu and Kerala in the south.

India manufactures two types of teas CTC (crush, tear, curl) and orthodox. CTC is used in low-quality products like tea bags as tea dust. 90% of India’s black tea is CTC, and 8.4% is orthodox tea, the rest is green tea manufacturing. 50% of Indian tea is grown in Assam state, and 90% of the tea grown in Assam is consumed domestically. Tea is broadly classified into two categories, black and green. But based on the processing, tea is classified as white, yellow, green, oolong and black. More than 97% of tea exported from India is black tea.

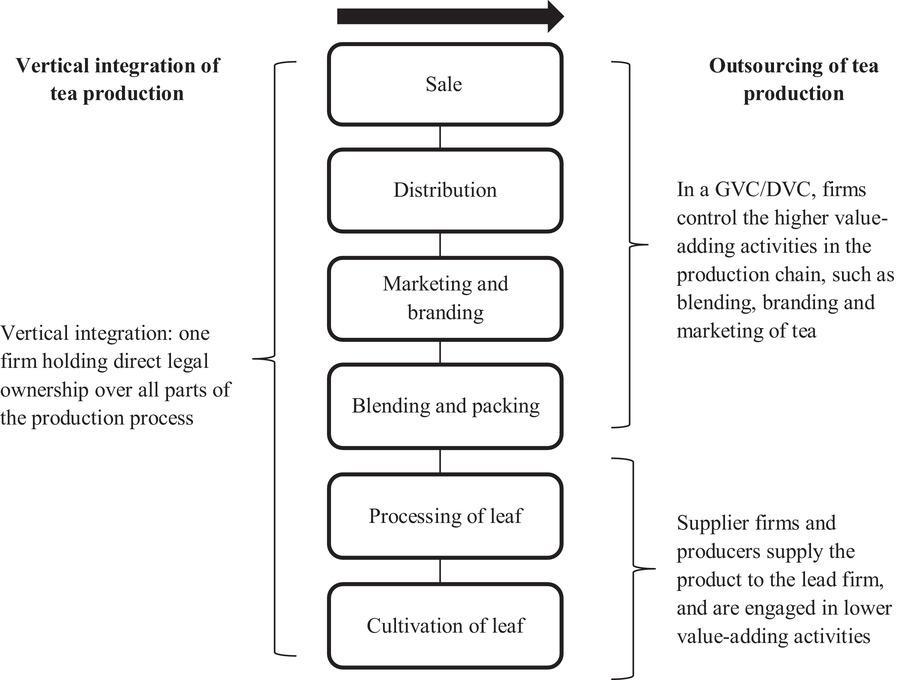

Three firms control one-fifth of the tea market. Unilever 12%, Tata Global Beverages 4% and Twinings 2% constitute a fifth of the global market. These firms source their products through a complex set of intermediaries, from producer to processor to blender. These inter-firm relationships contain significant degrees of power asymmetry, with implications for the capture of value at each stage of the production process. The Tea Board of India plays a crucial role in promoting and marketing Indian tea, both domestically and internationally. The supply chain of tea on the Indian subcontinent is a complex and fascinating process. It begins with the cultivation of tea plants in the lush, verdant hills of the region. The tea plants are carefully tended to and nurtured by skilled farmers who use traditional techniques passed down through generations. Once the tea leaves are mature, they are harvested by hand and transported to processing facilities.

At the processing facilities, the tea leaves undergo a series of steps to transform them into the finished product. First, the leaves are withered, which removes excess moisture. Then, they are rolled, which helps to release the tea’s flavour and aroma. The rolled leaves are then oxidised, a process that gives tea its characteristic colour and taste. Finally, the tea is dried and sorted into different grades.

The finished tea is then packaged and shipped to distributors and retailers around the world. Along the way, it may pass through several intermediaries, such as wholesalers and brokers. Each intermediary plays a vital role in ensuring that the tea reaches consumers in a timely and efficient manner.

The supply chain of tea in the Indian subcontinent is a global network that connects farmers, processors, distributors, and consumers from all over the world. It is a testament to the enduring popularity of tea and the ingenuity of the people who bring it to our cups.

Here are some additional insights into the supply chain of tea in the Indian subcontinent:

- Cultivation: Tea is grown in a variety of regions across the Indian subcontinent, including Assam, Darjeeling, and Nilgiri. Each region produces tea with its own unique flavour and aroma.

- Processing: The processing of tea is a delicate and time-consuming process. It requires skilled workers and specialised equipment.

- Distribution: Tea is distributed to consumers through a variety of channels, including supermarkets, specialty stores, and online retailers.

- Sustainability: The tea industry in the Indian subcontinent is facing a number of challenges, including climate change and the rising cost of labour. However, there are a number of initiatives underway to promote sustainable tea production.

Assam tea value chains

There are two supply chains of Assam Tea. One is that tea from large tea estates or small tree growers goes either to warehouses or to private factories. Tea factories process tea leaves and from the warehouse, the teas go to auction for blending or to national buyers for export. These are further sent to distributor/wholesaler wholesalers, retailers smaller retailer and then consumers.

The second supply chain of Assam tea is small tree growers who sell tea leaves to bought leaf factories and co-operative factories. The processed tea from the factories is then sent to national and international buyers. The tea from here either goes to branded teas or to retailers for loose tea and branded teas.

Supply chain Darjeeling tea

Darjeeling tea is also called Champagne tea and is a high grade tea that is an important contributor to Darjeeling’s economy. Darjeeling tea manufacturing follows sustainable farming, which has resulted in organic farming and biodiversity conservation and the hilly tea farms have led to scenic beauty that promotes tourism in Darjeeling. The tea from gardens is sent to factories/warehouses. The factories, too, are major tourist attractions. The tea from the farms goes to auctions or private players and then to exporters.

One major issue with Darjeeling tea plantations is that the tea bushes have aged and replacement needs to be carried out in a scientific manner.

Supply chain Nilgiri tea (Ooty)

The Nilgiri tea goes to factory managers/garden managers, where it’s taken to the factory and then to consumers. India exports a significant portion of its tea production, with the United Kingdom, Russia, and the United States being major importers.

Diagram 1: Vertical Integration of Indian Tea

Indian green tea is exported to Germany, the USA, the UAE, Australia, the United Kingdom and the Netherlands. Indian black tea is exported to Iran, Russia, USA, UAE, Kazakhstan, UK and Germany.

Challenges

By 2013, 90% of the tea manufactured in India was consumed domestically. The growth in the domestic market is correlated to the changing consumer preferences of Indian consumers. As disposable income has risen, consumers have switched from loose leaf teas towards premium, branded categories. The Indian tea industry continues to evolve, with a focus on quality, sustainability, and innovation. Small-scale producers are now focusing on crafting high-quality loose leaf tea, offering a variety of green, white and oolong teas, with direct sourcing of high quality organic loose leaf teas, thus eliminating the complex structure of the tea industry, empowering Indian tea producers and connecting them with global buyers.

Sri Lankan tea industry

Sri Lankan tea contributes to 14 % of the total export earnings of the country. Ceylon tea has a global reputation for its taste and aroma. However, increasing competition from countries like India, Kenya and Indonesia has resulted in low market share and lower prices in international markets. Also, the importer-exporter relationship, value addition and relationship quality between the exporter and importer affect the competitive advantage in the Sri Lankan tea business.

Marketing Sri Lankan tea in developed countries is not managed by exporters due to reasons of conflict, control and power. Value creation, like marketing and packaging, in Sri Lankan tea is dependent on the characteristics of supplier – buyer relationship.

Sri Lankan family owned tea companies successfully export their own brand to developed countries, have direct contact with the buyers and thus have a competitive advantage. Presently, price is the most important factor in exporting Sri Lankan tea. The supply chain inefficiencies are due to short term individual stakeholder interests.

The highest grade for Western and South Asian black tea is ‘orange pekoe’, and the lowest is ‘fannings’ or ‘dust’. Sri Lanka produces tea throughout the year due to its climatic conditions. Sri Lankan tea exports have declined due to currency depreciation due to the politics of the country.

There are two types of tea cultivation. One is the smallholder sector, which is owned by private owners and the second is the estate sector, which is managed by tea cultivators. 41% of Ceylon tea is exported in bulk and blended with others, so new product benefits do not come to the country. Export companies have wide knowledge of overseeing customer preferences, but a gap between manufacturers and exporters has resulted in a lack of knowledge flow in the tea value chain.

Sri Lankan Orthodox tea appeals to the world market for its aroma, texture and flavour. The major reason for the low production of value added tea is a lack of technology.

Opportunities

There are multiple opportunities for tea business expansion in Sri Lanka. The tea tourism concept can be introduced. Many teas are unique to Sri Lanka and are not found anywhere else in the world. Ceylon tea is the cleanest tea in the world and has a good reputation in the world market. Nuwara Eliya, Dimbula, Uva and Uda Pussellawa, Ruhuna and Sambaragamuwa are types of Ceylon teas only found in Sri Lanka. Organic tea, and healthy tea marketing can boost Sri Lanka’s GDP. Thus, we see that women’s empowerment, decreasing time from farmers to exports, and enhancing mobile applications and technology will help Sri Lanka achieve increased profitability and overall sustainability in the tea industry.

Nepal tea industry

Nepal contributes to 0.2% of the global tea. 12-15% Orthodox tea is grown here, Nepal CTC tea is of low quality; and green tea grown here is export quality. Initially, Nepal tea leaves were sent to Darjeeling for processing, but Nepal has made tea a fully commercial industry.

The expensive Orthodox is exported to Europe, Germany, and the USA, and the cheaper CTC is exported to India & Pakistan to meet local demand. Green tea is exported to India, Germany and other developed countries.

One challenge in the supply chain of Nepal tea is that it is sold in small portions. The developed countries need tea of larger quality and in single consignment. These initiations have been taken by tea growers in Nepal to meet the bulky demands. Nepal is planning to increase the exports of green tea, which has higher demand and is also marketed for health benefits.

Issues tea industry will face in the future

Climate change, like change in weather patterns, leads to decreased quality of tea leaves; labour shortages in tea growing regions can impact the cost of tea, sustainability concerns the growing demand for conserving natural resources and reducing climate impact; and transport and logistics challenges.

As tea is a commodity, any natural disasters and trade policies like those in Sri Lanka lead to logistical issues affecting the availability and price increase for consumers. Increased transportation costs, labour costs, and fuel costs lead to an increase in consumer demand. Food and safety regulations can lead to an increase in costs, and non-compliance can lead to penalties and fines. Competition from other beverages is one of the issues the tea industry will face in the coming years.

In order to stay competitive, the tea industry needs innovation, unique blends, and marketing to attract retail customers.

Conclusion

Tea is a cash crop that is presently in high demand in developed countries. The tea drinking choice is shifting from local CTC to luxury flavoured Orthodox and spiced green teas.

As the Indian subcontinent, with countries like Nepal, India, and Sri Lanka having their own advantages, we see that the main changes done in the supply chain are reducing the time from farmers to consumers and this has benefited the entire vertical supply chain. The tea available to the consumer is fresher and valued for its spices and blends. Also, the lead time reduction has helped the manufacturers with cash flow.

The challenges included value addition at the manufacturer level, which can be advanced with information sharing using apps and customer feedback through exports and importers.

References

- Tea Supply Chain – Steeped Content

- https://lebasic.com/wp-content/uploads/2019/10/BASIC_Assam-tea-Value-Chain-Study_October-2019.pdf

- A Schematic Model Showing Supply Chain of Tea in India

- Supply Chain Issues the Tea Industry Will Face

- Product Profile: Tea – Trade Promotion Council of India

- History of Indian Tea

- A study on supply chain management of tea in Nilgiri’s district of Tamil Nadu

- From Global to Local Tea Markets: The Changing Political Economy of Tea Production within India’s Domestic Value Chain – Langford – 2021

- A study on supply chain management of tea in Nilgiri’s district of Tamil Nadu

- The Ceylon Black Tea Value Chain

- Tea Industry in Nepal and its Impact on Poverty

- https://www.teaboard.gov.in/pdf/techno_economics_darjeeling_2001_pdf4407.pdf

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications