This article is written by Yash Bagra, a student of Nirma University, on how to transfer shares in India under Companies Act, 2013.

The shares of a company are movable property and are generally freely transferable. Though there might be certain restrictions on transfer of shares of private companies provided in the articles of the company, such restrictions are generally added to protect the rights of one set of investors or the shareholders. However, shares of a public company are always freely transferable. Under section 56 of the Companies Act, 2013 a company will register a transfer of securities of the company (which includes shares), only when a proper instrument of transfer as per the format laid down in Form No SH. 4 (when such securities are held in the physical form). The form needs to be duly stamped, with adequate value, dated and executed by or on behalf of the transferor and the transferee.

The form needs to be sent to the company by the transferor or the transferee within a period of sixty days from the date of execution, along with the share certificate/certificate relating to the securities. In case there is no such certificate, the application must be sent along with the letter of allotment of securities.

A company will not register a transfer of partly paid shares, unless the company has given a notice in Form SH-5 to the buyer and has obtained no objection from the buyer within two weeks from the date of receipt of notice.

What is the time limit for issuing certificate on transfer of shares?

A company should deliver all the certificates of transferred securities within a period of one month from the date of receipt by the company of the instrument of transfer, unless the company is prevented from such delivery due to an order of the Court or instruction by other authority,

What is the applicable stamp duty on transfer of shares?

Companies Act, 2013 requires that where share transfer form is delivered to the Board it should be duly stamped, with adequate value, and dated and cancelled as per section 12 of the Indian Stamp Act. The seller of the shares is responsible for the payment of the stamp duty. The seller must pay stamp duty at the rate of Rs 0.25 for every Rs 100 of share. Special adhesive stamps bearing the word “share transfer” shall be used for stamping for share transfers.

Under 8A of the Indian Stamp Act, securities issued in electronic form need not be stamped provided the issuer pays stamp duty on the total amount of securities issued. Also the transfer of registered ownership of share from a person to a depository or from a depository to a beneficial owner shall not be liable to any stamp duty.

How to determination of valuation of shares for purpose of affixing stamps on the transfer deed happens?

In case of listed companies, it is very easy to find out the price of the shares from the stock exchanges. However, in case of private companies, the value of the shares are difficult to obtain, in such cases the value of the shares for the purpose of determining the stamp duty, will be taken on the basis of the average market value of the shares at the time of transfer or the agreed price between the seller and the buyer, whichever is higher. However, generally the Articles of a private company might contain provisions which provide that the shares must be sold at a fair price determined by the directors or the company’s auditors.

Steps involved in transfer of shares in a private company

Generally, transfer of shares in a private company is governed by the articles of association of the company. Generally, a private company follows the following steps:

- i) The seller should give a written notice to the company about his intention to transfer his share.

(ii) The company would in turn notify other members of the company, stating that certain shares are available which can be purchased by the members. It would generally state the price of such shares along with the time limit within which the members should notify their interest of purchasing such shares. However, if none of the members agrees to purchase the shares, the shares can be transferred to an outsider, to which the company cannot refuse.

iii) Once there is a prospective buyer, one need to fill up the share transfer deed in Form No- SH.4

- iv) The transfer deed needs to be duly executed both by the transferor, which should be duly stamped, with adequate value, dated and cancelled.

(v) Attach the relevant share certificate or allotment letter with the transfer deed and send the same to the company within sixty days from the date of execution.

- vi) Execute Shareholders Agreement and Share Transfer Agreement to regulate the relationship between the shareholders.

Transfer procedure under the depositories system

Under Section 56(4) of the Companies Act, 2013, when a company is transferring the securities through a depository, the company should immediately inform the details of allotment of securities to the depository. If any depository or depository participant has fraudulently transferred the shares, it shall be liable under section 447.

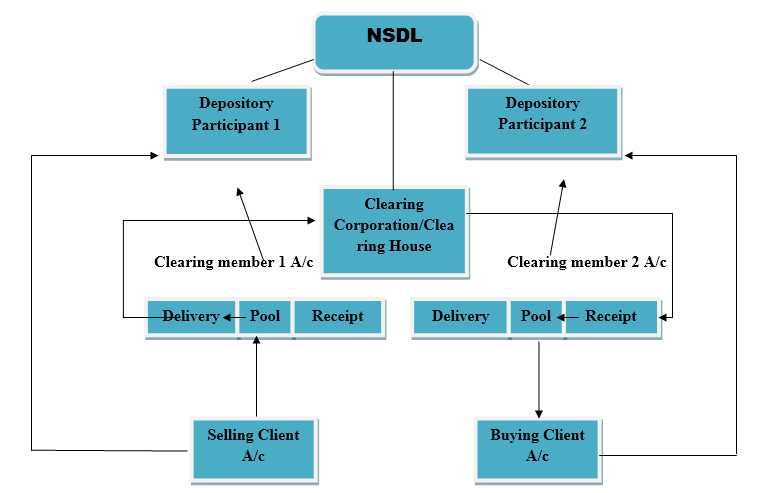

Diagram below explains the depository system in case of transfer of shares. This procedure will apply when the investor or transferor has informed the company about his intention to transfer and is doing under the depository system.

Step 1: Firstly, seller has to give delivery instruction to Depository Participant 1 (DP1) to debit his account and transfer the concerned securities to Clearing Member1 Pool A/c with DP1. Clearing Member1 than gives parallel receipt instruction to DP1 to accept in his clearing account securities transferred by seller through DP1, if he has not already given standing receipt instruction for all credits into his clearing account. Securities are in turn transferred from selling client A/c to clearing member pool A/c with DP1.

- Step 2: Now, Clearing Member1 gives delivery to Clearing Corporation (CC) instruction to DP1 to debit his Clearing Member1 Pool A/c and credit his Clearing Member1 Delivery A/c. The transfer takes place on the execution date which is mentioned in the instruction. Delivery which is supposed to be given to CC instruction will be as per final/ net delivery obligation.

- Step 3: Till settlement day securities which are to be transferred lay in the clearing member1 Delivery A/c. Securities lying in clearing member1 delivery A/c are automatically transferred to the Clearing Corporation/ Clearing House at the time of pay in. There is no requirement of debit instruction for this transfer. There is no set deadline time for pay-in of securities to the Clearing Corporation/ Clearing House as it varies from one exchange to another.

- Step 4: Now, automatic transfer of securities from Clearing Corporation/ Clearing house to clearing member 2 pool A/c with Depository Participant 2 (DP 2) at the time of pay out takes place and no instruction is required because of the automatic transfer.

- Step 5: Securities are transferred from clearing member2 receipt A/c to clearing member 2 pools A/c. Receipt account of clearing members is nothing more than a transit account used for maintaining audit trail.

- Step 6: Clearing Member 2 gives a delivery instruction to DP 2 to debit his Clearing Member 2 Pool A/c and credit Buying Client A/c with DP 2. Buyer gives parallel receipt instruction to DP 2 to accept in his account securities transferred from Clearing Member 2 Pool A/c through DP 2 unless he has not given a standing instruction to receive credits to his account.

Note: – National Securities Depository Limited (NSDL) does not handle these funds. Buyer gives cheque to Clearing Member 2 and subsequently he gives it to the Clearing Corporation/ Clearing House. After the cheque is cleared by clearing bank, the Clearing Corporation/ Clearing House allow credit of securities to clearing member 2 and thereafter, communicate the same to NSDL.

- Step 7: Lastly, securities are transferred to Buying Client A/c from Clearing Member 2 Pool A/c with DP 2. The securities will remain in clearing member pool A/c until delivery instruction is given by him.

NOTE: For further clarifications NSDL bye laws (9.6) and business rules 12.2 can be taken as a basis of information.

When does transfer of shares complete?

A transfer is complete when all the formalities such as execution of the transfer deed and handing over the share certificates are complete.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

https://t.me/joinchat/J_

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

In telangana how much is share transfer fee/stamp duty ? .25 or .50?

Whether we have to sign share transfer deed and follw the whole procedure In case of order by court for transfer of share. Please Reply

sir, can you provide a format of the notice to be sent by the transferor to the company for the transfer of shares?

Please share the procedure of online payment of stamp duty on transfer of shares for Rajasthan State.