This article has been written by Samridhi Jain, pursuing the Certificate Course in Introduction to Legal Writing from LawSikho.

Table of Contents

Introduction

The word “smart contract’ emerged in 1994 by an American cryptographer and a computer scientist, Nick Szabo. The widespread use and understanding of practical applications happened only in 2008.

“A smart contract is a computer protocol (set of rules) that digitally facilitates, verifies, and enforces the negotiations between two parties. It uses a distributed ledger system (blockchain) to store data on public databases and perform transactions without involving third parties.”

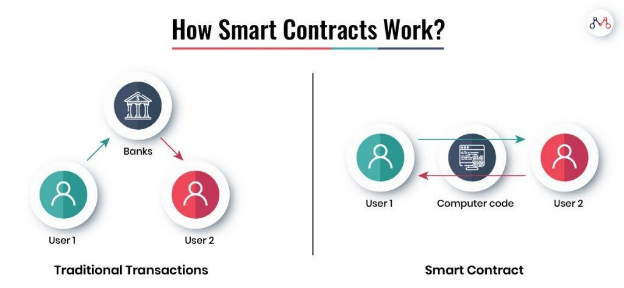

How do Smart Contracts work?

The smart contract is a blockchain-based computer input code. The contract terms are already put in the code itself. Smart contracts analyse and verify every transaction against the terms and automatically executes them.

Smart Contract Real Estate Use: Propy

For example, Propy is a smart contract-based cross-continental marketplace for buying and selling properties. It allows owners and brokers to list their properties and allows sellers to search and negotiate irrespective of their locations. The closing of the deal happens when the online transaction occurs and each block is recorded in the blockchain.

Traditional Contracts v. Smart Contracts

To understand Smart Contracts it’s crucial to know the difference between smart contracts and traditional contracts. Let’s understand it by using a table.

|

Traditional Contracts |

Smart Contracts |

|

Focuses on performance of legal terms agreed by the parties. |

An automatic computer Program. |

|

Can be modified when both parties agree for an amendment. |

Cannot be modified as the code is already inputted in the block, must create a new one. |

|

Have a great possibility of manipulation and bias.

|

Smart contracts cannot be hacked or manipulated in the interests of any of the parties.

|

|

Clearly involves human intervention like negotiation, drafting, etc. |

Very restricted human intervention. |

|

These are simple in terms of the Terms of the contract. |

These can get complex as it uses a ledger-based technology. |

Advantages of Smart Contracts

Safe

Safety is an integral part of Smart Contracts which is possible through encryption and the distributive ledger systems that ensures complete data security or protection. Each block or piece has information that is unhackable due to the interconnectedness of all the blocks.

Speedy Process

It’s one of the fastest mechanisms to get the task done smoothly and swiftly with great accuracy. Since these are focused on reducing human intervention the accuracy points increase as time spent in processing and administrative work becomes negligible. Algorithms have the ability to totally eradicate these errors.

Reliable

The contract is based on an already inputted program which is determined by algorithms. It can automatically process the data at every step involved in the process. A series of networks interconnectedly work together to bring about the output which reduces the possibility of bias or manipulation or one-sided deals that could be harmful. One-sided deals often lead to lots of disputes if parties have negligently negotiated.

Cost-Efficient

All types of fees, administrative formalities, procedural costs or any sort of paper wastage is cut. Not to forget the costs of human error as well. Any kind of ancillary or third party costs can also be eliminated because everything is governed by a program.

Smart Contracts: The Indian Perspective

The world is changing and developing at a faster rate than ever. Blockchain is taking over the internet and being discussed in almost every conversation. Considering the Budget 2021 news, smart contracts would not be a very viable option in India, but this can only be decided once the Budget is out.

Nevertheless, it’s important to understand how Smart Contracts is not equal to Blockchain technology but just a part of it. Blockchain technology is used across operations and should not be misunderstood.

It’s extremely crucial for India, a growing economy to leverage this amazing opportunity to create a system that further enables better R&D in this space to understand and implement the strategies involved to ultimately benefit from it.

Though there have been creating departments and authorities who have started programs in the direction we still need better private participation to scale this to the next level.

|

Department/Board/Authority |

Program |

|

Ministry of Electronics and Information Technology |

National Policy on Software Products (2019) |

|

Telecom Regulatory Authority of India |

In exercise of powers conferred by section 36 and section 11of the Telecom Regulatory Authority of India Act 1997 |

|

Press Information Bureau Government of India: Ministry of Commerce and Industry |

Integrate to Innovate Programme for energy Startups |

|

Department of Banking Regulation Banking Policy Division |

Enabling Framework for Regulatory Sandbox |

|

Press Information Bureau Government of India: Ministry of Commerce and Industry |

Coffee Board Activates Blockchain-Based Marketplace in India |

Section 10 of the Indian Contract Act, 1872 says – “All agreements are contracts if they are made by the free consent of parties competent to contract, for a lawful consideration and with a lawful object, and are not hereby expressly declared to be void.”

If two parties sign a contract with or without third party involvement it will be considered legal. By definition, we could say that the Indian Contract Act 1872 allows Smart Contracts.

Sections 5 and 10 of the Indian Information Technology Act, 2000 legally recognize digital signatures and consider e-contracts as valid and enforceable under the law.

Smart Contracts use cryptography for coding into the ledger-based system. These could also use digital signatures for authentication purposes. But the problem is digital signatures created as a part of blockchain technology, are auto-created and are not authorized under the IT Act, 2000. This amounts to being invalid.

Conclusion

In sum, Smart Contracts and its technology will continue to evolve irrespective of us as a country implementing it or not. The legal issues involved will continue to rise and simultaneously have innovative solutions. These contracts involve questions that are beyond the contract law we’re taught in law schools.

This deals with algorithms and data processing which isn’t really present in law books. The power of disruption that such contracts will bring is tremendous and the growth can be a driving factor if India takes the opportunity and does not refuse to change with the changing world.

Risks are always necessary for growth. Change is inevitable and is the only constant. Smart Contracts will change the legal arena with its accompanying challenges, but that is what legal systems are- ever-evolving with the times.

References

- https://www.perkinscoie.com/images/content/1/9/v5/199672/2018-More-Legal-Aspects-of-Smart-Contract-Applications-White-Pa.pdf

- https://www.mondaq.com/india/fin-tech/889458/blockchain-and-smart-contracts-indian-legal-status

- https://www.mantralabsglobal.com/blog/smart-contracts-in-india/

- https://law.asia/smart-contracts-blockchain-technology/

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications