")

In this blog post, Anand Sancheti, a student pursuing a Diploma in Entrepreneurship Administration and Business Laws by NUJS, describes the accounting system to be followed by Partnership Firms and LLPs.

Applicability of the Act

Limited Liability Partnership is prevailed by ‘The Limited Liability Partnership Act, 2008’ and various Rules made there under. It is a separate legal entity under the Limited Liability Partnership Act 2008.In LLPs purchases movable / immovable property has to do in the name of LLP. Liability of a partner is limited to the extent of his capital contributed or agreed to be contributed as per LLP agreement.

Partnership prevails by the Indian Partnership Act 1932 and various rules made there under. It is not a separate entity. Partnership firm cannot purchase property in its name only purchase is permitted in the name of partners. Liability of partners is unlimited.

Books of Accounts to be maintained

- Partnership Firms and LLPs are required to maintain books of accounts as per Tax laws. Both can maintain books of accounts on Cash or Mercantile basis.

- Fundamental Accounting Assumptions -1) Going Concern, 2) consistency, 3)Accrual has to follow.

- LLPs have to keep books on the basis of double entry system of Accounting at its registered office. The LLPs has to maintain proper books of accounts as follows prescribed (Rule 24 (1)) relating to its affairs for each year of its existence.

- Statement of Receipt & Expenditure.

- A record of the assets and liabilities of the limited Liability Partnership.

- Statement of recognized gains & Losses.

- Statement of cost of goods purchased, inventories, work –in-progress, finished goods and cost of goods sold; and

- Any other particulars, which the partners may decide.

- Both LLPs & Partnership Firms have to follow the complete accounting cycle from Journals, Ledgers, Cash Book, Bank book, Trial balance, Profit & Loss account and finally, a Balance Sheet which gives the financial position of the business at the end of the period. Few more records need to maintained are specifically mentioned below:

- Partners Capital Account: Fluctuating Capital Method and Fixed Capital Method (Partners Capital Account & Partners Current Account)

- Profit & Loss Appropriation Account: The net profit as shown by the profit and loss account of partnership firm needs certain adjustments with regard to interest on capitals, interest on drawings, salary, commission to the partners, if provided, under the agreement. For this purpose, ‘Profit and Loss Appropriation Account’ maybe prepared.

- Calculation of Interest on Capital: Interest @12 % pa is deductible as per Income Tax Act.

- Calculation of Interest on Drawings

- Past Adjustments: Past Adjustments relate to the interest on capital, interest on drawings, salary to partners, etc that have been omitted by mistake or have been wrongly treated. In such a situation, necessary adjustments have to be made in the partners’ capital account through an account called Profit and Loss Adjustment Account.

- Goodwill (Intangible Assets) Valuations: Following methods can be used for Goodwill Valuation:

- Average Profits Method:

- Weighted Average Profit method

- Super profit Method,

- Capitalization Method,

- Present value of Super Profits

- Average Profits Method:

- Partners Capital Account: Fluctuating Capital Method and Fixed Capital Method (Partners Capital Account & Partners Current Account)

Applicability of Accounting Standards

Council of ICAI has classified the non-Corporate assesses in three different level(level I, Level II, or Level III).Applicability of AS 1 to As 32 depends on the fact that, In which level LLP or Partnership Firm has been categorized.

Deductions as Expenses as per Income Tax Act

LLPs and Partnership Firms can claim the following amounts as deduction:

- Interest paid to partners, provided such interest is authorized by the LLP or Partnership Agreement Interest @12 % pa is deductible as per Income Tax Act.

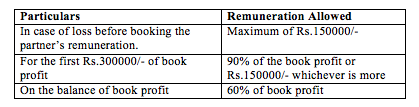

- Any salary, bonus, commission, or remuneration (by whatever name called) to a partner will be allowed as a deduction if it is paid to a working partner who is an individual.

- The remuneration paid to such working partner must be authorized by the LLP Agreement and the amount of remuneration must not exceed the given limits as per income Tax Act.

Accounting Implication of Change in Profit sharing ratio

Accounting Implication of Change in Profit sharing ratio

When the partners decide to change their profit-sharing ratio, some partners will gain while others will lose. Hence, the gaining partner has to compensate the partner who makes the sacrifice by paying (or through necessary adjustment in their respective capital accounts) the proportionate amount of goodwill.

Accounting for Inventories for Partnership Firm & LLPs

As per As 2 – Inventories should be valued at the lower of cost and Net Realizable Value.

- Techniques for the measurement of the cost of inventories:

- Standard cost method

- Retail method

- Calculation of the cost of Goods

- FIFO (First in First out) Method

- LIFO (Last in First Out) Method

- Weighted Average Method

Depreciation

Different accounting policies for depreciation are adopted by different Enterprises. Depreciation is charged in each accounting period by reference to the extent of the depreciable amount, irrespective of an increase in the market value of the assets. Methods for calculation of depreciation:

- Straight Line (Time) method.

- Straight Line (use) method.

- Accelerated Depreciation:

- Sum of digit method

- Declining balance method.

Annual Statement of Accounts and Solvency

Annual Statement of Accounts and Solvency (Form No 8) needs to be filed by every LLP with the Registrar of Companies every year within 30 days from the end of financial years.

Annual Compliances

- The LLP is required to file an Annual Return (Form 11) duly authenticated with the Registrar within 60 days of the closure of its financial year in such manner & shall be accompanied by prescribed fee.

- Partnership firm will have to file income tax return irrespective its income. There is no requirement of filing Annual Accounts and Annual returns with the Registrar for Partnership Firm.

Preservations of Accounting Records

Limited Liability Partnership Firms has to preserve the accounting records for 8 years from the date on which they are made.

Electronic Filing of Documents and Returns

- Every form or application or document or declaration required to be filed by the Limited Liability Partnerships in computer readable electronic form, in PDF to the Registrar trough the portal maintained by the Ministry Of Corporate Affairs on its website mca.gov.in

- No such requirement is there for Partnership Firm.

Income Tax Aspect

For the purpose of Income Tax Act, a limited Liability Partnership Firm is treated like Partnership Firm. All the provisions of Income Tax for a Partnership Firm is applicable as it is to Limited Liability Partnership.

- TDS: No TDS is required to be deducted by firm from payment of interest (TDS exemption under Section 194A (3)(iv) of the Income Tax Act) and remuneration to partners (As Employer-Employee relationship does not exist)

- MAT & DDT

- Since the LLP is treated as same as Partnership firm in the matter of taxation, the provisions of MAT and Dividend Distribution Tax will not be applicable for LLP and Partnership firm.

- Profit of LLP and Partnership Firms credited to the partners’ account shall be an exemption to tax under Section 10(2A) to avoid double taxation. However, remuneration and interest paid to its partners shall be liable to tax under Section 40(b) of the Income Tax Act.

- AMT is applicable to LLPs & Partnership Firms Alternate Minimum Tax means the amount of tax @ 18.5 % + 3% Education Cess on the adjusted total income of the Non-Corporate Assesses. The provision of AMT is given under Section 115JC under Chapter XII-BA of the Income Tax Act.

- The word Adjusted Total Income has been defined under Section 115JC (2) of the Income Tax Act as the total income of the assesse on which he is liable to pay income tax, is increased by-

- Deduction claimed under Sections 80H to 80RRB, except Section 80P.

- Deduction claimed under Section 10AA.

- Tax Credit of AMT is of an assessment year is allowed U/S 115 JD.

Presumptive Taxation under section 44AD of Income Tax: Section 44 AD is applicable to Individuals, firms and HUFs but not applicable to LLPs. Thus LLPs will not be able to avail presumptive taxation schemes under section 44AD.

Presumptive Taxation under section 44AD of Income Tax: Section 44 AD is applicable to Individuals, firms and HUFs but not applicable to LLPs. Thus LLPs will not be able to avail presumptive taxation schemes under section 44AD.

Service Tax

For the purpose of Service Tax, a LLP is treated as Partnership Firm. But Partial reverse charge is not applicable to LLPs, as it does not cover under the definition of “Body Corporate” in Service Tax Act although it has a legal status of a body corporate.

Sales Tax /VAT

Under Sales Tax, LLP is treated as body Corporate and the definition of “Dealer” under the Central Sales tax Act 1956 includes Body Corporate also.

Audit

Every LLP whose Annual turnover exceeds INR 40 lac or total contribution of partner exceeds INR 25 lac, has to mandatorily get the Accounts audited as per the rule 24(8) defined under LLP Rules, 2009. In other cases, where the LLP does not meet the above criteria, the audit of accounts is not compulsory.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

https://t.me/joinchat/J_

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

is LLP required to comply with ICFR?