")

In this blog post, Ananda Boga, a student pursuing a Diploma in Entrepreneurship Administration and Business Laws by NUJS, analyses the possibilities of ratification of a related party transaction made without the approval of the Board.

An RPT is a related party transaction between companies and their related subsidiaries, associates, joint ventures, directors and their relatives, substantial shareholders, executives or entities owned or managed by its directors, executives or their families. It is a transfer of resources, services or obligations between a Company and its related party, regardless of whether or not a price is levied.

What is Related Party?

These related party transactions are rampant and play a role in many businesses. The Company Act 2013 defines the term “related party” as:

- A director or his relative

- KMP or his relative

- A firm, in which a director, manager or his relative is a partner

- A private company in which a director or manager is a member or director

- A public company in which a director or manager is a director and holds along with his relatives, more than 2% of its paid-up share capital

- A body corporate whose board, managing director or manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager, except if advice/ directions/ instructions are given in the professional capacity

- Any person on whose advice, directions or instructions a director or manager is accustomed to act, except if advice/ directions/ instructions are given in the professional capacity

- Any company which is:

- A holding, subsidiary or an associate company of such company, or

- A subsidiary of a holding company to which it is also a subsidiary

- Such other persons as may be prescribed.

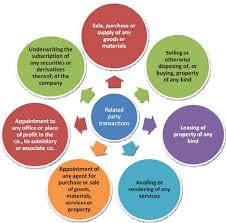

Forms of Related Party Transaction

Related party transactions can be in many forms. Under Section 188 of the Company Act 2013, the sale, purchase or supply of any goods or materials, selling or otherwise disposing of, or buying property of any kind as well as leasing property of any kind can be considered as a related party transaction. Furthermore, availing or rendering of any services, appointing an agent for the purchase of sale of goods, materials, services or property, appointment to any office or place of profit in the company, its subsidiary or associate company is also considered to be an RPT.Here, under the Company Act 2013, ‘office or place of profit’ means any office or place –

(i) Where such office or place is held by a director, if the director holding it receives from the company anything by way of remuneration over and above the remuneration to which he is entitled as director, by way of salary, fee, commission, perquisites, any rent-free accommodation, or otherwise;

(ii) Where such office or place is held by an individual other than a director or by any firm, private company or other body corporate, if the individual, firm, private company or body corporate holding it receives from the company anything by way of remuneration, salary, fee, commission, perquisites, any rent-free accommodation, or otherwise;

Lastly, an RPT could also extend to underwriting the subscription of any securities or derivatives thereof, of the enterprise.

Approval of RPTs

It has frequently been observed that in several cases companies that have higher RPTs linked to sales and income have reported relatively poorer performances in comparison to those having lower RPTs. Moreover, RPTs have come under the microscope as many firms have misused them, which inadvertently led them to massive corporate scandals. Due to this, some approvals are required to permit a related party transaction.

As per the Company Act, 2013, an audit committee must approve where transaction value is within the prescribed limit. The Board of Directors too must approve this by an ordinary resolution. Where transaction value exceeds the prescribed limits, an ordinary resolution must be passed by the audit committee and the board or directors. However, in this case, shareholders too must pass a special resolution as opposed to the ordinary resolution.

Related party transactions that shareholders must approve of include sale, purchase or supply of any goods or materials, directly or through the appointment of an agent having limits on transactions greater than 10% of the annual turnover or 100 crores, whichever is lower. Selling or otherwise disposing of or buying property of any kind directly or through the appointment of an agent must be limited to 10% of the net worth or 100 crores, whichever is less. Transactions relating to the leasing of the property of any kind must be limited to 10% of the net worth or turnover or 100 crores, whichever is less. The availing or rendering of any services, directly or through the appointment of an agent is also limited to 10% of the net worth, or 50 crores in this case, whichever is less. The appointment to any office or place of profit in the company, its subsidiary company or associate company is limited to two and a half lakhs per month, while remuneration for underwriting the subscription of any securities or derivatives thereof of the company has a limit of 1% of the net worth. As mentioned, all these related party transactions must also be approved by the shareholders, along with the board of directors and audit committees.

When a director or another employee enters into any contract or arrangement without the prior permission and approval of the Board or approval through a special resolution in the general meeting, and if it is not ratified at that meeting, regardless of what the case may be, the contract shall be deemed voidable at the option of the Board of Directors after three months from the date on which the related contract was signed or arrangement agreed upon.

Under the Company Act, 2013, there is an exemption provided that states, “There is an exemption provided under the Companies Act, 2013, wherein the approval of board or shareholders are not required if the Company has related party transactions as per the prevailing market price and on arm’s length basis irrespective of transaction value” This is provided that the Company need to justify and should have the required evidence proving that the transactions were made on arm’s length basis.

There is no exemption from the approval process based on the ‘arm’s length’ criterion, but it is important to understand that a transaction entered into by a firm on an arm’s length basis has a strong likelihood of helping the approval process and setting an example for commendable corporate governance.

It is also important to know that under implications of the revised clause 49 of Listing Agreement, any related party transactions regardless of the value of transaction demands approval of audit committee before hand. Also, Under the Company Act 2013, “Ratification of RPT can be done in Board Meeting or General Meeting by passing a Special Resolution is available under the Proviso of CA, 2013 and which shall be done on or after three months from the date of entering into Related Party Transaction.”Under the Revised Listing Agreement, ratification of related party transaction is not available.Furthermore, it is mandatory to enter an agreement with the related party, and just a letter of engagement will not suffice. In the case of entering related party transactions with foreign parties and foreign body corporates, no compliance is required, as mentioned under the Company Act, 2013 and The Listing Agreement.

The Board of Directors plays a crucial role in ratifying any related party transaction. A company must seek certain approvals from their board before going ahead with any such transaction. Regardless of its capital or transactional value, every company must attain the approval of the Board. The approval must be requested at a planned Board meeting and must be obtained without passing of a circulated resolution. Any interested Director is not allowed to be present at the meeting when discussions regarding his interest are going on.

Along with the approval of the Board of Directors, approvals through a special resolution by the firm’s members must be attained beforehand when entering into a related party transaction. A member of the company who is also a related party cannot have the privilege of voting on such special resolution to approve any contract or arrangement that the company may enter into. When it comes to a wholly owned subsidiary, the holding company will pass the special resolution. That alone will be sufficient for the objective of entering into a related party transaction between a holding company and a wholly owned subsidiary.

[divider]

References:

- http://taxguru.in/company-law/related-party-transactions-companies-act-2013.html#sthash.veCuahkC.dpuf

- http://taxguru.in/company-law/keeping-track-india-spends-money.html – sthash.c3LxN330.dpuf

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications