This article is written by Saloni Mathur, Corporate Finance Consultant at S. R. Ashok and Associates Private Limited, pursuing Diploma in M&A, Institutional Finance and Investment laws (PE and VC transactions) offered by Lawsikho.

Introduction

In the words of the famous James McNerney,

” The key to making acquisitions is being ready because you really never know when the right big one is going to come along.”

2018 was a big year for mergers and acquisitions in India and proved to be quite a robust one for the Indian Corporates. Triggered by the Insolvency and the Bankruptcy Code (hereinafter referred to as “IBC”) that came into effect from June 2016 majority resolution plans for the insolvent companies adopted revival through mergers or foreign acquisitions. Foreign Direct investment in India increased by 3675 USD Million in January of 2019 and averaged 1341.88 USD Million from 1995 until 2019, reaching an all-time high of 8579 USD Million in August 2017. A foreign Company has been defined in Section 2(42) of the Companies Act, 2013 which means any company or body corporate incorporated outside India, and which conducts any business activity in India. When this foreign company acquires any stake or substantial stake in the Indian Company, registered and Incorporated in India, it refers to foreign acquisition or Foreign Direct Investment.

Foreign acquisitions of the Indian Companies come with a lot of benefits and expertise. New technology, know-how transfer, increased capital investment and financial resources for expansion are some of the key reasons why an Indian Company goes for foreign investment. Foreign companies get a couple of tax benefits while investing in Indian Companies and in turn acquire a significant control over the decision making of the Indian Companies

There is a plethora of laws that govern acquisition of an Indian Company by a Foreign Company comprising of the Master Directions of the Reserve Bank of India on Foreign Direct Investment in India,[1] Foreign Exchange management (Transfer or Issue of Security by a person Resident Outside India) Regulations, 2017[2], Securities and Exchange Board of India (Substantial Acquisitions and takeover Regulations), 2011 [3], Consolidated FDI Policy issued by the Department of Public Policy, and the International Taxation Laws. This article shall take you through the legal regime governing acquisition of an Indian Company by a foreign company broadly covering the modes of acquisition, entry routes, and RBI and SEBI guidelines dealing with substantial acquisition.

Defining Foreign Acquisition in Indian Company

Investment

The term investment has been defined in clause 2.12 of the Master Direction on Foreign Direct Investment in India which means to subscribe, acquire, hold or transfer any security or unit issued by a person resident in India.

Direct Foreign Acquisition

Since Investment includes ‘to acquire’, Foreign Direct Investment is the investment by a foreign company through capital instruments by a person resident outside India in an unlisted Indian Company or in ten percent or more of the post issue paid up equity capital on a fully diluted basis of a Listed Indian Company. When there is a direct target on the Indian Company, it refers to direct acquisition.

Indirect Foreign Acquisition

When the investment made by an Indian Entity which has received foreign direct investment makes investment in the capital instruments of another Indian Entity it refers to an indirect acquisition or downstream investment as defined in clause 9.1.15 of the Master Direction of RBI on Foreign Direct Investment in India. Thus if a foreign company invests in Indian Company and that Indian Company further invests in another Indian Entity, the investment gets down-streamed and shall be called an indirect foreign investment.

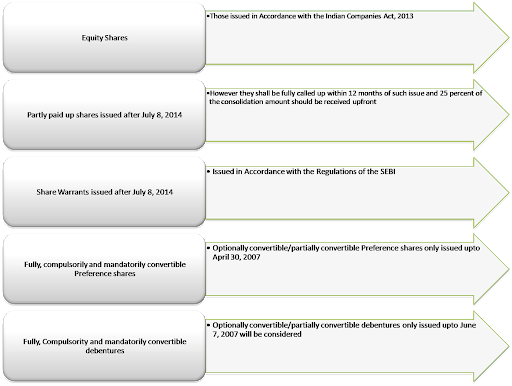

Capital Instruments through which foreign Companies can make Investment

Figure 1.1

Indian Capital Instruments for foreign acquisitions

Entry Routes for Foreign Acquisitions and Sectoral Caps

There are primarily two entry routes for Foreign Companies for making investment in Indian Companies:

- Automatic Route

- Approval Route

Automatic Route

It is that entry route that does not require prior approval of the Reserve Bank of India.

Government Route

Government route requires prior approval of Secretariat for Industrial Assistance, Department of Industrial Policy and Promotion, Government of India.

What is the Cap on Acquisition by Foreign Companies?

Sector cap is the limit indicated against each sector or activity where the amount of foreign acquisition can be made. Following is an illustration depicting various sectors under the Automatic and the Approval Route.

Automatic Route in selected sector/activities

| Serial No. | Sector/Activity | Cap |

| 01. | Agriculture | 100% |

| 02. | Plantation Sector | 100% |

| 03. | Manufacturing | 100% |

| 04. | Air-Transport Service | 100% |

| 05. | Construction Development | 100% |

| 06. | Credit Information Companies | 100% |

| 07. | NBFCs Registered with RBI | 100% |

| 08. | Insurance | 100% |

| 09. | Pension | 100% |

| 10. | Asset Reconstruction Companies | 100% |

Approval Route in selected sectors/activities

| Serial No. | Sector/Activity | Cap | Government Approval |

| 01. | Defence | 100% | Beyond 49% |

| 02. | Print Media-Publishing of Newspapers and periodicals | 26% | Up to 26% |

| 03. | Investment by foreign Airlines | 49% | Up to 49% |

| 04. | Satellites- Establishment and Operation | 100% | Up to 100% |

| 05. | Telecom Services | 100% | Beyond 49% |

| 06. | Banking-Private Sector | 74% | Beyond 49% |

| 07. | Banking-Public Sector | 20% | Up to 20% |

| 08. | Broadcasting content service( FM Radio) | 49% | Up to 49% |

| 09. | Pharmacy- Brownfield | 100% | Beyond 74% |

| 10. | Private Security Agencies | 74% | Beyond 49% |

Table 1.1

Source: Consolidated FDI Policy, 2017

Are there any Prohibitions from Foreign Acquisitions?

Lottery, Gambling, chit funds, Nidhi Companies, Transferable Development Rights, and real estate business or construction of farm houses prohibit any kind of foreign acquisition. Investment from Pakistan and Bangladesh in sectors like defence, Space and Atomic Energy is strictly prohibited. Investment by these companies can be received in sectors other than defined above, however they are subject to prior government approval.

What are the modes through which a foreign Company go for Indian Acquisition?

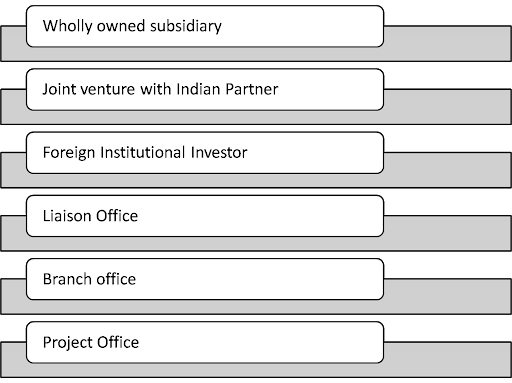

There are broadly five modes through which a foreign company can acquire control over the Indian Company:

Figure 1.2

Modes of Acquisition by a foreign Company

Steps Involved in Investment or Acquisition

For incorporating a wholly owned subsidiary the entry procedure generally involves incorporating a company, setting-up of business, and undertaking business compliances. A company can be a public company or a private company and necessary provisions governing incorporation of the Company are there in the Indian Companies Act, 2013. The foreign company then requires establishing a set up through a Branch Office, Liaison Office, and a project office. Project office generally requires Registration with the Registrar of Companies and prior approval of the RBI. Once there has been a business set-up certain compliances in the form of PAN, TAN, GST Registration Number, and Import Export Code have to be taken.

Following are some steps that require an investment or foreign acquisition to be complete:

- Identifying the appropriate structure to invest through

- Take Central Government Approval (if required)

- Inflow of funds via eligible capital instruments as discussed above

- Complying with the reporting requirements of the Reserve Bank of India.

- Finding the ideal project space for the business transactions

- Hiring of manpower

- Obtaining licenses, if any

Other Aspects to be covered in Foreign Acquisition

Repatriation of Investment Capital and Profits earned

All foreign investments are freely repatriable, subject to the sectoral policies. The dividends can also be freely repatriated, only through the authorized dealer bank. Further the Foreign companies can sell shares on the stock exchange without prior approval of the RBI and repatriate the sale proceeds through the bank, if they hold the shares on the repatriation basis.

Pricing Guidelines and Consideration Treatment

A foreign company can open an escrow account in accordance with the Foreign Exchange Management Act (Deposit) Regulations, 2000. Such can be funded by an inward remittance through the Authorized dealer bank subject to the conditions of FEMA.

The price of the Securities to be issued to the foreign investor shall be worked out as follows:

- A) Listed Company: The price shall not be less than the price worked out in accordance with the SEBI Guidelines in case of a listed Indian Company or of a company going through delisting.

- B) Unlisted Indian Company: The price shall not be less than the valuation of the capital instruments done as per internationally accepted pricing methodology for valuation on an arm’s length basis duly certified by a chartered accountant or a SEBI Registered Merchant banker or a practicing cost accountant.

The above guidelines shall not be applicable if the investment is made on a non-repatriable basis.

Subscription to Memorandum of Association

If the shares are issued to a foreign company outside India as subscription to Memorandum of Association such investments shall be made at face value subject to entry route and sector caps.

Purchase of Capital Instruments of the Indian Company by a person resident outside India

Any foreign company can purchase shares in an Indian Company listed on a stock exchange:

- The foreign company has already acquired control of such company in accordance with the SEBI (Substantial Acquisition and Takeover) Regulations, 2011.

- The amount of consideration is paid as per the mode of payment or out of the dividend payable by the Indian Investee Company in which such foreign company has acquired or has control in terms of the SEBI regulations governing takeover.

Disinvestment from the Indian Company

The sale proceeds of the Capital instruments can be remitted outside India or credited to NRE/FCNR account of the foreign company.

Reporting Requirements – Single Master Form

- Indian Entities that have received FDI shall register themselves with Entity master.

- Entity master is the one stop portal for foreign investment reporting which has been introduced with the objective of obtaining data on foreign investment in an Indian Entity.

- Indian Entities who do not comply with the above registration will not be able to receive FDI under FEMA regulations and shall be marked as non-compliant. Existing companies had to register by July, 2018 on FIRMS Portal.

- The form has subsumed 9 forms of erstwhile reporting in following forms:

- FC-GPR- Old ARF and FCGPR filed for allotment of Capital Instruments.

- FC-TRS- Reporting transfer of Capital Instruments between persons of Indian Origin and Persons Resident outside India.

- Form LLP-I- FDI in LLP through capital contribution

- Form LLP-II- Disinvestment or transfer of capital contribution in LLP

- Form CN- Issue or transfer of convertible notes

- Form DRR- Transfer of Depository Receipts

- Form DI- Reporting of downstream investment

- Form InVi- Reporting of investment by a person resident outside India in an investment vehicle.

How are Indian Acquisitions by Foreign Companies governed by SEBI (Substantial Acquisition and Takeover) Regulations, 2011?

- Indian Companies listed on a stock exchange which are proposed to be acquired by a foreign company are required to comply with the SEBI (Substantial Acquisition and Takeover) Regulations, 2011.

- The SEBI SAST Regulations, 2011 came into force on October 22, 2011. When the acquirer takes over the control of the target company it is termed as a ‘takeover’. When there is a substantial acquisition of shares and voting rights, it refers to the substantial acquisition of shares.

- If the acquirer (along with the persons acting in concert) holding less than 25 percent shares and voting rights in the target company, agrees to acquire the target company (Indian Company) which would entitle it, along with the persons acting in concert to exercise 25% or more voting rights in the target company, it will need to make an open offer to the shareholders of the target company.

- Any foreign company with or without holding any shares in the target Indian Company can make an offer subject to a minimum offer size of 26 per cent.

- Only the acquisition of the equity shares carrying voting rights or any securities that entitle the holder to exercise voting rights require obligation of the open offer. Global depository receipts shall be covered under such securities.

- If the takeover is pursuant to any scheme of merger or amalgamation or reconstruction of the target company pursuant to an order of the court or Tribunal, open offer requirements shall not be complied with.

- A foreign company is also liable to make an offer to the listed Indian Company even if there is an indirection acquisition beyond the defined threshold limit

- Offer price shall be calculated on the basis of the frequency of the shares being traded on the stock exchange.

- The foreign company or the acquirer shall be required to deposit some percentage of the offer price in the escrow account before issuing any detailed public statement.

- The acquirer is also required to issue a letter of offer to all the shareholders of the company as on the identified date.

Case Example: Etihad’s Acquisition of Jet Airways

Initially, Etihad Airways, Dubai-Aviation Company, was supposed to make an open offer to acquire around 100% stake in debt-laden Jet Airways (if Etihad’s shareholding would have crossed 25%). However, considering the limit of Foreign Direct Investment of 49% under Government Route in Aviation Sector, it would have had to divest it to 49% following the open offer. Consequently, it wasproposed to give Etihad a three-month period to divest its stake to 49% as per the foreign direct investment norms.

Conclusion

Indian Company Acquisitions by Foreign Companies are highly governed and regulated. A web of legal compliance encompasses such acquisition. There shall always be a balanced view for all the Regulations that govern an Indian Company Acquisition.

For example, SEBI in its recent ruling took the financial sector by storm when it addressed that there would be no open offer exemptions to the companies not getting restructured through the IBC route. The lack of such exemption would increase the cost of buying a company for the buyer. Thus, foreign companies would be in a better position and standing if the target company restructures itself through the IBC, because it would be advantageous to them in terms of cost of buying a company.

Further there shall be a consensus between the SEBI(SAST) Regulations, and the RBI guidelines on foreign acquisitions, such that no provision overrides the other.

[1]https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11200

[2]https://rbi.org.in/Scripts/BS_FemaNotifications.aspx?Id=11161

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications