In this blogpost, Saumya Agarwal, Student, Amity Law School, Delhi writes about what are e-wallets, how is it used, benefits, uses of e-wallets and how are e-wallets governed in India.

What are E-Wallets?

E-Wallet refers to an electronic device that allows an individual to make electronic commerce transactions. E –Wallet is an online prepaid account where one can store his money and use it whenever he requires it again. As it is a preloaded facility. Consumers can buy a range of products. It is used to purchase items online with a computer or a smartphone. Nowadays, it is used to verify the holder’s credentials. For example, this e-wallet helps to authenticate the age of a person while he is buying alcohol.

E-Wallet is a feature exclusively for customers who have registered and established a My Account profile. E-Wallet allows you to store multiple credit card and bank account numbers in a secure environment. This saves the users’ time as he does not have to enter the card details again and again. This makes the payments faster, and user-friendly as the user does not have to type much.

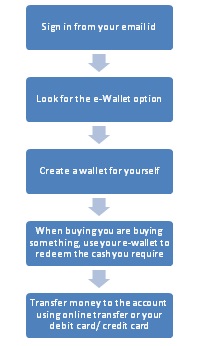

How to use it?

To use an E-Wallet these steps have to be followed:

Information stored in the E-Wallet:

E-Wallet stores all of the basic information for credit card, debit card and electronic check processing. For credit and debit cards, this includes the card type, account number and expiration date. For electronic check, this includes the account type, bank routing number and checking or savings account number.

Benefits:

E-Wallet saves the time of the user. The user does not have to look for the credit card/ debit card every time he/she makes a payment. The information is pre-filled. Also, the user can have multiple accounts. He can quickly select another credit card in case he has saved more than one set up in the account. The user can store up to 10 credit/debit card profiles and up to 10 bank account profiles in E-Wallet. The user can pass on the benefits of the e-wallet to his friends and family simply by sharing his account id and the password. Further, the user can delete, edit the information if there is a change in the account number or the account has expired with ease.

Where are the E-Wallets used?

- Recharging the Mobile Phones

- Fly Prepaid

- Utility Payments: Electricity bills, phone bills, hall seats

- Online Grocery Stores

- Buying Online

How are the E-Wallets/ Prepaid Payment Systems governed in India?

The prepaid payment systems are governed in India by the Reserve Bank of India, under the Payment and Settlement Systems Act, 2007.

According to Section 4 of the Act, no person other than the RBI shall commence or operate a payment system except under and in accordance with an authorization issued by the RBI under the provisions of this Act. The section applies to

- The continued operation of an existing payment system on commencement of this Act for a period not exceeding six months from such commencement;

- Any person acting as the duly appointed agent of another person to whom the payment is due;

- A company accepting payments either from its holding company or any of its subsidiary company or any other company;

- Any other person whom the Reserve Bank after considering the interests of monetary policy or efficient operation of payment systems, the size of the payment system or for any other reason, by notification, exempt from the provision.

Also, the RBI may authorize a company or corporation to operate or regulate the existing clearing houses or new houses of the banks in order to have a common retail clearing house system for the banks throughout the country.

Under Section 7 of the act, the RBI can issue or refuse to issue the authorization for operating the payment system under the act.

The things kept in their mind before issuing the authorization are:

- The financial status, experience of management and integrity of the applicant

- The procedure for setting of payment instructions

- The manner in which transfer of funds may be affected

- The terms and conditions including their security procedure

- The need for the proposed payment system or the services proposed to be undertaken by it;

- The technical standards or the designs

- Interest of consumers, including the terms and conditions governing their relationship with the payment system providers

- Monetary and credit policies

- Such other factors as may be considered to be relevant by RBI.

Further, the authorization issued should be in a prescribed form as-

- State the date on which it takes effect

- State the conditions subject to which the authorization shall be in force

- Indicate the payment of fees, if any, to be paid for the authorization to be in force

- If it considers necessary, require the applicant to furnish such security for the proper conduct of the payment system

- Continue to be in force till the authorization is revoked.

Every application for authorization shall be processed by the RBI as soon as possible, and efforts should be made to dispose of the application within six months from the date of filing of such application.

The RBI has the power to determine the standards of the functioning of the payment systems. Section 10 of the Act gives RBI the power to regulate the functioning.

The RBI may prescribe from time to time-

- The format of payment instructions and the size and shape of such instructions

- The timings to be maintained by payment systems

- The manner of transfer of funds within the payment system

- Such other standards to be complied with the payment systems generally

- The criteria for membership of payment systems including continuation, termination and rejection of membership

- The conditions subject to which the system participants shall participate in such transfers and the rights and obligations of the system participants in such funds.

Further, RBI may from time to time issue such guidelines as may be considered proper for efficient management of the payment systems or with reference to any particular payment system.

The RBI can revoke the authorization for the payment system, change the payment system by issuing a notice; it can call any system provider for such returns and documents or any other information in regard to the operation of his payment system. It also has the power to enter, audit and inspect any premises where a payment system is being operated. The information so received is confidential. The RBI has been given the power to generally give directions and any person to whom the directions are given should comply with them.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

Yes Vina,

This is called internet account, a variety of wallet generally used in an online sales/transaction portal.

Hi there,

Can you tell me whether the online accounts maintained by some websites for refunds come under the category of e-wallet?Since most of the features specified in this article apply to such online stores,and the accounts maintained by their regular customers on their website.