In this article, Parth Sarthy Kaushik discusses Financial Creditors vs. Operational Creditors and gives reasons on who is better off and why.

The Insolvency and Bankruptcy Code, 2016 (IBC) which has replaced the earlier ‘debtor in possession’ insolvency regime with a more expedient ‘creditor in control’ regime provides that in case of default of debt or interest payment by the corporate debtor, any financial or operational creditor (or corporate debtor) can make an application to the adjudicating authority (i.e. National Company Law Tribunal for companies, limited liability partnerships and other body corporates) under the Code for commencing the Insolvency Resolution Programme.

Once such an application is admitted by the NCLT, an interim resolution professional will be appointed and the authority will declare a moratorium period during which all pending and future legal actions against company will remain in suspension. During the moratorium period, the resolution professional is required to constitute a committee of creditors (excluding the related parties) which would include both financial creditors and operational creditors. The main purpose of the committee is to create a resolution plan within the stipulated time frame, in order to revive the corporate debtor. For this purpose, IBC provides that such a plan must have the approval of at least 75% of the creditors and a failure to approve resolution plan would by default lead to the initiation of liquidation proceedings.

For the purpose of proceedings under the Code, a distinction has been created between ‘Financial Creditors’ and ‘Operational Creditors’. It is pertinent to note that the Companies Act, 2013 does not create any such classification and only uses the term ‘creditor’. Further, this classification under IBC has been used to put the creditors on different pedestals at every stage of the proceedings whether they pertain to maintainability of applications, approval of resolution plan or distribution of assets (in case of liquidation). Therefore, with a view to secure their interests, it is imperative for creditors to be completely aware of the range of options/rights available to them under IBC.

Classification of creditors

Who is a Financial Creditor?

Section 5(7) of the Code defines a financial creditor as – “a person to whom a financial debt is owed and includes a person to whom such debt has been legally assigned or transferred“.

The term financial debt has been defined under Section 5(8) as – “a debt along with interest, if any, which is disbursed against the consideration for time value of money and includes:

- Money borrowed against payment of interest;

- Any amount raised by acceptance under any acceptance credit facility or its de-materialized equivalent;

- Any amount raised pursuant to any note purchase facility or the issue of bonds, notes, debentures, loan stock or any similar instrument;

- The amount of any liability in respect of any lease or hire purchase contract which is deemed as a finance or capital lease under the Indian Accounting Standards or such other accounting standards as may be prescribed;

- Receivable sold or discounted other than any receivable sold on non-recourse basis;

- Any amount raised under any other transaction, including, any forward sale or purchase agreement, having the commercial effect of borrowing;

- Any counter-indemnity obligation in respect of a guarantee, indemnity, bond, documentary letter of credit or any other instrument issued by a bank or financial institution;

- The amount of any liability in respect of any of the guarantee or indemnity for any of the items referred to in sub-clauses (a) to (h) of this clause“

Thus, all lenders who have extended any kind of loans, guarantees or financial credit are covered within its ambit.

Who is an Operational Creditor?

Section 5(20) of IBC defines an Operational Creditor as – “any person to whom an operational debt is owed and includes any person to whom such debt has been legally assigned or transferred“.

The term operational debt has been defined under Section 5(21) as – “a claim in respect of the provisions of goods or services including employment or a debt in respect of the repayment of dues arising under any law for the time being in force and payable to the Central Government, any State Government or any local authority”.

Thus, operational creditor refers to anyone who has provided goods or services and the payment for same is due from the corporate debtor. In the course of business, several transactions are entered into on credit terms customarily in different industries.

Thus, IBC creates the distinction between a financial and operational creditor based on the nature of transaction (i.e. purely financial transactions or transactions related to day to day operations) a creditor enters in with the corporate debtor.

Ability to start insolvency proceedings

Financial creditors can start insolvency proceedings even for disputed debts but operational creditors cannot

Based on whether the creditor is a Financial or Operational creditor, the Insolvency and Bankruptcy Code provides for different schemes of admission for insolvency petition which will initiate the resolution process.

Section 7 of IBC provides that a financial creditor can directly approach the adjudicating authority and the only condition that needs to be satisfied is that the creditor must show that the corporate debtor has defaulted in the payment of a due debt.

On the other hand, Section 8 of IBC lays down that for an operational creditor to succeed in initiating the resolution process, it must satisfy the adjudicating authority by demonstrating that:

- It has served a demand notice to the corporate debtor stating that the debtor has committed a default in debt; and

- No dispute exists between the parties in relation to the payment of debt.

The Hon’ble Supreme Court in Mobilox Innovations Pvt. Ltd. Vs. Kirusa Software Pvt. Ltd while interpreting the term ‘dispute’ as defined under Section 5 (6) and appearing in Section 8 (2) held that, the adjudicating authority is only required to see if there is a bona fide dispute in existence and it is not allowed to examine the merits such dispute. It is to be noted that this holds true even if the dispute notice has been served after the acceptance of demand notice by the corporate debtor.

Therefore, under the scheme of the Code, if a debt is not admitted by the organization (a corporate debtor) and is disputed within the meaning of Section 5 (6) or Section 8 (2), it is a sufficient ground to reject the insolvency application made by an operational creditor (i.e even if there are no pending proceedings between the parties, the corporate debtor can scuttle the insolvency proceedings). On the other hand, a financial creditor is allowed to initiate the resolution process even in case the debt is disputed by the corporate debtor.

Insolvency Resolution Process

Once the insolvency petition has been admitted by the adjudicating authority, Section 14 of the Code provides that a moratorium will be imposed on all judicial proceedings (both future and pending) against the corporate debtor until the approval of a resolution plan under section 31.

During the moratorium period, the Resolution Professional is required to constitute a committee of creditors which is tasked with the preparation of a Resolution Plan. This committee plays the most vital role in the insolvency resolution process as any resolution plan prepared and approved by it would be equally applicable on all the creditors. Thus, while the insolvency process can be initiated by any individual creditor, once the moratorium is imposed and Interim Resolution Professional appointed, the whole process becomes collective in nature, requiring a consensus among all the creditors for its success.

Operational creditors not permitted to be part of the Committee of Creditors

Section 21 (2) provides that the committee of creditors shall consist solely of financial creditors. The Code also lays down that each creditor shall vote in accordance with voting share assigned and the resolution plan can be implemented only if it has been approved by 75% of creditors. Further, Section 24 (3) (c) provides that only operational creditors having aggregate dues of at least 10% of the total debt shall be given the notice of the meeting. It is to be noted that, an operational creditor (irrespective of the claim size) is not allowed to be a member of the committee. Thus, IBC limits the right of an operational creditor to only attending the meeting of CoC subject to the abovementioned threshold.

Therefore, the Insolvency and Bankruptcy Code effectively confers only three rights on an operational creditor:

- To initiate insolvency resolution process.

- To receive notice of meeting of committee of creditors.

- To attend the meeting of committee of creditors.

It is to be noted that a resolution plan can be proposed by any category of creditors. However, it must be stressed that the same needs to be approved by the committee which is controlled by financial creditors. Therefore, unlike financial creditors, the rights conferred on the operational creditors are subject to certain conditions which resultantly gives more weightage to the concerns of financial creditors by giving them total monopoly over the entire resolution process.

Liquidation and Asset Distribution

Unsecured Financial Creditors and Operational Creditors are on Par, But Secured Financial Creditors Have a Priority

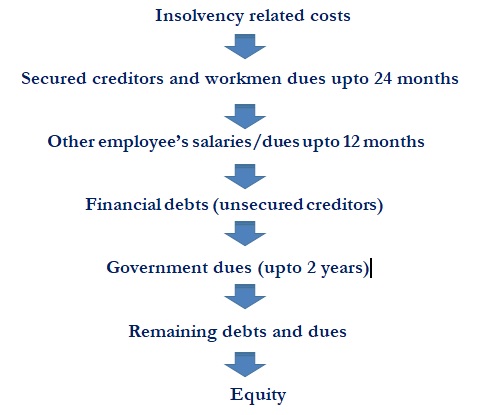

In case the committee of creditors fails to approve a resolution plan within the stipulated time period or demands liquidation, the adjudicating authority will pass an order for liquidation of the corporate debtor. The official liquidator appointed by the CoC is then required to sell the assets of the corporate debtor and distribute the proceeds among all the creditors. Section 53 provides that the order of priority for the distribution of assets shall be:

While a financial creditor can be either a secured or unsecured creditor, an operational creditor always falls in the category of unsecured creditors. Therefore, even in the case of liquidation and asset distribution, financial creditors are prioritised over operational creditors (excluding workmen and employees, who are operational creditors but are specified to be treated equally with secured financial creditors).

Conclusion

The rationale behind this imbalance in the rights assigned to financial and operational creditors under IBC has been explained by the Banking Law Reforms Committee in its report, which states that:

“….members of the creditors committee have to be creditors both with the capability to assess viability, as well as to be willing to modify terms of existing liabilities in negotiations. Typically, operational creditors are neither able to decide on matters regarding the insolvency of the entity, nor willing to take the risk of postponing payments for better future prospects for the entity. The Committee concluded that, for the process to be rapid and efficient, the Code will provide that the creditors committee should be restricted to only the financial creditors.”

Therefore it is clear from the above position that framers of the Code created this classification with the aim to protect the rights of all stakeholders by providing a mechanism which primarily focuses on resolution and re-structuring of the debt by treating the corporate debtor as a going concern and provides for liquidation only when all the attempts towards such a resolution ultimately fail.

This approach is certainly much more rational than giving the reigns of the resolution process in the hands of Operational Creditors who are more than often not interested in the revival scheme and look for the obvious solution of liquidation to recover their dues which would defeat one of the main objects of the Code that is, to allow an honest but unfortunate corporate debtor to obtain a discharge from his debts subject to reasonable conditions.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

https://t.me/joinchat/J_

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

A crystal-clear articulation of a much recondite topic..

great work

It is a good paper, overall, but not well-edited. The author/authoress knows that Operational creditors cannot become members of the CoC in CIRP, yet allows an erroneous statement to remain in the paper that CoC consists of FCs and OCs.

I compliment the writer for the lucidity of language.

I would like to request the writer to share a contact number, to be used only for professional communication. Mine is 98312-36625.

I was going through the blog / article “Financial Creditors vs. Operational Creditors – Who is better off and why?”

Since the Financial Creditors have complete authority over conclusion of resolution or liquidation, they are likely to take care of only their dues without heeding for operational creditors.

How this aspect is taken care of in the law?

The “Distribution of Assets” chart given in the article does not show level of “Operational Creditors” in the hierarchy. Where do they stand – is it the last portion – Remaining debts and dues?

I presume – as an ex-employee – I will be considered as “other employee”. The dues of 12 months payable are months preceding the conclusion of liquidation or it can be a 12 months of historical period – e.g. January 2016 to December 2016?