In this article, Kashish Khattar discusses All you need to know about Fintech in India. Kashish is a 4th-year student at Amity Law School, Delhi. This article is a discussion revolving around the FinTech space and the regulations surrounding them.

Introduction

You would have heard of Berkshire Hathaway’s investment into Paytm recently. According to a Livemint article, it was Warren Buffett’s first investment in the country. Berkshire invested Rs 2500 Cr in the parent company of Paytm i.e One97 Communications Ltd, this gives the company a valuation of USD 10-12 billion. Further, the Indian fintech software market is forecasted to touch USD 2.4 billion by 2020 from a current USD 1.2 billion, as per NASSCOM. The transaction value in the FinTech space was recorded around USD 33 billion in 2016 and is expected to shoot up to USD 73 billion by 2020. According to an EY report, India is just behind China in the adoption of FinTech services in the world. The adoption rates are through the roof, the EY report states that the sample in the survey done by this particular report had used 2 FinTech services in the last 6 months.

According to a livemint article, the FinTech Industry in India can be divided into 12 broad categories and they can be listed as follows:

- Alternative Funding;

- Banking Tech;

- Crowdfunding;

- Consumer Finance;

- Cryptocurrency;

- Enterprise Finance;

- Foreign Exchange;

- Insurance Tech;

- Investment Tech;

- Mobile Wallets;

- Payments; and

- Software for Institutional Investor.

Reasons for rapid growth

The FinTech industry’s rapid growth can be attributed to the holy trinity of India’s Fintech revolution: The Banks, Government and Startups. Let us now analyse all these three aspects and how they helped in the exponential growth of the FinTech space in India.

- Government – The Central government’s push towards a cashless digital economy through its various policy initiatives has helped in laying a strong foundation for the FinTech sector in the economy. These factors can be listed as follows:

- India Stack – With the introduction of India Stack, which is basically a set of APIs that allows governments, businesses, startups and developers to utilise a unique digital infrastructure. The government has tried to introduce a world-class technological framework to the startup sphere, innovators and MNCs which would, in turn, accelerate the growth of the FinTech space in the country. The scenario is just like the policy support given by the government in the late 1990s to the Telecom industry which took paramount importance in many reform initiatives of those times.

- Startup India – The startup India program as launched by the Centre includes various tax exemptions, simplification of regulations, reforms to the patent regime, mentorship and a substantial increase in government funding.

-

- Pradhan Mantri Jan Dhan Yojana – Financial inclusion drives such as the PMJDY is regarded as the world’s biggest financial inclusion program which had a target to get basic banking activities to the underserved section of the Indian population.

- Adoption of Aadhar – You would know about RBI’s KYC norms involving Aadhar based biometric authentication which will make opening a bank account to be a hassle-free task.

- National Payments Council of India Initiatives or the NPCI – With the introduction of Unified Payment Interface or UPI, the NPCI has tapped into the exponential growth of the mobile phones and the Jio revolution and in turn, reduced the cost of infrastructure for the FinTech startups. The smartphone user base which is expected to touch about 500 million users by 2020, from about 150 million users in 2016. This aggressive growth will ensure a bigger digital banking footprint in the economy. The NPCI has come up with numerous innovative initiatives which give a solid base for a digitally enable FinTech sector in the country. Which gives the startups in this space, to leverage this time and the numerous opportunities to grow and be adopted as mainstream banking activities. Services such as Digital KYC, BHIM (Bharat Interface for Money), Bharat Bill Payments Scheme (BBPS), Aadhar Enabled Payment System (AEPS) are all trying to ease the process of digital payments for all classes of people in the Indian society.

-

- Public Relations – Centre has also marketed the whole digital monetary system well. Space still requires regulations for various FinTech industries such as the P2P transactions, crowdfunding and data security. PM Modi’s formula of IT + IT = IT (Indian Talent + Information Technology = India Tomorrow) can be seen as the government’s stand on the digitisation of every sector including the finance field.

- Effects of Demonetisation – The FinTech space got a major boost due to the sudden announcement of Rs. 500 and 1000 notes were demonetized by the Prime minister on 8th Nov 2016. The e-payments and e-wallet system saw a boost of 500% in terms of traffic in the first few months. Government data states that 1.7 mn transactions were done by these e-wallet services in the first month after the announcement of demonetisation. Approximately, 46% of the FinTech space are involved in the payment services business.

- Regulators – The four main regulators who will be taking care of the FinTech space will be the Reserve Bank of India, Securities and Exchange Board of India, the Telecom Regulatory Authority of India (TRAI) and finally, the Insurance Regulatory and Development Authority (IRDA).

- Startups – India’s Fintech space got it’s much-needed attention in 2016 and has been growing ever since the Payments sector got a boost after the Demonetization. Alternate lending also has been enjoying a good growth rate because of a number of unbanked, new to the bank, underbanked consumers. But the FinTech system still has a lot of scope for growth, let us look at the various sectors in the startup sphere of the FinTech space:

- Payments – The digital payments sector in the country is expected to grow to USD 500 billion by 2020, representing around 15% of the GDP. It is estimated that 80% of the economic transactions in India still happens through cash, whereas it is 21% for developed economies. This leaves a significant room for growth. There was a rapid growth in transactions in the year 2016-2017 and has grown ever since. Mobile payments applications such as wallets, P2P transfer applications and mobile points of sale are as popular as ever and they have a strong user adoption rate among the tech-savvy youth of the country. Some players in the FinTech space are taking advantage of different and innovative policy initiatives such as Payments Banks. Basically, a model of a modern bank to serve the unserved which blends together both mobile services and the traditional banking services.

- Alternative Lending – Alternative Lending is said to the second most funded and one of the fastest growing sectors in the Indian FinTech space. As of October 2016, alternate lending in India had received USD 199 million in funding across 33 deals.

- P2P lending has emerged to be the most sought out startup idea of the FinTech system. P2P has the characteristics of everything FinTech solution – it is quick, cheap and meant for the greater good. After the 2008 financial crisis, banks have become risk-averse, loans have got tougher to obtain and the banks have altered their own operations. P2P is the solution to this problem, the major contributors to this growth are the unmet demand loans by MSMEs with a gap of roughly USD 200 billion in credit supply. It is a really inexpensive model that runs on a sense of social responsibility. P2P is here to stay and has all the prerequisites to grow exponentially in the Indian society.

- InsurTech – The insurance sector in India has not been the easiest sector to accept innovative products, but with the customers asking for a bang for their buck and an increased access to technology-enabled efficiencies. The insurance companies are not looking out to incorporate technologies and products that improve basic factors of customer engagement, retention and improving the complete customer lifecycle. Internet-of-Things or IOT has gained quite some reputation in the InsurTech sector, which is powered by extensive customer data. Linking of data of health and wellness can help the insurers to predict the know-hows of customer behaviour and lead to an increase in their earnings through better pricing strategies.

- Wealth Management – The asset and wealth management will witness a wave of automation, and so will India. The technological advancements have to lead to a better product offering. The rise of e-payments, e-KYC through Aadhar and online fund transactions, online statements of investments have made the future of an automated wealth management sector quite bright. India’s young and largely under-banked population has been largely absent from the stock and the bond markets and this present quite a room for improvement for players in this sector. Furthermore, SEBI and RBI have encouraged simplicity. All in all, this has lead to quite a lot of users being guided towards formal investments.

- Banking Technology – Financial Institution has been investing heavily in emerging technologies to improve the customer experience, their internal operations etc. Globally, it can be seen that large commercial banks are investing in Artificial Intelligence, Machine Learning and Blockchain startups for both back office and front office purposes.

- Blockchain Tech – Blockchain based system offer vastly improved trust and transparency and due to its regulatory uses, the adoption of Blockchain or Distributed Ledger Technology (“DLT”) in the Indian banking sector is also finding some traction and support from the regulatory bodies. DLT in India presently has only reached the proof of concept stage, where a commercial bank is trying it out to enforce a smart contract, its application in remittances and trade finance. DLTs are overall attractive from a regulatory and audit point of view. The three main applications of the DLT in the coming future could be: (i) Efficient payments transfer infra; (ii) Enforcement of smart contracts; and (iii) Digital Identity i.e. a tamper-proof history of a transaction and gives the users an option of choosing who to give access to their personal data.

- AI and ML – Artificial Intelligence (“AI”) and Machine Learning (“ML”) are all set to disrupt the Banking sector in India in the near future. AI can be explained as a bigger and broader concept which relates to machines doing activities that we consider to be smart, while MI is one of the particular applications of AI which basically learns from the data given to it to make predictions and inferences that can be used by the user. AI can have a lot of applications in the banking sector ranging from customer acquisition, KYC and Onboarding, Accounts and Loans, Customer Service, Brand Management, to Risk and Credit etc.

Click here

Legal framework governing the Fintech Space

Most of the sectors in the Fintech space are not yet regulated. Sectors such as P2P lending and payments systems are some of the sectors that need to be regulated on an urgent basis because they handle public money. P2P lending does not fall under the regulatory framework of the RBI. Therefore, these alternative lending entities have quite an edge over banks and financial institutions who charge higher rates of interest and demand a collateral.

However, the alternative lending platforms do fall under the Usurious Loans Act, 1918. This Act has given the power to the courts in India to intervene in cases where the interest rates are really high, which basically keeps a check on unfair rates of interest. Further, almost 22 states have different and separate acts on money lending to be complied with. Furthermore, the platforms also need to have a license from the state under the Act to carry out the business of lending.

RBI has gone ahead and regulated with some sectors of the Fintech, which mainly include the e-wallets and payment services. These entities have to be registered with the RBI under the Payment and Settlements Act, 2007. The RBI has made sure to have stringent rules and regulations regarding these. This ensures the security of the information given and the public money at large, which are basically moved around through the means of the FinTech space. Apart from these, there has not been much of regulation in any of the other sectors of the FinTech space. This does put an opportunity in the hands of the regulator and the businesses to try different approaches.

The RBI has as per its press release of 14th July 2016, set up Inter-regulatory Working Group on FinTech and Digital Banking to review and appropriately reorient the regulatory framework and respond to the dynamics of the rapidly evolving Fin Tech scenario.

Various security risks faced by the FinTech space

There are a number of risks faced by the Fintech Companies at present. There are various new avenues that have come up due to the evolution of the FinTech revolution. You must have heard of the all the famous line that data is the new oil. The most valuable thing in the world is not a fossil fuel, but sensitive information collected by apps from its users. The more FinTech revolution spreads nationwide, the more will be the amount that they deal with. As more people go online, things like data ubiquity, data security are becoming a major challenge for the FinTech industry. A tremendous amount of data is gathered by the FinTech space, which is then analysed to gather insight into more of customer buying patterns and retention strategies. This includes a lot of personal data, including financial, health, and social data of a user. Protection of this kind of data is the need of the hour. Seamless data is another avenue which helps survive the dynamics of the partnerships formed between Financial Institutions and the Fintech space. They have provided the users with better products at better prices and have improved the existing products and services also. Another challenge that is faced by the FinTech space can be of data ownership. This kind of a risk must be overcome through a combination that consists of both technical and legal measures. Furthermore, trying to manage customer access to various solutions and services becomes a lot more complicated for the ever-increasing customer base. Options of cyber security concepts like data labelling, selective data sharing and identity-aware data shareholding can be solutions to various risk-related problems for this space.

FinTech Companies v. Financial Institutions

The Fintech Space has really evolved over time with the emergence of multiple mature players especially in the payments segment and consumers giving preference to new innovative products that offer different financial services. This puts the FinTech companies in direct competition with the traditional large bank and financial corporations. The ecosystem by no doubt has shifted from a traditional competitive edge where the financial institutions introduce their own products and services to compete to more of a collaborative one. Where both the startups are looking for growth with the help of Large institutions who have been in this game for very long. And open innovation and new ideas can be adopted by big institutions. The financial institutions have realised over time that collaboration with the FinTech industry is more an effective strategy than competing with them. These institutions now even embrace the disruption that this space is creating in the financial world.

Basically, institutions are trying to blend existing technologies offered by the FinTech space in their operations or are developing their own innovative solutions in partnership with various startups. Partnering with a FinTech startup allows the institution to effectively outsource their research and development and develop services that can be introduced and brought to the market quickly. Which in term also makes them gain access to different technologies that can build solutions for bigger and better problems they may face in the future. The FinTech scene benefits from this partnership with the access to the large customer base of financial institutions as well as their management and deployment capabilities. Collaboration makes sense for startups as they have to compete in the marketplace where a lot of similar services are already being offered by major telecom or public sector players.

The methods by which Indian financial institutions use while working with new FinTech technologies can be summarised as follows:

(i) Supplementary Offering – Use of new or existing subsidiaries to offer new services;

(ii) Partnerships – where both the parties develop solutions together;

(iii) Acquisitions – of various startups and enhancing their value;

(iv) Incubation – Where you run startup programs to incubate companies relevant to the market they are involved in;

(v) Investing – Setting up of venture funds to invest in the FinTech space; and

(vi) Bridge makers – Bridging the gap between demand and supply by curating the best business ventures to meet the needs of the market.

The road to collaboration is not an easy one, there are a couple of hurdles that have to bridged by both the parties to come up to a suitable solution. The obstacles arise from the new challenging the old, the different business models of both the businesses, a difference of the culture between both the places. Institutions have a problem because of their slow adoption of change and innovation, their slow acceptance to disruption in the market. The difference also arises in terms of goals where FinTech wants to bring in new levels of efficiency in what they do, whereas Institutions have to go slow and steady as they have to take care of the whole range of products and services required in the transaction. However, these challenges can be overcome and make way for a highly promising future for both the FinTech space and the financial institutions. Opportunities for collaboration and growth will only grow over time and there will be so much room for innovation and disruption.

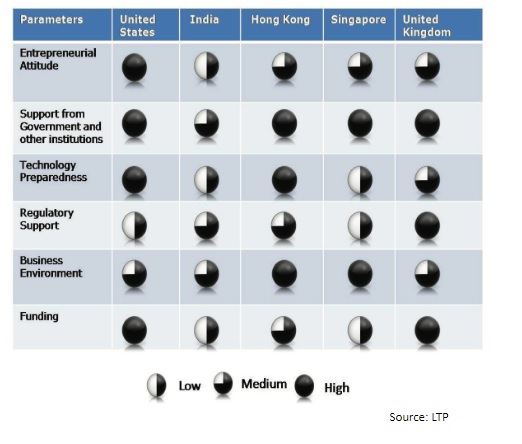

(A graph comparing India v. Other FinTech hubs globally.)

Conclusion

India needs to regulate, invest, and promote its business, startup environment only after which it can emerge as a startup haven. It has got a huge potential to change into a developed economy. FinTech space has made use of new technologies and disruptive approaches to come up with better and innovative products. This trend is expected to continue and go bigger in the coming years. Banks will go through a revolutionary change with AI and MI in the centre of all the disruption that will happen in this sector. Wealth management which consisted mainly of high net worth individuals now has room due to cheaper services to advise more customers in the coming times. There is automation in Corporate and Investment Banking, which has led to cost reduction and improved efficiency in all major banks. India is on the cusp of the FinTech revolution, accelerated in part by the Government’s policy initiatives and development of the Indian Stack. India’s vast underbanked and new-to-bank population makes it the most exciting opportunity place to be in right now. It is now to be seen as to how the FinTech revolution is going to change the habits and behaviour of the Indian population.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

This writer is a student of 4th year of law.

But has wrote this article like a well versed lawyer.

Good !