Written by Saloni Mathur, pursuing Certificate Course in Insolvency and Bankruptcy Code offered by Lawsikho as part of her coursework. Saloni completed her course in Company Secretary and is currently employed with S R Ashok and Associates Pvt. Ltd. as the Manager of Finance and Legal Department.

Introduction

Some days ago, I was surfing some good reads on Bankruptcy and I found this very interesting statement by Ernest Hemingway,” How did you go bankrupt? Two ways, gradually, and then suddenly.” I can to an extent, apply the same to define the key of Bankruptcy in India, i.e the Insolvency Resolution mechanism as defined under the IBC, 2016. When all the efforts of its predecessors like Debt Recovery Tribunals, SICA, and SARFAESI proved to be ineffective, IBC entered the scene gradually, and then suddenly as a pressure tool for recovery.

Keeping the very nature of the Insolvency and the Bankruptcy code, 2016(hereinafter referred to as “IBC, 2016”) intact, M.S Sahoo, Chairman of Insolvency and the Bankruptcy Board of India, (“IBBI”) in one of his interviews with the leading newspapers said, ”Focus shall be resolution, not liquidation.” It definitely goes without saying that the IBC, 2016 was one of the most landmark moments in the history of India. When the Non-performing asset crisis burgeoned between 2008 and 2014, it became one of the hardest nuts to crack for the government officials. The SICA and the establishment of the Debt recovery tribunals had proved to be an ineffective mechanism due to substantial hurdles in its implementation, until a dynamic mechanism i.e the IBC came into force.

Though the very characteristic of the code was to promote resolution over liquidation, over two years of its implementation, one cannot deny the fact that IBC, beside its primary role of providing resolution for stressed companies, has also proved to be a strong pressure tool for recovery of dues of the creditors.

This article is an attempt to contemporarily analyze IBC as a mechanism to pressurize recovery for the dues of the creditors while how far it has been successful in maintaining the balance of its stakeholders and protecting the very interest of the code.

Current Statistics at a Glance

As per the Quarterly Newsletter of the IBBI ending 30th September, 2018, a total of 1198 applications were admitted by the NCLT for the calendar year 2018, out of which 118 applications were closed on appeal/review, 52 were closed by the resolution and 212 were closed by the liquidation, and 238 applications are undergoing Corporate Insolvency Resolution Process (“CIRP”). The notable fact here is that out of 212 applications under the CIRP, 238 have already crossed the deadline of 180 days of the CIRP process as mentioned in IBC, 2016

The status of CIRP at a glance

Figure 1.1

| Admitted since January 2018 | Number of CIRPs |

| Admitted | 1198 |

|

Closed on appeal/review |

118 |

| Closed by resolution | 52 |

| Closed by liquidation | 212 |

| Ongoing CIRPs | 816 |

Source: IBBI Website, Quarterly Newsletter (30th September, 2018)

Resolution Mechanism-Nipping the Cases in the Bud

The most interesting aspect of the Insolvency resolution mechanism that has been witnessed since its enforcement is the threat amongst the defaulters for initiation of the corporate insolvency process against them, if they default in payment of the debts amounting to Rupees One lakh or above. The various facets of the process have been so defined that each is a labyrinth in itself. Defaulters are well aware of the fact that once the Application by any financial or operational creditor is admitted in the NCLT, the entire management loose hands in the affairs of the company and the Insolvency professional takes charge as a going concern.

Two years broadly have been more than satisfactory. The impressive of all is that the defaulters are coming up even before the admission and paying up and settling, for the fear and the consequences of the IBC. Thus if an Application under Section 7 of the IBC by a financial creditor is admitted, the management is sure to lose the affairs of the company, and if the resolution plan fails to get approved by the committee of creditors formed primarily of the financial creditors, the company goes into liquidation.

One of the landmark moments in the history of the IBC was the insertion of Section 29A by way of the Second Amendment Act, 2018 which prescribes non admission of resolution plans of the promoters and their related parties in the company, thereby relieving the management of the company from the hands of people responsible for its doom. It is needless to say that this mechanism has proved to be a pressure tool for recovery. The defaulters in the fear of taking back the control are paying the debt at the pre-admission stage, in a fear of losing the stake in the company. This has fairly resulted in nipping the application process in the bud, and that apparently portrays the bright side of IBC.

Applauding the CIRP

With the insolvency resolution mechanism in place, Rs.80,000 crore has been recovered by the creditors in 66 cases resolved by the NCLT and some of the big 12 cases such as Bhushan Power and Steel and Essar Steel are in the advanced stages of resolution and Rs.70,000 crore is expected to be recovered in the next financial year.

The schemes and the incentives which the Insolvency resolution mechanism possesses have brought in behavioral changes on the part of the stakeholders, and minimizing the incidence of the failures and the default. The Amendment in the CIRP regulations on 4th July, 2018 had specified timelines for each activity ranging from public announcement to proof of claim admission, verification, submission of resolution plans etc. Thus, by setting the internal timelines, IBBI has been quite effective in working as a pressure tool for the recovery. For example, IBC has to an extent tarnished the image of the Bhushan Steel and its stakeholders, where the management is continuously changing hands. This has put a pressure on the debtors to repay the dues on time.

A trend can be seen where the applications are being withdrawn before their admission in NCLT. According to an extract from an interview with Mr. M.S. Sahoo( Chairman, IBBI) creditors have recovered more than 1 lakh crore if they are following this route. The banking sector is making a pretty good recovery outside the IBC. Over 2000 applications have been closed prior to their admission.

Till date, the IBC has been successful in resolving cases amounting to debt of Rs.3 trillion comprising Rs.1.2 trillion at the preadmission stage and about 600 billion NPAs that turned into the standard accounts.

Is Insolvency Resolution Mechanism more effective than its predecessors?

The average recovery in the 60 resolved cases under the IBC is around 47 percent as against 26 percent under the earlier board for industrial and financial reconstruction (BIFR).

Another important section, to take the bull by the horns, is the invocation of Section 74 of the IBC that prescribes penal provisions for violation of the moratorium by the officers of the corporate debtor, creditors and bidders, and failure to comply with the resolution plans by the resolution applicants. In the case of Amtek Auto(the corporate debtor and the Liberty House (Resolution Applicant) for the Amtek Auto, The Liberty House failed to comply with the resolution plans and the Amtek Auto decided to invoke section 74 of the IBC. The purpose fairly acts a pressure tool for recovery as it protects the code from being taken lightly, and also infuses some pressure in the stakeholders to the transaction.

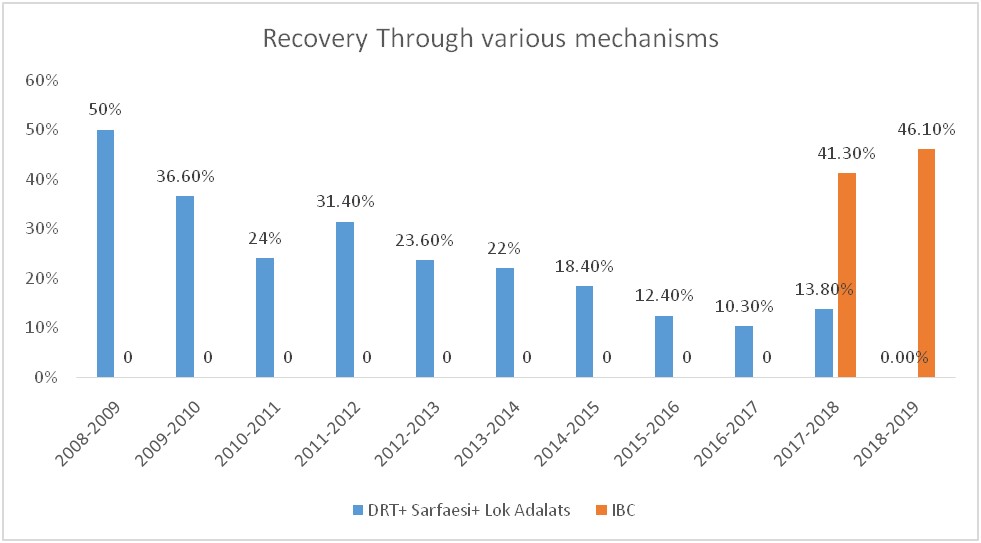

A Glance at the recovery through various mechanisms

Source:IBBI and RBI, Data on average recovery for DRT, Sarfaesi, and Lok Adalats is not available

It is notable that the average recovery by the banks, based on the data available, through the IBC was 41.3% in FY-18 against 13.80% through other modes of recovery. The recovery through SARFAESI stood at only Rs.26,500 crore as against IBC which stood at Rs.9,92,900 crore. The recoveries through the DRTs and the Lok Adalats were even lower which stood at 7200 crore or 5.4% and Rs.1800 crore or 4% respectively.

The latest quarterly report of the IBBI reveals that out of the 12 cases resolved under its regime, the average recovery as percentage of total claims filed by the financial creditors was quite high i.e 69.7%. Cases such as Kohinoor CTNL Infrastructure owed Rs.2528 crore to the financial creditors and they could recover Rs.2246 crore or 89% of the total claim amount. Cases like Forward Shoes, Trinity Auto Components, and Propel Valves, recovered full amount to the financial creditors. Two cases sound exceptionally successful. Burn Standard Company and Shree Radha Raman Packaging recovered more than the amount due.

Instances of Recovery through IBC Mechanism

The threat which the IBC possesses is a recovery mechanism in itself. The legal notices or the threatening notices being sent to the debtors are rendering them between the devil and the deep sea, whereby they are leaving no stone unturned in the paying the dues of the creditors.

If one analyses the Corporate Insolvency Resolution process deeply, then each section has an important role to play. The various provisions of admission of application in the NCLT have been structured in such a way that the debtors are left with limited options and benefits to prove their innocence against the application filed by the financial creditors. The debtors are left with no options other than to repay the debts of the creditors.

Conclusion

The Insolvency resolution mechanism has been successful to quite an extent in preserving the interests of its stakeholders. Though the motive of the mechanism is not recovery, but it has successfully acted as a pressure tool of recovery. The number of applications being withdrawn before the pre-admission stage is quite high in number.

The provisions of the resolution mechanism are strictly time bound which are exerting pressure on entire stakeholders to comply with the ideology of the code. There are strict penal provisions as defined in section 74 of the IBC, 2016 for violations on the part of the officers of the corporate debtor, the creditors and the bidders. The approval of the resolution plans is governed in such a way that failure by the committee of creditors to approve the plan, would lead the company into liquidation.

It’s been two years to IBC, and so far the performance has been more than satisfactory. Needless to say that, the code has been demonstrating multifarious interests and things are changing gradually. One can see and analyse the arrows being thrown in all the directions by the Insolvency mechanism, leaving debtors between a rock and a hard place.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications