This article has been Vijay Shekhar Das.

Abstract

Since, Sec.238 of Insolvency & Bankruptcy Code 2016 (hereinafter be referred as “IBC 2016”) and sec.35 of Securitisation and Reconstruction of financial assets and Enforcement of Security Interest Act,2002 (hereinafter be referred as “SARFAESI Act 2002”) gives overriding effect of the abovementioned acts over other laws, this caused cropping of the confusion that whether with the commencement of the moratorium under IBC 2016, Bank can enforce security interest under chapter III of SARFAESI 2002 against corporate debtors and personal guarantor/s. This confusion seems to have been abated with the decisions of PR. Commissioner of Income Tax vs Monnet Ispat & Energy ltd[1]. and State Bank of India vs V.Ramakrishnan & Anr[2]. From the decisions of these recent cases it becomes clear that Banks/Financial Institutions cannot proceed against the corporate debtors under SARFAESI Act 2002 to enforce their security interest during pendency of moratorium u/s 14 (1)(c) of IBC 2016,but, this does not preclude them in proceeding against personal guarantors u/s 13(11) of SARFAESI Act 2002.Moreover, as NCLTs are not generally aware of the proceedings pending in DRTs when they accept application under section 10 of IBC 2016 it unnecessarily deprives Banks from getting their dues back from corporate debtor for a considerable period of time. Thus, this incongruity in the functioning of the two tribunals must be weeded out for want of which whole purpose of bringing about IBC 2016 & SARFAESI Act 2002 would fail.

Introduction

Background

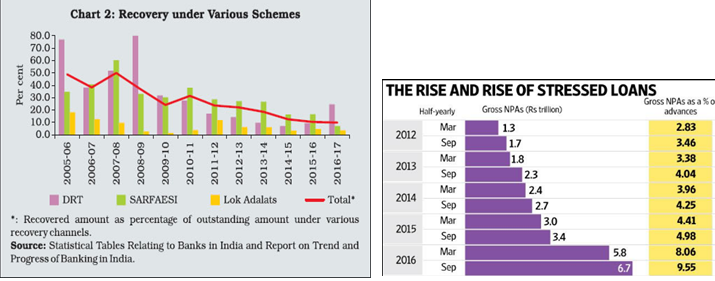

As on 30th of September 2016 India’s Non Performing Assets[3] (hereinafter be referred as ‘NPA’) shot up to 9.1% of its total lending by Banking sector in India. Due to these NPAs, banks were starved of cash flows, which coupled with stringent provisioning norms had led to losses / reduced profits. This made it quite evident that all existing laws esp. SARFAESI Act,2002 which was considered to be panacea for Banks against bad loans, have miserably failed to quell this rising NPAs (esp. because length of time consumed in the completion of proceedings under various acts have had been interminable) and there was an urgent need to overhaul the present system to avert impending collapse of Banking system in India.

(Source- Capitaline[4])

Table.1 (Above shows how NPAs have gradually increased while recovery under various schemes remained meagre.)

Thus, in the backdrop of above, government of India undertook a plan to replace existing insolvency laws with one consolidated and comprehensive law that would facilitate easy and time bound resolution / liquidation of business entities in distress. On 11th May,2016 the Rajya Sabha passed the major economic reform bill moved by the Government that is Insolvency and Bankruptcy Code 2016 (hereinafter be referred as ‘IBC 2016’). Lok Sabha had already passed the bill on 5th May,2016.

In the words of Bankruptcy Law Reforms Committee of Nov 2015, as mentioned in its Para 3.4.2 following are the principles on which new insolvency and bankruptcy resolution framework was designed:

“I. The Code will facilitate the assessment of viability of the enterprise at a very early stage.

- The Code will enable symmetry of information between creditors and debtors.

III. The Code will ensure a time-bound process to better preserve economic value.

- The Code will ensure a collective process.

- The Code will respect the rights of all creditors equally.

- The Code must ensure that, when the negotiations fail to establish viability, the outcome of bankruptcy must be binding.

VII. The Code must ensure clarity of priority, and that the rights of all stakeholders are upheld in resolving bankruptcy.”

Research Problem

Can Security Interest u/s 13 of the SARFAESI Act 2002 be enforced after the commencement of moratorium u/s 14(1) of Insolvency & Bankruptcy Code 2016?

Scope & Limitation of the present study

This paper focuses on whether or not Banks can enforce security interest u/s 13 of SARFAESI Act 2002 against corporate debtor(defined u/s 2(8) of the IBC 2016) and personal guarantor(defined u/s 5(22) of the IBC 2016) after commencement of Moratorium u/s 14 of the IBC 2016.

In this study researcher has used doctrinal research and no empirical study has been done by the researcher. In absence of any commentary in the library regarding IBC 2016 this research is mainly based on pertinent contents available online (including various government/RBI reports).

Furthermore, present study is limited to moratorium as mentioned in Part II chapter II u/s 14 of IBC 2016 which deals with moratorium which prohibits various legal proceedings mainly against Companies and does not discusses moratorium as discussed u/s 96 and 101 of Part III chapter III of the IBC 2016.

Understanding the source of the Problem

As per this code of 2016 i.e. IBC 2016, time limit for the completion of Corporate Insolvency Resolution Process ( which is the process of resolution of insolvency of a corporate debtor as provided under this code) is 180days + extended period of 90 days i.e. total 270 days[5].To ensure the success of Corporate Insolvency Resolution Process (hereinafter be referred as ‘CIRP’) (which eventually causes passing of resolution plan or commencement of liquidation proceedings) the code provides for ‘Moratorium’ u/s 14 of the code which has effect of preclusion of all legal proceedings against the corporate debtor till CIRP finishes (which also causes a corporate debtor to postpone any payment to be made to creditor). Thus, moratorium is a calm period during which there is no further action by creditors or other persons towards recovery of debts from the corporate debtor.

The commencement of moratorium is very essential in achieving the one of the avowed principles on which new insolvency and bankruptcy resolution framework was designed as posited by Bankruptcy Law Reforms Committee of Nov 2015 in its report as “ IV. The Code will ensure a collective process” which in the own words of Committee means:

“The law must ensure that all creditors who have the capability and the willingness to restructure their liabilities must be part of the negotiation process. The liabilities of all creditors who are not part of the negotiation process must also be met in any negotiated solution.”

From above, it can be inferred that IBC 2016 was mainly brought up not just to take care of interest of one specific bank but to secure the financial interest of all kinds of creditors who are stakeholders in proper functioning of debtor company.

Section 14(1) makes mandatory on the part of Adjudicating Authority[6] to declare moratorium by an order prohibiting under sub- clause (c) following :

“any action to foreclose, recover or enforce any security interest created by the corporate debtor in respect of its property including any action under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;”

Contrasting, Sec 14(1) read with Section 238 of IBC which reads as:

“The provisions of this Code shall have effect, notwithstanding anything inconsistent therewith contained in any other law for the time being in force or any instrument having effect by virtue of any such law.”

with sec. 35, which is a similar provision under SARFAESI Act 2002 as provided u/s 238 of IBC 2016 which reads as:

“The provisions of this Act to override other laws.—The provisions of this Act shall have effect, notwithstanding anything inconsistent therewith contained in any other law for the time being in force or any instrument having effect by virtue of any such law.”

The question which crops up is which law shall prevail in case when there is any clash between the two in the sense that whether or not during the subsistence of moratorium Banks can enforce its security interest (as defined u/s 2(zi) of the SARFAESI Act 2002) provided u/s 13(4) of chapter III of the SARFAESI Act 2002 against corporate debtor (defined u/s 3(8) of the code) & personal guarantor (defined u/s 5(22) of the code). This can be better understood if this issue is seen in following two scenarios:

(a.) Position before IBC 2016. (b.) Position after IBC 2016.

(a) Position before IBC 2016

Before the advent of IBC ,2016 position was that a secured creditor was not required to get the leave of the Company Court/Official liquidator thus, while remaining totally aloof to winding up /liquidation proceedings, it could successfully enforce its rights provided under SARFAESI Act/DRT Act. In case there is any case pending in the Company Court/Official Liquidator, it was required to be transferred to the Debt Recovery Tribunal (hereinafter be referred as ‘DRT’ as mentioned u/s 3 of The Recovery of Debts Due to Banks and Financial Institutions Act, 1993 (hereinafter be referred as ‘RDDBFI Act,1993’)).This is manifest by following judgments

Allahabad Bank vs Canara Bank and Anr;[7]

At page no. 14 para 1 of the Judgement Apex Court said :

“The provisions of the RDDBFI Act,1993 are to the above extent inconsistent with the provisions of the Companies act, 1956 and the latter Act has to yield to the provisions of the former. This position holds good during the pendency of the winding up petition against the debtor-company and also after a winding up order is passed. No leave of the Company Court is necessary for initiating or continuing the proceedings under the RDB Act, 1993. Thus, on questions of adjudication, execution and working out priorities, the special provisions made in the RDB Act have to be applied.”[8]

“The proceedings under the RDB Act 1993 cannot be stayed by the Company Court nor can they be transferred to the Company Court. No leave of the Company Court is necessary either for the filing of the OA for adjudication of the debt nor for executing the decree passed by the Tribunal. Section 34(1) gives overriding effect to the provisions of the Act save as provided in section 34(2).”[9]

Pegasus Assets Reconstruction P. Ltd. v. M/s. Haryana Concast Limited & Anr.,[10]

At page no. 25 of the judgement Apex court said

“For the purpose it has been enacted, it(SARFAESI Act 2002) is a complete code and the earlier judgments rendered in the context of SARFAESI Act 2002 or RDDBFI Act 1993 vis-à-vis the Companies Act, cannot be held applicable on all force to the SARFAESI Act. There is nothing lacking in the Act so as to borrow anything from the Companies Act till the stage the secured assets are sold by the secured creditors in accordance with the provisions in the SARFAESI Act and the Rules.”[11]

From above cases it is clear that before IBC 2016 came into picture Banks were empowered to enforce its security interest irrespective of what stage the winding up proceeding was.

(b) Position after commencement of IBC, 2016

After the advent of IBC 2016, it was made mandatory on the part of Adjudicating Authority (mentioned u/s 13(1)) once it admits application made u/s 7 or 9 or 10 of the code to:

“(a) declare a moratorium u/s 14;

(b) cause a public announcement of the initiation of CIRP and call for the submission of claims u/s 15; and

(c) appoint an insolvency resolution professional (hereinafter be referred as ‘IRP’) in the manner as laid down in section 16.”

And, as stated above the moment moratorium commences, Section 14(1) of the code prohibits under its clause (c) following:

“Any action to foreclose, recover, or enforce any security interest created by the corporate debtor in respect of its property including any action under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (54 of 2002);”

- Now here two situations arise:

- Creditors who have staked their claim in interim resolution professional

- Creditors who do not stake their claim to interim Resolution Professional in insolvency process.

(a.) Creditors who have staked their claim to interim resolution professional

Those creditors who stake and submit their claims to IRP[12] who then inspects their claims & if found true shall allow their claims. Once claims of all creditors are finalised committee of creditors (hereinafter to be referred as ‘CoC’) is constituted by IRP who then chooses Resolution Professional[13] who shall perform his duty on the directions and orders of CoC . Thereafter, resolution plan is finalised on the application of resolution applicant and is sent for the approval of Adjudicating Authority i.e. to National Company Law Tribunal (hereinafter be referred as ‘NCLT’). As provided by the proviso to section 14(4) the moratorium ends to operate from the time the Adjudicating Authority either approves the resolution plan or passes the order of liquidation.

Thus, now following four situations can be imagined where there might be conflict of IBC 2016 and SARFAESI Act 2016:

Situation 1: Application for initiation of corporate insolvency resolution process (CIRP) under section 7 or 8 or 9 or 10 of the IBC 2016 moved but not admitted: There will be no stay on SARFAESI Act 2002 proceedings.

Situation 2 : When NCLT admits of CIRP application: In accordance with section 14(1)(c) of the IBC 2016 there will be stay on proceedings under SARFAESI Act 2002 .

Situation 3 : Resolution plan ordered by Adjudicating Authority: In pursuance to Section 31(1) of the IBC, 2016, the parties are bound to comply and act in accordance with conditions of resolution plan.

Situation 4: Commencement of liquidation proceedings: As specifically stated by Proviso to Section 14(4) of IBC 2016 there will be no stay on enforcement of security interests.

In liquidation proceedings, as provided by section 52 (1) read with sub section (4) of the code provides secured creditors’ right to choose between

“(i) relinquishing rights on these assets to the liquidation trust and receiving the proceeds obtained from the liquidator’s sale of assets or (ii) enforcing / realising/ settling / compromising / dealing with their security interests and applying the proceeds to recover the debts due to it,.”

In case any secured creditor fails to recover its all debts through the sale proceeds of the encumbered properties, section 52 (9) of the IBC 2016 gives refuge to those creditors as well.[14]

Section 52(9) of the code states following:

“ Where the proceeds of the realisation of the secured assets are not adequate to repay debts owed to the secured creditor, the unpaid debts of such secured creditor shall be paid by the liquidator in the manner specified in clause (e) of sub-section (1) of section 53.”

Now, the question that would be pertinent to answer is that when two central acts contains non-obstante clause which act will prevail? Answer to this question can be best understood after taking stock of following observations of the Apex Court:

Maharashtra Tubes Ltd. v. State Industrial and Investment Corporation of India[15]

“ In the present case on a consideration of the relevant provisions of the two statutes it becomes clear that the State Finance Corporation Act 1951, deals with pre-sickness situation while the 1985 Act deals with post-sickness situation. It is, therefore, not possible to agree that the 1951 Act is a special statute vis-a-vis the Sick Industrial Companies (Special Provisions)Act 1985 Act. Both are special statutes dealing with different situations notwithstanding a slight overlap here and there, for example, both of them provide for grant of financial assistance though in different situations[16]. The Sick Industrial Companies (Special Provisions)Act,1985 being a subsequent enactment, the non-obstante clause therein would ordinarily prevail over the non-obstante clause found in Section 46 B of the State Finance Corporation Act 1951 unless it is found that the 1985 Act is a general statute and the 1951 Act is a special one. In that event the maxim generalia specialibus non-derogant would apply[17].”

From the observation of the Hon’ble Supreme Court made in 1993, it becomes clear that why moratorium u/s 14 (1) (c) of the IBC 2016 is able to prohibit enforcement of security interest under SARFAESI Act 2002, and the reason is that as sec. 238 of IBC 2016 is a provision of subsequent enactment it follows from the above observation of the Apex Court that by virtue of section 238 IBC 2018 will prevail over sec. 35 of SARFAESI Act 2002 although both being special statutes.

Thus, in view of Section 238 & aforementioned provisions of the IBC 2016 read with the above mentioned judgement of the Apex Court it can be safely said that provisions of IBC 2016 overrides SARFAESI Act 2002 in all four above mentioned situations.

(b.) Creditors who do not stake their claim to Interim Resolution Professional in insolvency process.

This also needs to be seen in two perspectives:

(i.) Creditors who have by mistake failed in staking and submitting their claim to insolvency resolution professional:

To such creditors regulation 12(2) of the CIRP (Corporate Insolvency Resolution Process) Regulations comes to their rescue, which states that:

“A creditor, who failed to submit proof of claim within the time stipulated in the public announcement, may submit such proof to the interim Resolution Professional or the resolution professional, as the case may be, till the approval of a resolution plan by the committee.”[18]

Thus, such creditors can stake their claim till the resolution plan is actually approved by CoC.

(ii.) Creditors who have not filed their claim (unintentionally or otherwise):

Section 31 (1) of the IBC states following:

“If the Adjudicating Authority is satisfied that the resolution plan as approved by the committee of creditors under sub-section (4) of section 30 meets the requirements as referred to in sub-section (2) of section 30, it shall by order approve the resolution plan which shall be binding on the corporate debtor and its employees, members, creditors, guarantors and other stakeholders involved in the resolution plan.”

Thus, this section appears to give a clue that resolution plan will be applicable on only those creditors who are involved in the resolution plan , hence it can be inferred that a creditor who has failed to submit its claim (unintentionally or otherwise) during the permissible period was not “involved” , and thus not bound by the resolution plan.

This point further substantiated by Article 300A of the Constitution which says,

“..No person shall be deprived of his property save by authority of law.”

In view of the aforementioned relevant statutory provisions, it appears that there is an ambiguity with respect to the status of claims of creditors who have not filed their claims as per the CIRP Regulations, and what remedy under the code is available to them apart from remedy available under SARFAESI Act 2002.

Cases Pending in different NCLTs against corporate debtors

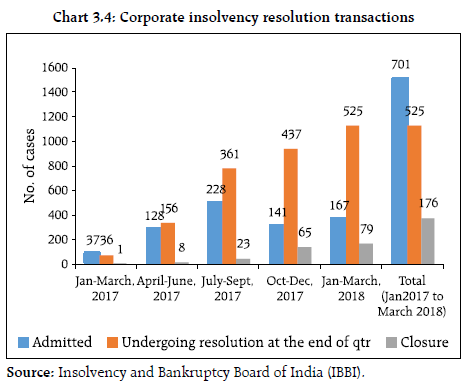

As of March 2018, 701 cases had been admitted for CIRP out of which 525 corporates were undergoing the resolution process in different NCLTs & out of 176 cases of closure 62 cases were closed on appeal or review[19] , which is manifest from the following chart published by RBI in June 2018 in its “Financial Stability report”.[20]

In para 3.25 of its report RBI states

“Of the 701 corporates admitted to the resolution process during January 2017 to March 2018,67 were closed on appeal or review, 22 resulted in a resolution and 87 yielded liquidations.”[21]

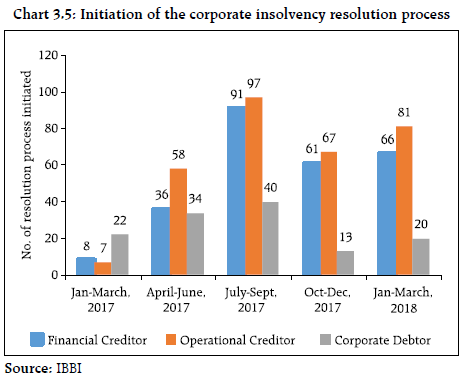

Chart 3.5 of its report, RBI also shows who have actually triggered initiation of the CIRP during January 2017 to March 2018.

From the data shown in the above chart, it is clear that out of 701 cases of CIRP initiated during Jan2017-March 2018, 129 cases of CIRP (18.40 %) were initiated by Corporates themselves & 262 cases of CIRP (37.37%) were initiated by Financial Creditors (which includes mainly Banks).

Table 4 -CIRP during January 2017-March 2018

(As mentioned in Financial Stability Report of RBI of June 2018)

|

Total No. Of cases admitted for CIRP |

701 |

|

No. Of cases undergoing resolution process |

525 (74.89%) |

|

No. Of cases initiated at the instance of Corporates |

129 (18.40%) |

|

No. Of cases initiated at the instance of Financial Creditor |

262 (37.37%) |

|

No. Of cases closed on appeal or review |

67 (9.55%) |

Judicial Decisions on whether moratorium u/s 14 of the code would prevail over SARFAESI Act 2002

Recently, the NCLTs have also passed some crucial orders to stop and dissuade any misuse of the provisions of the IBC 2016 so as to cause implementation of its provisions as per the letter and spirit of the Code.

Leo Duct Engineers and Consultants Ltd[22]

In the present case the corporate debtor “Leo Duct” had an outstanding liabilities of Rs. 32 crores towards Banks. Since, the Leo Duct was not in a position to discharge its liability, so, it made an application u/s 10 of IBC to initiate CIRP.As discussed above, the moment NCLT the admits of application u/s 10 of the IBC 2016 it has to declare moratorium (mentioned u/s 14 of the code ) u/s 13 of the code. Somehow Banks who had already initiated proceedings under SARFAESI Act 2002 got to know regarding moving of the application of CIRP by LeoDuct in the NCLT, therefore, they approached NCLT to dismiss application made by LeoDuct ,positing such move being a blatant abuse of law.

Problem before NCLT was whether to admit the application for the initiation of CIRP which would cause commencement of moratorium and thus would preclude Financial Creditors from recovering their debts under SARFAESI Act 2002.[23]

The NCLT stated that though SARFAESI Act 2002 permits Banks to proceed against any security be it of Corporate Debtor or Personal Guarantor yet the moment moratorium u/s 14 of the IBC 2016 commences it stalls all proceedings both against Corporate Debtor and Personal Guarantor. Thus, there is a fair possibility that Corporate Debtor or Personal Guarantor may use moratorium under IBC 2016 to stall proceedings under SARFASEI Act 2002.[24]

Noting this, the NCLT held that since the Banks had already set the wheels in motion to recover their debts against LeoDuct , Leo Duct was just using application u/s 10 of the IBC 2016 as a dilatory tactic to stall Bank’s proceedings under the SARFAESI Act which was quite evidently frustrate process of law. Accordingly, the application of Leo Duct was dismissed.[25]

Unigreen Global Private Limited vs Punjab National Bank and Ors [26]

In the present case, Unigreen Global Pvt. Ltd. (“Unigreen“)which was corporate debtor made an application in NCLT to initiate CIRP as it was unable to discharge its outstandinf liabilities of Rs 100 Crores.The Creditor Bank argued that the Unigreen with the aim to delay the payment had already initiated several civil suits and had also preferred appeal u/s 17 of the SARFAESI Act 2002 .The issue was whether the CIRP application could validly be admitted.

The NCLT after verifying all documents presented by Banks observed that admission of the CIRP application would invoke the application of moratorium scuttling all legal proceedings thus, it would unjustly restrain bank from exercising security interest under SARFAESI Act 2002 over the securities. Thus, the NCLT not only dismissed Unigreen’s application but also imposed a penalty of Rs. 10,00,000/- on Unigreen and its directors u/s 65 of the IBC 2016.[27]

Schweitzer Systemtek India Private Limited vs Pheonix ARC Pvt. Ltd. & Ors [28]

Brief facts of this case is same as facts of the above two cases as it was alleged by Financial Creditors that Schweitzer Systemtek India Private Limited (“SSI”) which was the corporate debtor in this case had with the aim to scuttle the proceedings of SARFAESI Act 2002 moved application u/s 10 of the IBC.

The tribunal took stock of Section 14 (1)(c) which states that a moratorium is to be declared to “prohibit any action to recover or enforce any security interest created by the Corporate Debtor in respect of its property“. Here, NCLT noted that because the word “its” has been used the moratorium declared u/s13 read with section 14 would only restrict proceedings against properties of corporate debtor and proceedings against personal guarantor were not restricted by section 13 read with section 14. The Application was therefore admitted, subject to this exception.

In the above cases, situation in which there might be a direct conflict between the two above named statutes did not arise as Adjudicating Authorities smelled rat before admitting application of the defaulting corporate debtor or admitted, subject to some exceptions.

But, in the case of Sanjeev Shriya vs State Bank of India & Ors[29] where the facts in brief were following:

In 2005 directors of the Company X entered and executed the deed of guarantee in favour of the bank .Two years later company was declared as a sick company under Sick Industrial Companies Act 1985 (“SICA”).In 2017 banks made application u/s 19(3) of the RDDBFI Act 1993 in the DRT for the recovery of due money against the principal debtor i.e. the company. Few days later the DRT admitted the application and also passed an interim order enjoining the personal guarantors i.e. directors to disclose particulars of their assets as specified by Bank in the application.

With the aim to bypass this order of the DRT, Company made an application u/s 10 of the IBC 2016 to initiate CIRP. Subsequently, NCLT admitted the application and declared moratorium. Then, the Company used this order of NCLT to get stay on the proceeding before DRT and contended that vide this order of the NCLT all proceedings against guarantors before DRT should also be stayed. But, DRT though stayed the proceedings against company denied staying of the proceedings against the guarantors. Thus, an appeal was filed before Allahabad High Court where High Court held that, moratorium u/s 14 of the code is also applicable on the personal guarantors.

Thus, it was seen that when there was actual tussle between the provisions of SARFAESI Act 2002 and IBC 2016, later prevailed over former.

The above matter i.e. whether IBC 2016 overrides any other act/statute is now seems to be settled by judgements of following two Supreme Court cases :

(i) M/s Innovative Industries Ltd. vs ICICI Bank & Anr.[30]

In this case a multi product company owing to suffering of losses and its inability to pay back for the financial assistance given to it by 19 banking entities itself proposed for corporate debt restructuring(“CDR”). These 19 banking entities formed a consortium and approved the CDR by approving the restructuring plan which was to be implementable over a period of 2 years and later based on this restructuring plan also entered a master restructuring agreement(“MRA”) as per which funds were to be infused by the creditors. Few months after ICICI Bank one of the 19 banking entities made an application in NCLT stating the company being a defaulter under the code i.e. IBC 2016 , the insolvency resolution process[31] should be set in; Controverting this the company replied that they are not legally obliged to pay any amount based on two notifications passed under Maharashtra Relief Undertakings (Special Provisions Act), 1958 (hereinafter referred to as the “Maharashtra Act”), and later filed one more application taking the plea that since no fund was released to it by the bank, it failed to pay the debt instalment on time and also controverted that since it paid some amounts to five banks it fulfilled its liability under MRA; thus the company committed no default.

Upon above facts NCLT held that IBC 2016 being a central statute would prevail over Maharashtra Act which was a state statute by virtue of non -obstante clause of section 238 of the code and found that company had defaulted in making payments.

Against this decision company filed an appeal in NCLAT which too met the same fate. Ultimately, appeal was filed in Supreme Court where counsel of the company argued since Maharashtra Act operated in the different field than IBC 2016 and there was no real inconsistency therefore provisions of the Maharashtra Act should be applied in present set of facts; on this, counsel of the ICICI bank riposted that since Maharashtra Act imposed moratorium against all legal proceedings, it was in this regard a real & direct conflict and this inconsistency of Maharashtra Act was not some theoretical inconsistency with section 14 of the code (as Supreme Court had applied the Principal of Occupied Field to reach onto this conclusion) . Further he also argued that by dint sec. 238 of the code provisions of IBC 2016 should prevail over Maharashtra Act.

Eventually, Supreme Court acceded to the prayer of ICICI Bank, and also countenanced the reasoning given by its counsel but, quite emphatically took stock of one particular clause of the MRA and held that as per that clause obligation on the part of the company was unconditional and did not depend upon the infusing of funds by the creditors. And , therefore held company to liable for default in payment.

From the observation of the Apex Court, it can inferred that Apex Court throughout its judgement maintained the position that IBC 2016 would prevail upon any other statue but still in the final reasoning Apex Court eventually based its decision on the clauses of the MRA which then causes some iota of confusion to persist as Apex Court failed to clarify the question ‘what if the obligation would have been conditional and depended on the infusing of funds by the creditors, is it then too IBC 2016 would have applied’ which was clarified by the Apex Court in following case:

(ii) PR. Commissioner of Income Tax vs Monnet Ispat & Energy ltd.[32]

In this case Supreme Court in quite clear terms observed that “given sec. 238 of the IBC 2016 it is obvious that the Code will override anything inconsistent contained in any other enactment, including Income Tax Act.”

This case made it very clear that in case of any inconsistency of any statute ( be it state or central ) with IBC 2016, IBC 2016 will prevail.

Judicial Decisions on applicability of Moratorium u/s 14 of the code over ‘Personal Guarantor’

Section 13(11) of the SARFAESI Act 2002 reads as:

“ Without prejudice to the rights conferred on the secured creditor under or by this section, secured creditor shall be entitled to proceed against the guarantors or sell the pledged assets without first taking any of the measured specifies in clause (a) to (d) of sub- section (4) in relation to the secured assets under this Act.”

Thus, the question arose whether after commencement of moratorium u/s 14 of the code could banks enforce security interest against guarantors as provided u/s 13(11) of the SARFAESI Act 2002 or sec 14 of the code even prohibits such enforcement?

This confusion was further augmented by contrary views taken by Allahabad High Court in the case of Sanjeev Shriya vs State Bank of India & Ors and NCLAT, New Delhi in the case of Alpha & Omega Diagnostics (India) Ltd. vs Asset Reconstruction Company of India Limited & Ors[33] . Allahabad High Court in the case Sanjeev Shriya vs State Bank of India & Ors. held that moratorium u/s 14 of the IBC 2016 is also applicable on personal guarantors ; whereas NCLAT, New Delhi in the case of Alpha & Omega Diagnostics (India) Ltd. vs Asset Reconstruction Company of India Limited & Ors[34] dismissing the petition filed against the decision of NCLT Mumbai Bench countenanced NCLT’s observation in which tribunal had observed following:

“The property not owned by the Corporate Debtor do not fall within the ambits of the Moratorium (para 7)” and “Before I past with it is necessary to clarify my humble view that the SARFAESI Act may come within the ambits of Moratorium if an action is to foreclose or to recover or to create any interest in respect of the property belonged to or owned by a Corporate Debtor, otherwise not (para 8).”[35]

Then, in March 2018 “Report of the Insolvency Committee” was published in which committee on para 5.11 of its report stated following:

“The Committee concluded that section 14 does not intend to bar actions against assets of guarantors to the debts of the corporate debtor and recommended that an explanation to clarify this may be inserted in section 14 of the Code. The scope of the moratorium may be restricted to the assets of the corporate debtor only.”

Finally, this matter came before the scrutiny of the Apex Court in the case of State Bank of India vs V.Ramakrishnan & Anr.[36] In the judgement given on 14th August 2018, Apex Court differentiated between moratorium mentioned u/s 14 of the code and interim moratorium and moratorium mentioned under sec 96 &101 respectively (under part III) of the IBC 2016 and made following observation

“We are also of the opinion that Sections 96 and 101, when contrasted with Section 14, would show that Section 14 cannot possibly apply to a personal guarantor. When an application is filed under Part III, an interim-moratorium or a moratorium is applicable in respect of any debt due……….. The object of the Code is not to allow such guarantors to escape from an independent and coextensive liability to pay off the entire outstanding debt, which is why Section 14 is not applied to them.”

(Apex Court also stated that since this clause is clarificatory so it will apply retrospectively as Hon’ble Supreme Court posited that clarificatory amendments are retrospective in nature.)

To obviate the above confusion and to clarify other matters parliament in observance of recommendations posited by Insolvency Committee in its March 2018 “Report of the Insolvency Committee” passed IBC (Second Amendment) 2018. Under its section 10 of the 2018 act, amendment was made to section 14(3) of the code which states following:

“The provisions of sub-section (1) shall not apply to-

(b) a surety in a contract of guarantee to a corporate debtor.”

Conclusion

From the above discussion, one thing that becomes crystal clear that once moratorium u/s 14 of the IBC 2016 commences banks cannot enforce its security interest against debtor under chapter –III of SARFAESI Act 2002 , but, as discussed in State Bank of India vs V.Ramakrishnan & Anr[37] banks can enforce its security interest against personal guarantor as provided u/s 13(11) of the SARFAESI Act 2002. Furthermore, by the observation of the cases like Leo Duct Engineers and Consultants Ltd., Unigreen Global Private Limited vs Punjab National Bank and Ors & Schweitzer Systemtek India Private Limited vs Pheonix ARC Pvt. Ltd. & Ors the problem that floats up is that company may use section 14 of IBC 2016 as a bulwark to protect itself against different proceedings which could be commenced by a bank to enforce its security interest against debtor (company) with no motive of corporate restructuring (and this problem is not an academic problem as of all cases admitted for CIRP between Jan 2017-Mar 2018, 18.40% were admitted at the instance of Corporate) , therefore, such technology must be developed in which record (esp. registry) of DRTs/DRATs and NCLTs are so integrated that NCLTs before admitting the application u/s 10 could confirm whether there is/are any pending proceeding/s under DRTs/DRAT so that it may work with DRTs/DRAT in a complimentary manner to relieve banks from the burden of bad debts as expeditiously as possible and this will also save precious time of tribunals from being wasted due to exploitation by cunning debtors owing to lack of effective co-ordination among different tribunals.

Endnotes

[1] SLP No. 6481 of 2018

[2] Civil Appeal No. 3595 of 2018

[3] Defined under section 2(o) of the SARFAESI Act 2002

[4] 5 charts that show why cabinet cleared ordinance to solve NPA issue ,Live Mint (Oct 2,2018), https://www.livemint.com/Industry/sDSiJqVcl8AcqwLBQ02KIJ/5-charts-that-show-why-cabinet-cleared-ordinance-to-solve-NP.html

[5] Section 12 of Insolvency Bankruptcy Code 2016

[6] Defined u/s 5(1) of the Insolvency Bankruptcy Code 2016

[7]AIR 2000 SC 1535

[8] Supreme Court of India (Aug 11,2018, 2:20 PM), https://www.sci.gov.in/jonew/judis/16439.pdf

[9] Ibid.

[10]Civil Appeal No. 3646 of 2011

[11]Supreme Court of India (Sept 19, 2018,10:40 AM) , https://www.sci.gov.in/jonew/judis/43212.pdf

[12] Defined u/s 2 (19) of Insolvency Bankruptcy Code 2016.

[13] Defined u/s 5 (27) of Insolvency Bankruptcy Code 2016.

[14] Insolvency and Bankruptcy Code and Bank Recapitalisation, Reserve Bank of India ( Sept 10,2018, 3:30 PM), https://www.rbi.org.in/scripts/PublicationsView.aspx?id=18060

[15] 1993(2) SCC 144

[16] Maharashtra Tubes Ltd. Vs. State Industrial and Investment Corporation of Maharashtra Ltd. and anr. – Court Judgment, Legal Crystal ( Sept 29, 2018, 3:30 PM), https://www.legalcrystal.com/case/657749/maharashtra-tubes-ltd-vs-investment-corporation

[17] Ibid.

[18] Interim Resolution Professional , ICSI( Sept 29, 2018, 3:30 PM), http://icsiipa.com/Portals/0/docs/Interim-Resolution-Professional-%20A-Handbook.pdf

[19] Financial Stability Report Issue No. 17 by Reserve Bank of India (published in June 2018)-available at page 62 para 3.25

[20] Ibid., para 3.23

[21] Ibid, Para 3.25

[22] 1103/I&BP/NCLT/MAH/2017

[23]NCLT, COURTS AND THE RBI WORK TOGETHER TO IMPLEMENT THE BANKRUPTCY CODE, Nishith Desai (Sept 23,2018,3:30 PM) , http://www.nishithdesai.com/information/news-storage/news-details/article/dispute.html

[24] Ibid

[25] Ibid.

[26] C.P NO. (IB)-39(PB)/2017.

[27] Ibid

[28] NCLAT, New Delhi, Company Appeal (AT) (Insolvency) No. 129/2017, Date of decision – 09 August, 2017.

[29] (MANU/UP/2243/2017)

[30] Civil Appeal No. 8337-8338 of 2017

[31] As mentioned under chapter II of the Insolvency Bankruptcy Code 2016.

[32] SLP No. 6481 of 2018

[33] NCLAT, New Delhi, Company Appeal (AT) (Insolvency) No. 116/2017, Date of decision – 31 July, 2017.

[34] Ibid

[35] Dignostics India Ltd Vs Asset Reconstruction Company of India Ltd Ors ,Insolvency and Bankruptcy Board of India (Oct 2,2018, 4:50 PM),

http://www.ibbi.gov.in/DignosticsIndiaLtdVsAssetReconstructionCompanyofIndiaLtdOrsCompanyAppealATInsolNo116of2017.pdf

[36] Civil Appeal No. 3595 of 2018

[37] Civil Appeal No. 3595 of 2018

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications