This article is written by Keshav Bhardwaj, pursuing a Diploma in Companies Act, Corporate Governance and SEBI Regulations from Lawsikho.com.

Table of Contents

Introduction

The Valuer is an individual/ an entity performing the act of valuation. What is meant from Value and Valuation? Value is the monetary worth of something (e.g. market rate), reasonable return/ exchange to something equivalent (e.g. property, goods or services), or something of relative utility. Valuation is the systematic method for determining the worth of any asset or liability at present time keeping in mind the valuation standards. The Registered Valuer means a body that is registered with the Authority in indication to the Companies (Registered Valuers and Valuation) Rules, 2017. An applicant has been a member of the Registered Valuer Organisation before seeking registration as a registered valuer under IBBI. There may be such situations where the valuation is required. For example, the valuation of shares for a merger has a distinct value than financial reporting as the regulatory standard may vary in terms of ways to arrive at a balanced value. The fair value of shares has different meanings for different purposes like a fair value in terms of legal, financial reporting, or market value, etc. Such valuation must be determined by the Registered Valuer.

There are three types of registered valuer:

- Land & Building Valuer.

- Plant & Machinery Valuer.

- Securities or Financial Assets Valuer.

Now Let’s understand how the concept of Registered Valuer was introduced in the Companies act, 2013, and related rules.

The Registered Valuer was firstly introduced in India by the Companies Act, 2013, although the “Valuer” is not a new concept, it was in existence earlier. However, there wasn’t any specific body to regulate it. The first attempt was made by introducing the Valuation Professional Bill, 2008. The same has been delayed for many years due to the dissolution of parliament. Thereafter, The Central Government of India introduced the Companies (Removal of Difficulties) Second Order, 2017 (dated 23rd October 2017) to conduct valuation which required to be performed by the person possessing the essential requirements, skill and working as a valuer need to register with the authority, the same date Central Government bestowed its powers and duties to the Insolvency and Bankruptcy Board of India (IBBI) under Section 247 of the Companies Act, 2013, also assigned IBBI as Authority under the Companies (Registered Valuers and Valuation) Rules, 2017.

Consequently, It’s required that only the person who has registered with the IBBI can conduct the valuation as per the Companies Act, 2013 with effect from 1st February 2019. The person providing valuation services can do so continuously without the requirement of any Registration Certificate only up to the 31st January 2019 as per the Insolvency and Bankruptcy Code. Till this date (13 September 2020), 3321 individuals and 26 Registered Valuer Entities have registered themselves with IBBI under three asset classes (For live status click here). Before coming to the eligibility and qualifications, Let us first understand why there is a requirement of the registered valuer with laws and regulations related to registered valuers.

Functions of valuers

A valuer shall perform the valuation under the Act as per the Companies (Registered Valuers and Valuation) Rules, 2017. The same rules applied just in case valuation is required under any other law or authorities related to it.

The registered valuer can perform the valuation under the following Acts or Regulations:

- Companies Act, 2013.

- Insolvency and Bankruptcy Code, 2016.

- SEBI [Real Estate Investment Trusts (REIT) Regulations, 2014 & Infrastructure Investment Trusts (InvIT)] Regulations, 2014.

Various laws and regulations you need to know about registered valuer

The Registered Valuer needs to abide by the different kinds of rules and regulations governing Registered Valuer. The Ministry of Corporate Affairs, Insolvency & Bankruptcy Board of India, and Stock Exchange Board of India making contributions in legislative affairs for Registered Valuer. These are the following steps taken by these bodies:

Companies Act, 2013: Firstly, Section 247 of the Companies Act, 2013 defines the basis of the valuer as follows:

Section 247 (1) mentions that if the valuation required to make regarding:

- Any property, shares, securities, stock, debentures, goodwill, or any other asset; or

- Net-Worth; or

- Liabilities

of the Company, the person must satisfy the required eligibility and experience, also to register with the assigned authority. Then, the person can be designated as Registered Valuer by the Audit Committee or in its absence appointed by the Board of Directors of the Company.

Insolvency and Bankruptcy Board of India(IBBI) via Circular dated 16th September 2019 provided a list of provisions from the Company Act, 2013 and Insolvency and Bankruptcy Board of India 2016 under which the valuation from Register Valuer is mandatory.

Provisions where the valuation mandated from the Registered Valuer (Companies act, 2013 and Companies Rules)

|

S No. |

Sections of the Companies Act, 2013

|

Particulars |

|

1 |

Section 62(1)(c) read along with Rule 13(1) under Companies (Share Capital and Debentures) Rules, 2014. |

Further issue of share for increasing its subscribed capital. |

|

2 |

Section 177(4)(vi) |

Valuation of asset or undertaking of as per the term of reference defined by the Audit Committee. |

|

3 |

Section 192(1) and 192(2) |

Restriction on every non-monetary transactions where directors are involved. |

|

4 |

Section 230(2)(c)(v) and Section 230(3) |

Power to negotiate or make settlements with creditors and members of the company. |

|

5 |

Section 232 (2)(d) and Section 232 (3)(h)(B) |

A valuation report by the expert regarding the Merger and amalgamation of companies. |

|

6 |

Section 236(2) |

Buying minority shareholding (Price to be determined based on valuation). |

|

7 |

Section 247(1) |

Valuation by Registered Valuers fulfilling all requirements given under this Act and Companies Rules (Registered Valuers and Valuation) Rules, 2017. |

|

8 |

Section 281(1)(a) |

Report Submission by Company Liquidator (along with the nature of the Asset or Property and Valuation of price the Asset. |

|

9. |

Section 305 (2) |

Valuation of the assets while proclaiming solvency in case of voluntary winding up. |

|

S No. |

Companies Rules |

Particulars |

|

1 |

Rule 2(c)(ix) – Companies (Acceptance of Deposit) Rules, 2014 |

Separation from deposits. (if the deposits which are taken by the charge on the Assets or Properties mentioned in Schedule III of Companies Act, 2013 excluding intangible assets, the value of before-mentioned deposits and the interest due shall not surpass the market price of before-mentioned assets as evaluated by Registered Valuer). |

|

2 |

Rule 6 Sub-rule 1 – Companies (Acceptance of Deposit) Rules, 2014 |

Creation of security (same as mentioned within the brackets above). |

|

3 |

Rule 8(6), (7), (9) and (12) – Companies (Share Capital and Debentures) Rules, 2014 |

Issuance of sweat equity shares (shall be priced at value ascertained by the registered valuer). |

|

4 |

Rule 16(1)(c) – Companies (Share Capital and Debentures) Rules, 2014 |

Provision of capital by the company for the buying of own shares by workers or by trustees, for the interest of employees (where the shares are not listed on the recognized stock exchange in such case price to be determined by Registered Valuer). |

|

5 |

Rule 12(5) – Companies (Prospectus and Allotment of Securities) Rules, 2014 |

Return of allotment (Valuation Report of Consideration to be attached with the Contract). |

Provisions of the Insolvency and Bankruptcy Code, 2016 and the regulations

|

S. No |

Section/Regulation/ Rules |

Particulars |

|

1 |

Section 59(3)(b)(ii) – Insolvency and Bankruptcy Code, 2016 |

Voluntary liquidation of corporate bodies (Asset Valuation Report). |

|

2 |

Section 46(2) – Insolvency and Bankruptcy Code, 2016 |

The appropriate duration for avoidable transactions (Independent Expert for assessing the evidential value if the transaction. |

|

3 |

Regulation 27 read with regulation 35 of the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 |

(The Resolution Professional appoints a Registered Valuer within a week of his appointment). |

|

4 |

Regulation 35 – IBBI (Liquidation Process) Regulations, 2016 |

Valuation of assets intended to be sold (the registered valuer calculates the realizable value of Asset or Property). |

|

5 |

Regulation 3(1)(b)(ii) – IBBI (Voluntary Liquidation Process) Regulations, 2017 |

Initiation of liquidation (a Valuation report of Asset or Property, if there any). |

|

6 |

Regulation 26 under IBBI (Fast Track Insolvency Resolution Process for Corporate Persons) Regulations, 2017 |

Appointment of registered valuer (Provide that the person shall not be appointed as the registered valuer in some circumstances). |

|

7 |

Regulation 34 – IBBI (Fast Track Insolvency Resolution Process for Corporate Persons) Regulations, 2017 |

Fair value and liquidation value (After the physical education makes an estimation based on international standard). |

Provisions of the SEBI Real Estate Investment Trusts (REIT) Regulations, 2014 & SEBI Infrastructure Investment Trusts (InvIT) Regulations, 2014:

The “Valuer” means any individual who is considered as “registered valuer” under Section 247 of the Companies Act, 2013, and the person elected by the manager for valuation of the Real Estate Investment Trust (REIT) assets & Infrastructure Investment Trusts (InvIT) assets.

After understanding the sections and rules related to the registered valuer this now let’s come to understand the steps required to become a registered valuer.

How to become a Registered Valuer

Every person whether it’s an individual or corporate entity (Limited Liability Partnership, Company, and the partnership firm) seeking to become a registered valuer require to follow the steps given under:

Most of the steps covered are common for an individual as well as the corporate entity. However, there are some aspects, which are different in the case of the corporate entity (which are stated in underlined-Italic font form).

Step 1: Qualification & Experience requirement

According to rule 4 along with Annexure-IV of the Companies (Registered Valuers and Valuation) Rules, 2017, a person required the following qualification and experience for enrolling as a registered valuer:

In Brief:

- Graduation Degree with 5 years of experience post-qualification.

- Post Graduation Degree with 3 years of Experience post-qualification.

- Enrolled as a member in any Professional Institute with 3 years of post-qualification experience.

In detail, qualification and experience required is hereunder:

|

Asset Class |

Qualifications |

Experience Required |

|

1. Graduation Degree In discipline from Mechanical, Electrical, Electronics and Communication, Electronics and Instrumentation, Production, Chemical, Textiles, Leather, Metallurgy, or Aeronautical Engineering, or Valuation of Plant and Machinery or equivalent. |

5 Years |

|

|

2. Post-Graduation of aforementioned degrees. |

3 Years |

|

|

Land and Building |

1. Graduation Degree in Civil Engineering, Architecture, or Town Planning or equivalent. |

5 Years |

|

2. Post-Qualification of aforementioned degrees & Real Estate or Building Valuation / Valuation of Land (2 Years Course). |

3 Years |

|

|

Securities or Financial Assets |

1. Membership of Institute of Chartered Accountants of India, Institute of Company Secretaries of India, Institute of Cost Accountants of India, Master of Business Administration Management or Post-Graduate Diploma in Business Management with specialization in the finance subject. |

3 Years |

|

2. Post Graduation Degree in the Finance subject. |

Note: Any other asset class corresponding to the qualification and experience mentioned above regarding rule 4 as may be defined by the Central Government.

Other Eligibilities as given under rule 3 are as follows that he/she:

- is not a Minor;

- hasn’t been declared unsound mind;

- is not undercharged insolvent or applied to adjudicated as insolvent;

- must be a resident of India;

The ‘person resident in India’ shall have the same meaning as mentioned in Section 2 (v) of Foreign Exchange Management Act, 1999 in case of an individual;

- hasn’t been sentenced for more than 6 months of imprisonment by any competent court or for moral turpitude offense & 5 years not completed from the date of expiry of such sentence;

Subject to given provision if the individual has been convicted for seven years or more, he shall not be competent to register;

- hasn’t been levied penalty given in Section 271(J) of the Income Tax Act, 1961, and the period for appealing in front of the Commissioner of Income-Tax Appellate Tribunal get expired or after confirmation, five years not complete from the date of levy of such penalty;

- is the fit and proper person, but that must scope not be limited to the following:

- Integrity, reputation, and character;

- Any kind of Convictions it restraint orders must not be present; and

- Competence and Financial Solvency.

Step 2: Enrolled in a Registered Valuer Organisation (RVO)

The Registered Valuer Organisation (RVO) is an institution that is acknowledged under rule 13 sub-rule 5 of the Companies (Registered Valuers and Valuation) Rules, 2017. Everyone firstly requires being a member of the RVO recognized by the IBBI, before seeking registration as the registered section. For accessing the list of (Asset Class-wise) registered with the IBBI along with the Website & Contact Details- Click here.

Step 3: Educational course (50 Hours)

After getting enrolled with the RVO, the person is required to finish the educational course (50 Hours) recognized by the IBBI.

The syllabus, format & frequency of the valuation exam comprising qualifying marks shall be acknowledged on the IBBI website before 3 months of the examination. There is no limit on the number of attempts for the valuation examination. After passing, acknowledgment is provided to the individual who has passed the valuation examination.

Step 4: Syllabus and Study Material of Valuation exam

Enroll and clear the computer-based Valuation Examination (with effect from 1st of June, 2020) of the chosen Asset Class administered by the IBBI. To access the syllabus and study material of the examination click on the links given below (Asset-Class wise):

|

S. No |

Asset Class |

Syllabus |

Study Material |

|

1. |

Land and Building |

https://ibbi.gov.in/uploads/resources/CVSRTA-Land_and_Building.pdf |

|

|

2. |

Plant and Machinery |

https://ibbi.gov.in/uploads/resources/CVSRTA-_Plant_and_Machinery_final.pdf |

|

|

3. |

Securities and Financial Asset |

https://ibbi.gov.in/uploads/resources/Securities_or_Financial_Assets.pdf |

Afterwards, the person can apply for registration within the preceding 3 years from the date of making the application.

Step 5: Submission of Form

After passing the valuation exam the person is required to fill and submit Form-A in case of an Individual (Step by Step procedure- how to fill Form-A) & Form-B for Corporate Entities (Step by Step procedure- How to fill Form-B) in case of corporate entity and upload the necessary documentary confirmations on the IBBI website and send the same to the RVO with whom the person is enrolled for approval. After inspection of the form, the Payment link is made available on that person’s email address.

Step 6: Application Fees payment

The person has to pay the fees ₹ 5,900 (₹ 5,000 + 18% GST) & for Corporate Entities ₹ 11,800 (₹ 10,000 + 18% GST) using the payment link from the Email. The payment link will be sent only after getting the approval on application from RVO. After that, take a print copy of the Payment Page for further use in the future.

Step 7: Submit the following documents to the RVO form

- Form-A Document in the signed form addendum to Form-A (Individual) & Form-B Document in the signed form addendum to Form-B (Corporate Entities);

- Documentary confirmations copies uploaded before;

- Print copy of Payment as (quote GST number if required) as mentioned in step 6.

Step 8: After receiving these documents RVO shall

- Shall verify the credibility of the documents (as mentioned in Step 7);

- Make sure that documents uploaded on the portal or not;

- Also, to inform the applicant, if anything is remaining.

Source: https://ibbi.gov.in/uploads/rules.pdf

Thereafter, send the scanned copy of the documents to the applicant for uploading on the portal. Scanned copy documents include the documents mentioned in Step 7.

Step 9: After receiving the Scanned documents

After receiving the scanned documents, the same shall be uploaded on the portal by the Applicant and then click on submit for completion of registration of Application.

Thereafter, RVO has to approve the online application and send documents in physical form to the IBBI.

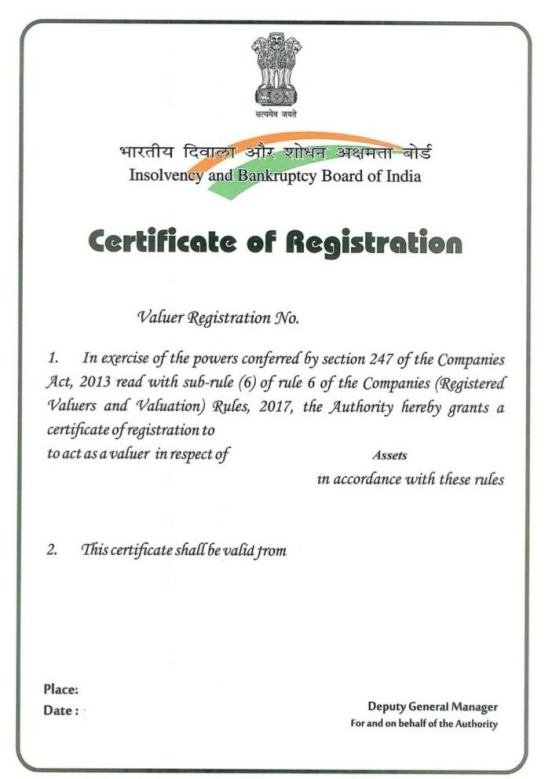

Step 10: Certificate of Practice

After the registration is granted by the IBBI, the applicant has to receive the Certificate of Practice from the related RVO before starting the practice.

Source:- http://www.rajvanshica.in/ibbi-registered-valuers.html

Cancellation & suspension of certificate of registration

The Insolvency and Bankruptcy Board of India (IBBI) may cancel or suspend the certificate of registration of the valuer the following circumstances:

- Public Interest; or

- Violation of any provision of Companies Act, 2013 & Insolvency and Bankruptcy Board of India, 2016 to related rules or any condition specified.

Thereafter the officer appointed by IBBI can conduct the inspection and send the Show Cause Notice to that person and thereafter the person has to prove himself by adhering with the principles of Natural Justice. The Authority can warn him instead of cancellation or suspension. The order will come into effect after 30 days of passing order, it can be appealed before IBBI. For additional information regarding Cancellation & Suspension- Click Here.

Punishment

Punishment for Contravention: Without implying an admission of liability, where the person contravenes any sections of the Act or the rules will be punishable under Section 247(3) of the Companies Act, 2013. The person will be charged with the fine ₹ 25,000 (Twenty Five Thousand Rupees) which may extend up to ₹ 1,00,000 (One Lakh Rupees).

Subject to this provision, if it’s with intent to deceive the company or its members then the person will be imprisoned for the term up to 1 year with the fine which shall not be less than ₹ 1,00,000 (One Lakh Rupees) which may extend up to ₹ 5,00,000 (Five Lakh Rupees).

Punishment for false statement: If any report, certificate, or other documents for the purpose or need of the Act or regulation, any individual make the declaration, which:

- Prove to be false in the material form, acknowledging it to be false.

- Material fact, acknowledging as material, will be held liable under Section 448 of the Companies Act, 2013.

What are some key changes proposed under the Draft Valuers Bill, 2020 regarding valuers?

Mr. Injeti Srinivas, Secretary, Ministry of Corporate Affairs, firstly understand the requirement of the institutional framework for the Valuation Professional noting the growth since the enactment of Valuer Rules, a Committee of Experts (CoE) was set up by the Government of India (GoI) to inspect upon the need of a framework for the growth of Valuation Professionals.

Here some of the key changes recommended under the report by COE to GOI, which thereafter represented as Draft Valuers Bill, 2020 (Dated 25h of April 2020):

- To constitute National Institute Of Valuers (NIV) consist of the Chairman of eight members as representative or elected members of Regulatory Bodies (Ministry of Corporate Affairs, Ministry of Finance, Reserve Bank of India, Securities and Exchange Board of India, Insolvency and Bankruptcy Board of India and three whole-time members Including one for Administrative Law Member. Also, Bill proposed the 3-tier method for regulators.

- NIV will acknowledge the Universities/ Institutions/Valuer Professional Institute after checking their credentials. Also to formulate the prescribed norms for courses providing excellence and keep monitoring the performance.

- Also, the scope valuation must not be limited only to the Companies Act, 2013, and the Insolvency and Bankruptcy Code, 2016, it will cover every area where the valuation is required. The NIV takes due care of action for recognition of valuation by Valuers.

- Registered Valuer name changed to Valuer and the Registered Valuation Organisation name changed to the Valuation Professional Organisation (Same applies to the existing Registered Valuers and Registered Valuation Organisation).

- There are four paths way recognized for becoming a valuer out of which two are temporary and two are permanent;

|

Graduate Valuation Programme |

National Valuation Programme (Relevant Asset Class) |

Limited Valuation Program |

50 Hours Training Programme from Registered Valuer Organisation |

|

|

Eligibility |

Any degree or equivalent qualification in the specified mode |

Senior Secondary Education |

Pass the Valuation Exam with experience as mentioned under |

Chartered Accountant, Company Secretary, Cost & Management Accountancy, Bachelor of Engineering, Bachelor of Technology, Post Graduation in the Valuation, Post Graduation Diploma in Business Management |

|

Experience |

Not necessary |

Not necessary |

Minimum of 5 years |

Chartered Accountant, Company Secretary, Cost and Management Accountancy, Master of Engineering, Master of Technology, Post Graduation in the Valuation: 3 Years Graduate: 5 Years |

|

Sunset clause for the eligibility |

Not Applicable |

Not Applicable |

2 years from the date of commencement of this provision |

3 years from the date of commencement of this provision |

The present method for becoming values automatically gets stopped after 3 years of implementation of this provision. Though, the person practicing the valuation services for more than 5 years required to clear the valuation exam and to enroll in the limited valuation program within 2 years from the date of implementation of this provision.

- Corporate entities including Partnership firm, Limited Liability Partnership or Company, except the joint ventures, association or subsidiary registered as registered.

- In the case of an entity, one of its partners or directors (as the condition may be) is a valuer of such asset class for which the company is applying by registration. The Partner/Directors who are valuers will be liable jointly and severally for any act or omission of the Entity, regarding valuation.

- The Valuer can’t hold the Certificate of Practice if he/she is working or employed anywhere. However, the person may continue the existing profession while working as a valuer.

- Valuers Professional Organisation (VPO), which is presently known as

Registered Valuer Organisation must formulate the bye-laws for members, professional growth, keep a check on activities on conduct education programs. - The Central Government of India will announce the Valuation Standard in discussion with the regulatory bodies such as the Ministry of Corporate Affairs, Ministry of Finance, Reserve Bank of India, Securities and Exchange Board of India, Insolvency and Bankruptcy Board of India, and other bodies.

Conclusion

The Ministry of Corporate Affairs has presented the much-awaited Valuation Rules. The Valuation Rules covered almost all of the concerning areas related to valuers and valuation. It’s an effort to ensure the fair & true valuation and to bring standardization. The transparency and fairness behavior among the valuer will lead to confidence among the stakeholders. The drafting panel’s expectation to grow valuation on par with professions like medication and advocacy will require some amount of time, yet the general uniform structure serves a worthwhile end.

Frequently asked questions

- What is meant from the word “Specified Discipline”?

It means the specified discipline required for the valuation of the asset for which registration is sought.

- What is meant from the word “equivalent” in terms of educational qualification?

It meant for the professional and technical qualification considered as equal to the required professional and technical qualification by the Ministry of Human Resources and Development.

- Can the application for registered valuer be made for all classes of assets?

Yes, provided that the applicant possesses qualification and experience specified within Companies (Registered Valuers and Valuation), 2017 for every asset and passed the valuation exam for every class applied for.

- Can registered values apply for moving from one Registered Valuers Organisation to another?

Yes, with prior written approval from the Insolvency and Bankruptcy Board of India. As per Circular No. IBBI/RVO/029/2020 (dated 28th January 2020).

- Can a working individual appear in the valuation examination and seek registration?

Yes, he/she can appear for the valuation exam during employment but the individual shall not be working while making registration as a registered valuer.

- Are all the partners or directors required to pass the valuation exam for making registration as a valuer?

Yes, All partners/directors require to pass the valuation exam as per rule 5 within 3 years from the date of applying for registration as a valuer under rule 6.

- If the self-certified experience is given on the affidavit, who is not a member of any professional institute, Will it be considered as proof of experience or not?

No, it will not be considered as proof of experience.

- If there any query or observation concerning the application, within how many it will be resolved, and what if it’s resolved within the specified duration?

The query usually gets resolved within the 21 days, but if it’s not resolved within the specified duration, then it will be deemed as rejected.

- In case, application rejected for the absence of submission of information or clarification within 21 days, Can a fresh application be filed?

Yes, but it will be considered as a fresh application.

- Where to reach if there is clarification required concerning registration as a valuer?

The person may contact the Registered Valuer Organisation (RVO). But, if the query does not get answered within 7 days from RVO, the email should be forwarded to the [email protected] along with a copy to the respective RVO.

If still there is any doubt, click here.

References

- The Companies Act, 2013

- THE COMPANIES (REGISTERED VALUERS AND VALUATION ) RULES, 2017

- https://ibclaw.in/how-to-become-a-registered-valuer/

- http://www.mca.gov.in/Ministry/pdf/Notice_14042020.pdf

- https://www.linkedin.com/pulse/key-takeaways-from-draft-valuers-bill-2020-madhur-n-agrawal

- https://taxguru.in/company-law/valuation-regime-companies-act-2013.html

- https://ibbi.gov.in/uploads/register/FAQ_Final_Ver.pdf

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications