In this blog post, Srishti Khindaria, a student of Amity Law School, Delhi, Guru Gobind Singh Indraprastha University writes about the new Income Declaration Scheme introduced in the Finance Act of 2016.

The Income Declaration Scheme, 2016 is contained in Chapter IX of the Finance Act, 2016 and provides an opportunity to all persons who have not declared their income correctly in the previous years to come forward and do so now. A scheme of similar nature was launched earlier too in 1997, known as the Voluntary Disclosure of Income Scheme (VIDS). This new Income Declaration Scheme of 2016 will remain in force from 1st June 2016 to 30th September 2016, i.e. a period of four months.

The Prime Minister, too in the 21st edition of his Man Ki Baat on 26th June 2016 asked all citizens to declare by 30th September their undisclosed income, making it clear that this would be the last chance to avoid any problems which would follow after this window closes. Mr. Modi said on his monthly radio program “For those having undisclosed income, the government has provided a special chance to declare it by September 30.”[1]

Who can avail this scheme?

This scheme is a window for all those who have not paid taxes or concealed assets in the past to come forward and declare their income and pay tax, surcharge and penalty totaling in all to forty-five per cent of such undisclosed income declared (further explained below).

This scheme shall apply to

- Any income or

- Any income in the form of investment in an asset located in India

Fair market value of the asset as on 1st June 2016 is deemed to be the undisclosed income.

- And acquired out of income that is taxable in India under the Income Tax Act

- For an assessment year before 2017-18.

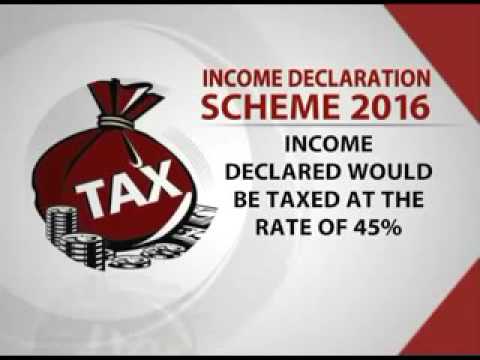

What is the rate of tax that will be charged?

Under this scheme the income declares would be taxed at the rate of 30% plus a “Krishi Kalyan Cess”of 25% on the tax payable and a penalty at the rate of 25% on the payable tax , therefore 45% of the income declared under the scheme is taxed.

What is the process of declaration?

- A declaration can be made at any time from 1st June 2016 up to 30th September 2016 in Form-1.

- Post-filing the declaration the Principal CIT who has jurisdiction or the CIT shall issue an acknowledgment in Form-2 within 15 days from the end of the month in which the declaration under Form-1 was made.

- This acknowledgment will ensure that the declarant is not liable for any adverse consequences under the scheme on any income which has been declared under the scheme but found to be ineligible for declaration.

- The declarant shall have to furnish proof of payment of tax, surcharge and penalty in Form-3 to the jurisdictional Principal CIT/CIT.

- After this proof has been furnished by the declarant, the jurisdictional Principal CIT/CIT shall issue Form-4 within 15 days. Form-4 certifies that the declaration has been accepted.

- The last date for payment is 30th November 2016.

In what cases is the declaration applicable?

The declaration is not applicable in all cases. As per the scheme the declaration for the assessment year 2016-17 or any earlier assessment year cannot be made in the following circumstances;

- Where a notice has been issued under section 142 or section 143(2) or section 148 or section 153A or section 153C of the Income Tax Act in respect of such assessment year and a proceeding is pending before the Assessing Officer. The notice must have been served upon the person on or before 31st May 2016 i.e. before the date of commencement of the scheme.

In the form of declaration i.e. Form-1, the declarant shall have to verify that he/she has not been served with any notice on or before 31st May 2016.

- The declaration cannot be made where a search has been conducted under section 132 or section 132A of the Income Tax Act, or a survey has been carried out under section 133A in the previous year and the time for issuance of a notice under section 143 (2) or section 153A or section 153C for the relevant assessment year has not expired.

In the form of declaration (Form-1), the declarant will also verify that these facts do not prevail in his case.

- Cases covered under the Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act, 2015 are also not considered valid.

- Any person in respect of whom proceedings for prosecution have been initiated under Chapter IX (offences relating to public servants) or under Chapter XVII (offences against property) of the Indian Penal Code, 1860 or the Narcotic Drugs and Psychotropic Substances Act, 1985 or the Prevention of Corruption Act, 1988 shall not be eligible to make a declaration under this scheme.

- Also, any person who has been notified under section 3 of the Special Court (Trail of Offences Relating to Transactions in Securities) Act, 1992 or any person in respect of whom a detention order has been made under the COFEPOSA (Conservation of Foreign Exchange and Prevention of Smuggling Activities Act), 1974 shall not be eligible for making declarations under the scheme.

Invalid declarations

Under the scheme a declaration shall be deemed to be void and never have been made in the following circumstances;

(a) If the declarant fails to pay the entire amount of tax, surcharge and penalty by 30th November 2016.

(b) If the declaration has been made by misrepresentation or suppression of facts or information.

Where the declaration is deemed to be void for the above-stated reasons it shall be deemed to have never been paid and all provisions, penalties and prosecutions under the Income Tax Act shall also apply if any tax surcharge or penalty has been earlier paid it shall not be refunded.

Effects of declaration

If a detailed valid declaration has been made then it will have the following consequences;

- The amount of undisclosed income which has been declared will not be included in the total income of the declarant for any assessment year under the Income Tax Act.

- The contents of the declaration shall not be admissible as evidence under the Income Tax Act and the Wealth Tax Act against the declarant in any penalty or proceedings.

- On assets disclosed in the declaration the declarant will receive immunity from the Benami Transactions (Prohibition) Act, 1988 provided that the asset with respect of which declaration of undisclosed income is made has been made transferred to the declarant or his legal representative by the Benamdar on or before 30th September 2017.

- The value of the asset declared shall not be chargeable to Wealth-tax for any assessment year(s).

- Such a declaration will not affect the finality of completed assessments, and the declarant shall not be entitled to claim re-assessment of any earlier year or any benefit or revision of any order or set off or relief in any appeal or proceedings under the Income Tax Act with respect to the undisclosed income or any tax, surcharge or penalty paid thereon.

Who is the declaration signed by?

The declaration is signed by the following

| Status of Declarant | Declaration To Be Signed By |

| Individual | Individual; if the individual is absent from Indian then any person authorized by him.If the person is mentally incapacitated then his guardian or another person competent to act on his behalf. |

| Hindu Undivided Family (HUF) | Karta; if the Karta is absent from India or mentally incapacitated from attending his affairs then by any other adult member of the HUF. |

| Company | Managing Director; if for any unavoidable reason the managing director is unable to sign or the company does not have a managing director then by the Director. |

| Firm | Managing Partner; if for any unavoidable reason the managing partner is unable to sign or if there is no such post then by any partner not being a minor. |

| Any other association | The principal officer or any member of the association. |

| Any other person | That person or anyone else competent to act on his behalf. |

Where can the declaration be filed?

A declaration can be filed in one the following ways;

- Before the jurisdictional principal CIT/CIT in paper

- Online on the website of the Income Tax office using the digital signature of the declarant or through electronic verification code.

Conclusion

The tax to GDP ratio of India is one of the worst globally. Undisclosed income is ferreted away year after year and is currently estimated to run into trillions of rupees. And this scheme is seen as a bid by the Centre to recover this stash. This is a beneficial scheme for eligible taxpayers to declare undisclosed income which was not offered to the taxation authorities in the previous financial years.

Footnote:

[1]http://www.financialexpress.com/article/personal-finance/narendra-modi-wants-you-to-reveal-your-undeclared-wealth-all-you-need-to-know-about-income-declaration-scheme-2016/297545/

References:

- http://www.incometaxindia.gov.in/Pages/default.aspx

- http://www.incometaxindia.gov.in/communications/circular/circular16_2016.pdf

- http://www.incometaxindia.gov.in/communications/notification/notification32_2016.pdf

- http://www.incometaxindia.gov.in/communications/circular/circular17_2016.pdf

- http://www.incometaxindia.gov.in/Documents/IDS-2016/Form-1-User-Manual.pdf

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications