This article is written by Saloni Surana, pursuing the Diploma Programme in Business Laws for In-House Counsels from LawSikho.

Table of Contents

Introduction

PIPE is the buying of shares of publicly traded stock at a price below the current market value (CMV) per share. The idea of PIPE (Private Interest in Private Equity) is created in the US with discrete arrangements. Notwithstanding, Indian law has no such explicit guidelines which control the PIPE bargains. The PIPE bargains in India are controlled by the particular designation rules clarified by SEBI. During unsure occasions, public organizations may end up needing extra capital, however a customary follow-on guaranteed public contribution might be far off or considered excessively hazardous. Elective approaches to get to the capital business sectors and increment liquidity through value financing incorporate, among others, “at-the-market” (ATM) contributions, enrolled direct contributions, and private interests in public equity (PIPE). This update depicts contemplations for backers and speculators thinking about a PIPE offering as an inexorably utilized technique for value financing in the current market environment.

Transactions in which public organizations issue protections in a private arrangement, or PIPEs, have been consistently ascending as of late and are moving to increment fundamentally for 2020, both in number of Transactions and complete dollar volume, in light of information and evaluations from Placement Tracker. PIPEs include the issuance in a private arrangement of traded on an open market value protections, regularly normal stock, or value connected protections, for example, convertible favoured stock, warrants, or convertible notes. In a PIPE, the backer sells a fixed number of protections straightforwardly to the financial specialists at a fixed cost, ordinarily at a markdown to advertise value, compliant with a buy understanding. The Transaction generally incorporates an enlistment rights arrangement requiring the backer to enlist the given protections (or basic protections) following shutting so the speculator may ultimately sell them uninhibitedly in the public business sectors.

Advantages of PIPE guarantors

- Accessibility: On the off chance that an unstable market presents snags to a conventional public contribution and customary bank financing is inaccessible, a PIPE might be promptly accessible, regardless of whether for issuance to existing speculators or new licensed or institutional speculators.

- Speed: A backer may acquire support rapidly in a PIPE. Financial specialists normally get genuinely light exchange explicit exposure, rather depending on freely accessible data. Contingent upon the arrangement of terms, a PIPE may meet up very quickly.

- Protection and Control: Since a PIPE isn’t openly revealed until after a buy arrangement is marked, the guarantor has adaptability to privately investigate potential terms with a speculator (regardless of whether straightforwardly or on a no-names premise through a position specialist before a financial specialist’s divider cross). This cycle may likewise permit the backer more power over the essential bearing of a PIPE offering—for instance, putting a square of value with a “white assistant” or other neighbourly speculator (especially with a proper stop understanding set up) to deflect crafty activists from exploiting market instability.

- Practical: Contingent upon the terms, PIPEs might be viewed as financially savvy options in contrast to conventional endorsed contributions, as a rule with lower exchange costs, in spite of the fact that the arranged estimating markdown might be higher.

Potential financial specialists may discover a PIPE engaging for a few reasons. During unpredictable occasions, private value and mutual funds backers may find that the vulnerability around privately owned business valuations makes privately owned business speculations harder to execute. A PIPE offers an occasion to get what could be a sizable stake in a public organization at an arranged and limited cost. Furthermore, speculators have an expanding capacity- particularly in the momentum market climate and for bigger ventures—to arrange minority financial specialist insurances in certain PIPEs like those they could get in privately owned business ventures, including the chance of a seat at the (board) table.

During times of relative market strength, backers have a more extensive scope of capital-bringing options up notwithstanding PIPE exchanges:

- A lot more backers presently are qualified to utilize a rack enlistment articulation on an essential premise. Thus, more follow-on contributions are finished as rack takedowns.

- Numerous rack takedowns utilize the divider crossing and private showcasing approach that started with PIPE exchanges.

- Notwithstanding, in times of increased market instability and in extraordinary circumstances, PIPE exchanges stay a capital-raising option of decision.

The expression “PIPE” has come to mean any private interest in a public organization, including:

- A customary PIPE;

- A private arrangement with postponed (or following) resale enlistment rights;

- A private convertible liked (fixed or floater) or organized PIPE; and

- An endeavour style, or change-of-control, private arrangement.

Each of these might be more qualified to a specific circumstance, and each raises various contemplations.

Advantages of PIPE offerings to the issuer

- Lower exchange costs contrasted with an enlisted offering.

- Permits the backer to build its institutional holder base.

- For the most part requires exposure of the exchange to the public simply after complete buy responsibilities are gotten from speculators.

- Guarantor looks to improve the evaluating of the exchange by forestalling shorting and other theoretical exchanging movements before the declaration;

- The exchange structure, for the most part, doesn’t work in non-U.S. locales in which financial specialists have pre-emptive rights over the issuance of new protections.

- Requires arrangement by the guarantor of moderately restricted contribution documentation.

Disadvantages of PIPE offerings to the issuer

Speculators quite often require a rebate to the market cost, because of restricted liquidity:

- Regularly, financial specialists may require warrant inclusion.

- Restricted to licensed financial specialists.

- Protections trade “20% Principle,” which may restrict the sum that the backer can raise without an investor vote.

- Cut-off on the quantity of “power outage periods” under the enrolment explanation.

Types of PIPEs

- Conventional PIPEs

Financial specialists resolve to buy a fixed measure of protections at a fixed cost, with the end moulded predominantly upon the SEC’s status to announce viable a resale enrolment articulation enlisting the hidden regular stock sold.

- Private placement with trailing registration rights

Private position of protections were the impacts the enrolment after the end of the private situation.

Developments in PIPE transactions

The private interest in open value (PIPE) exchange has demonstrated to be a well-known financing device in unpredictable business sectors. For the initial five months of 2020, $29.3 billion has been raised through PIPE exchanges, basically in the medical services and innovation areas.

Year-over-year since 2015, there is an outstanding expansion in the quantity of arrangements for 2020, with 533 PIPEs finished as of now. Essentially, in 2020, the returns raised through PIPE exchanges have expanded, contrasted with earlier years, with more and bigger exchanges being finished.

Unstable securities exchanges, during COVID-19, the monetary aftermath from these occasions have left numerous freely recorded organizations needing new capital, while speculators, (for example, Private Value reserves) are hoping to convey capital in a venture atmosphere where it is hard to direct conventional “buyouts”. In the spring and late-spring of 2020, this pattern happened with prominent private interests in open value (PIPE) bargains. In the U.S., the PIPE market saw $8 billion worth of arrangements in April 2020 alone, a long way in front of a normal month a year prior, and a few observers have extended an in excess of 30% expansion of PIPE action for 2020 in general.

In Canada, Washington D.C.- based Tough Capital Accomplices LP put US$ 150 million into FirstService Corp. also, Brookfield Resource The executives Inc. procured US$ 250 million of favoured offers in Predominant In addition to Corp. These exchanges signal a reappearance of PIPE bargains in Canada.

In 2018 and 2019, speculators saw an administration closure, less Initial public offerings and a fully open public market where raising capital through conventional contributions was no test for public organizations. When all is said in done, PIPE arrangements can be difficult to close because of market limitations. The Protections and Trade Commission requires investor endorsement for issuance of 20% or a greater amount of a remarkable regular stock or stock that can be changed over to normal stock. “part of exchanges that might have executed in PIPE get stumbled to public,” one of the brokers says.

In any case, given organizations’ quick requirements for capital imbuement, the SEC in April postponed this standard until 30 June. The SEC has since endorsed the New York Stock Trade’s solicitation for the waiver to be reached out to 30 September. The Central bank likewise opened up another road for public organizations to raise capital – corporate securities. Without precedent for history, the national bank began purchasing portions of trade exchanged assets mid-May in an offer to keep the credit markets above water. Right off the bat, the security purchasing office purchased $305 million worth of corporate securities, as indicated by openly accessible information.

The Central bank’s program difficulties PE firms hoping to close Line bargains as organizations race to give bonds, Enterprises gave about $265 billion under water from mid-Walk-through 27 April, as indicated by Intelligize. In May, Expedia gave $2 billion-worth of obligation. The movement organization likewise sold $1.2 billion in favoured offers to Silver Lake and Apollo Gathering The executives. “With government purchasing the better-quality organizations that may in some way or another need to acknowledge PE cash, PE folks drop further down the market,” says a convertible-market counsellor.

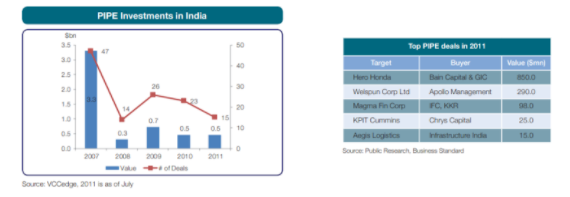

PIPE transactions in India are expected to boom, especially in the PE sector, although it has failed in the last few years. As per experts, according to the Code by SEBI, the PIPE transactions must rise by 70%, focusing on small and medium scale industries.

Conclusion

The private interest in open value (PIPE) exchange has demonstrated to be a well-known financing device in unpredictable business sectors. After the dip in the PIPE transactions in India, the rise in the same would be noticeable. The increasing PIPE transactions will surely make the equity market safe, clean and transparent.

References

- https://www.investopedia.com/terms/p/pipe.asp

- https://www.tresvista.com/wp-content/uploads/2018/03/White-Paper-Private-Investment-in-Public-Equity-India-Focus.pdf

- https://cbcl.nliu.ac.in/capital-markets-and-securities-law/pipe-transactions-a-failure-in-the-indian-scenario/

- Section 72(1)(a) of the SEBI(ICDR) Regulations, 2009

- Section 144 of the Securities Act, 1933

- Sambhav Ranka & Vyapak Desai, SEBI must set rules to avoid insider play in PIPE deals

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications