This article is written by Aditya Kasiraman, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from LawSikho.

Table of Contents

Introduction

Consolidation is a restructuring tool available to Indian conglomerates who aim to grow and diversify their businesses for a variety of reasons whether to gain competitive advantage, reduce costs or open prices. In commercial terms, a merger actually means an arrangement in which one or more existing companies merge their ownership with another existing company or form a new separate business. The company law in India is still in full swing and a new law was finally passed in 2013. However, only 98 sections of the Companies Act, 2013 (“2013 Act”) have been implemented and the provisions relating to consolidated mergers Sections 230 to 240 are yet to be announced. Until then, this court-administered procedure will continue to be governed by Section 391-396A of the Companies Act, 1956 and the Companies Act (the Court), 1959 (referred to as the “1956 Act”).

This article describes the key changes introduced by the 2013 Act regarding mergers, which is a term, in a similar way, used interchangeably under consolidation under Indian law. In addition, it is intended to compare those changes with the 1956 Act.

Framework for Merger & Acquisitions

Chapter XV of the 2013 Act deals with “Compromises, Arrangements and Amalgamations.” In this chapter, the Act covers applicable provisions and related issues for compromises, arrangements and amalgamations; however, other offers are also attracted to different stages of the process. Amalgamation means integration in accordance with the provisions of the Act. In a consolidation function that includes assets, assets and liabilities of one (or more) company are incorporated and transferred to an existing company or to a new company. Simply put, the transferor meets the transferee and the former loses its business and melts away without finishing. The 2013 law creates a new regulator, the National Company Law Tribunal (“Tribunal”) which, in its constitution, will take power (the High Courts will no longer have jurisdiction) in a court of law. Once the tribunal has been established, and the related legislation has been finalized, the provisions under the 2013 Act will apply.

Before describing the key changes under the new law, a brief overview of the existing process will be helpful. Under the 1956 Act, companies that have reached a merger agreement must prepare a consolidation plan (“scheme”). Lenders (financial institutions or banks) of both the transferor and the transferee must agree to the terms of the scheme, subject to the following approval of the relevant board of directors of the merger organizations. If the joint ventures are listed companies, then the stock exchange agreements require the company to transfer sensitive information to the stock exchange immediately, in order to seek approval from the Securities and Exchange Board of India (“SEBI”) at the same time as public information. This took place after the board’s approval of the plan. The next step is to apply to the Supreme Court with jurisdiction over the registered office of the company seeking an order to summon shareholders and lenders. Apart from obtaining further details of the process, the key point is that anyone who opposes the stakeholders can challenge the scheme in court proceedings.

Part of the preparation of the scheme is maintained under the 2013 Act. In contrast to the 1956 Act, the new state (a) recognizes boundary contexts, (b) sets out a separate procedure for the merger of small companies and holders with their full owners.

Changes in the M&A process

- Regulatory/ Third approval: Since shareholder and lender’s approval is important, the 1956 law, therefore, considers the issuance of a notice to them. The 2013 Act requires the issuance of a notice of consolidation and documentation (such as a copy of the Scheme and valuation report) not only to shareholders and lenders but also to various regulators including the Department of Business Affairs (Regional Director, Registrar of Companies and Legal Liquidator), Reserve Bank of India ( “RBI”) (where non-resident investors are involved), SEBI (listed companies only), the Competition Commission of India (where deposit limits and proposed mergers may have a negative impact on competition), Stock Exchange (listed companies only), Income Tax authorities and other sector regulators or authorities that may be affected jointly. This ensures compliance with the scheme and other legal requirements imposed by the joint venture. In fact, under the 1956 Act the courts made the merger subject to the approval of the regulators. The 2013 Act stipulates a 30-day deadline for regulators to make representations, otherwise that right may be revoked. This is a good step because in the 1956 Act no time was given which led to significant delays in court proceedings.

- Approval of the scheme by postal vote: The 1956 Act required the presence of shareholders and creditors at meetings, either in person or by an attorney, to vote on the scheme. In the 2013 Act, shareholders and lenders also have the opportunity to vote by post while considering the scheme. The 1956 law did not allow for this and stockbrokers and lenders could only vote physically. This right will ensure the full participation of shareholders and creditors, especially those scattered across the country and who find it difficult to physically present or provide representation. Post voting, therefore, will give them greater flexibility in their voting.

- Evaluation report: Although the 1956 law makes no mention of disclosing stakeholder rating reports, such as transparency and good corporate governance, the listed companies used to make the evaluation report audited during meetings. The courts also demanded the inclusion of a rating report in the application filed before them. The 2013 law now authorizes the inclusion of a rating report in meeting notices so that they can be easily accessible to shareholders and creditors.

- Objections: The ban under the 1956 Act was that it allowed shareholders and individual lenders to raise unreasonable arguments for twisting arms and unfairly harassing companies by following meetings. Such right to challenge the scheme will no longer be available to any person. The objection may be raised by shareholders holding 10% or more equity and lenders with a debt of 5% or more in total debt in accordance with the final audited financial statements. By raising the bar, the new law aims to ensure that absurd arguments/ cases can be avoided.

- Accounting standards: As a matter of practice, the scheme often provides for financial management that may deviate from the prescribed accounting standards that require this to be recorded in the company’s balance sheet. This was underestimated by the tax authorities. Consequently, in the case of listed companies, the list agreement was amended to provide an auditor’s certificate stating that the financial treatment compliant with the financial standards had to be applied for to apply for a stock exchange permit. The 2013 Act makes the previous certificate from the auditor liable for both listed and unlisted companies.

- The merger of a listed company has been added to the unregistered list: The 2013 Act specifically provides for a tribunal directive that the merger of a listed company into an unregistered company cannot be made so that an unregistered company is listed. It will remain unregistered until compliance with applicable SEBI listing rules and guidelines regarding the allocation of shares to public shareholders. In addition, should the shareholders of the listed company decide to exit, the unregistered company will make it easier to exit with a fixed price formula that will be within the price set by SEBI rules. Indian security law imposes strict enforcement of listing requirements by companies intending to be listed. SEBI, however, has reduced these requirements to the listed companies that promote mergers by granting them exemptions from compliance with the basic public requirements. SEBI recently issued guidelines stating that if the scheme provides for the listing of shares of an unregistered company without complying with the initial public offering requirements, then, when the court approves the scheme, the unregistered company must apply for certain SEBI exemptions. Such an application must be submitted, inter alia, to the allocation of financial shares to the shareholders of the listed company. The changes under the 2013 Act are in line with the requirements of SEBI. The 1956 law was silent on this issue.

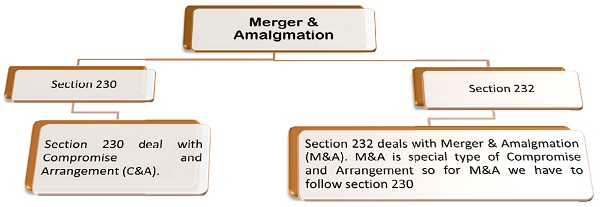

Sections relating to Merger & Amalgamation: Sections 230 & 232

In case of an application u / s 230 for Compromise & Arrangement in respect of the restructuring of a company or companies involving the merger or amalgamation of any two or more companies must state the purpose of the scheme.

Who can apply for Merger and Amalgamation proposal: Section 230(1)

Merger & Amalgamation applications can be filed with the tribunal (NCLT). Both the transfer company and the transferee company shall lodge a grievance procedure with the tribunal under Sections 230-232 of the Companies Act, 2013 for a proposal to approve a merger scheme.

Combined application

Where more than one company is involved in the process, such an application, at the discretion of these companies, may be submitted as a joint application.

However, when the office of a registered company is located in different jurisdictions, there will be two courts that will have jurisdiction over that company, which is why a separate application must be filed.

Process for M&A

It must be ensured that the companies under the consolidation must have a strong clause in the Memorandum of Association of their organization to merge although their absence will not be an obstacle, but this will make things work smoothly.

The merger scheme will be prepared to welcome you to the board meeting of each company.

- Type of Performance: An application to the court for merger and amalgamation will be submitted on form No. NCLT-1 along with the following documents:

- notice of admission on Form No. NCLT-2.

- affidavit in Form No. NCLT-6.

- copy of C&A scheme (Merger & Amalgamation).

- a sworn affidavit involving the following items: all company-related facts, e.g.:

- the company’s recent financial position.

- the latest auditor’s report on company accounts.

- the height of any investigation or operation of the company.

- reduction of company’s share capital, if any, included in the agreement or arrangement.

- any business loans rehabilitation program approved by less than seventy-five percent for lenders that are protected by value, including:

- statement of borrower’s commitment to Form No. CAA-1.

- to protect other secured and unsecured lenders.

- report to the auditor that the requirements of the company’s fund after the restructuring of the company’s debt as approved will be in accordance with the audit of the assets in accordance with the criteria provided by the board.

- when the company proposes to adopt the debt restructuring guidelines for companies specified by the Reserve Bank of India, a statement thereon; and

- stock and asset valuation report and all assets, tangible and intangible, movable and immovable, of the company by a registered valuer.

- the applicant will also disclose to the tribunal on this application, on the basis that each category of members or creditors have been identified for the purpose of approval of the scheme.

- Convening of the Tribunal: Upon hearing of the tribunal’s application, unless it deems it appropriate for any reason to dismiss the application, it will provide such order as it may deem necessary in connection with the creditors meeting or the creditors category, or the members or members category, as the case may be as follows:

- adjusting the time and place of a meeting or meetings.

- appoint the chairperson and the examiner of the meeting or meetings to be held, as the case may be and to adjust the terms of his or her appointment, including remuneration.

- adjusting the quorum and the procedure to be followed at a meeting or meetings, including voting in person or by proxy or by postal ballot or by electronic voting.

- determining the amount of creditors or members, or creditors or members of any category, as the case may be, in their meetings to be held.

- notice to be given of a meeting or meetings and an advertisement for that notice.

- notice to be given to line directors or managers as required under sub section (5) of Section 230.

- the time when the chairperson of the meeting is required to report the outcome of the meeting to the tribunal.

- other matters such as those considered by the tribunal are required.

- Notice of Meeting: Notice of meeting in accordance with court order to be issued on Form No. CAA-2 Rule 6.

- Eligible person to receive notice: Notice will be sent to each of the creditors or members and shareholders at the address registered with the company [Section 230 (3)].

- Authorized person to send the notice: Chairman of the company, or if the court is directed by the company or by another person. Ways to send notification include:

- by registered post, or by speed post, or by courier, or

- by email, or by hand delivery, or by any other means as ordered by the court.

- Documents to be sent:

- a copy of the C&A Scheme; and

- following the specified C&A details if not included in this program:

- details of the order of the tribunal directing the convening, and conduct of a meeting.

- company details including:

- Company Identity Number (CIN) or Global Location Number (GLN) of a company;

- Permanent Account Number (PAN);

- Company name;

- Date of installation;

- Type of company (either public or private or individual);

- Registered office address and email address;

- Summary of the main item in terms of the organization’s memorandum; and large corporations run by the company;

- Details of name changes, registered office and company assets over the past five years;

- The name of the transaction where the company’s security is listed, if applicable;

- Details of the company’s financial structure including authorized, disbursed, registered and paid payments; and

- Names of promoters and directors and their addresses.

- Relationships in the case of a combined application: If the relaxation or planning program affects more than one company, then the truth and details of any relationships that exist between those companies that are part of that compromise or planning program will include management, subsidiaries & related companies as well.

- Board meeting details:

- The date of the board meeting at which the plan was approved by the board of directors.

- The name of the directors who voted for this decision.

- The name of the directors who voted against the decision.

- Name of directors who did not vote or participate in that decision.

- A descriptive statement that discloses details of a compromise or plan including:

- Parties involved in such compromises or arrangements;

- Fixed date, effective date, stock exchange rate (if applicable) and other considerations, if any;

- A summary of the rating report (if applicable) including the basis of the rating and the impartial opinion of the registered rating, if any, and a declaration that the rating report is available for inspection at the company’s registered office;

- Details of capital or debt restructuring, if any;

- Reason for agreement or arrangement;

- Benefits of reductions or adjustments as determined by the board of directors of the company, members, lenders and others (as applicable);

- Amount paid by unsecured lenders.

- Disclosure of Merger & Amalgamation (C&A) results in:

- Key Managerial Personnel;

- Directors;

- Facilitators;

- Non-Movement Members;

- Stockbrokers;

- Lenders;

- Debt holders;

- Deposit and debt manager;

- Company employees;

- Company shareholders.

- Specified details:

- Investigations or further investigations, if any, still pending in the company under the Act.

- Details of approval, sanctions or objections, if any, from regulatory or other government officials who are required, who have received or are awaiting a proposed reversal of planning.

- A statement that the people to whom the notice is sent may vote at the meeting either in person or by proxies, or where appropriate, by voting by electronic means.

- A copy of the evaluation report, if any, under Section 230(3).

- Acquisition details: Details of the following documents for obtaining the issuance of or making or receiving copies or inspections by members and creditors, i.e.:

- The company’s recent financial statements including consolidated financial statements;

- A copy of the tribunal order following the meeting to be convened or delivered;

- A copy of the Merger & Amalgamation (C&A) scheme;

- Contract or contractual items in Merger & Amalgamation (C&A);

- Certificate issued by the company’s Auditor General proving the financial management, if any;

- The recommendations of the Merger & Amalgamation (C&A) scheme are in line with the Accounting Standards prescribed under Section 133 of the Companies Act, 2013; and

- Other information or documentation the board or manager believes is necessary and appropriate to make decisions or objections to the plan.

- Other documents: When an order is issued by a tribunal under Section 232(1), merging companies or companies proposed by division, will also be required to distribute the following:

- Draft proposing terms of a plan developed and approved by the directors of the merger company;

- Confirmation that a copy of the draft plan has been submitted to the registrar;

- Expert report on measurement, if any.

Case illustrations

- In the case of Kirloskar Electricals Co. Ltd., the Court held that the various sections of Section 394(1) of the Companies Act propose that both the transferor and the transferee company shall apply to the Court under Sections 391-394 of the Companies Act, 1956 for the prohibition of the agreement or arrangement involving the merger.

- In the case of Mohan Exports Ltd. v/s Tarun Overseas Pvt. Ltd., it was held that if both companies are under the jurisdiction of the same Supreme Court, a joint application may be made.

Penalties

Penalties for breach of provisions under the 1956 Act were INR 50,000 applicable to the company. However, under the 2013 Act, separate fines were paid to the company and its defaulting manager. To bring more accountability, the penalties increased from the above mentioned amount to a minimum of INR 100,000 and a maximum of INR 2,500,000. Officials will also be punished with imprisonment for up to one year or a small fine of INR 100,000 and INR 300,000 or both for consolidation of small companies by those of a holding company and wholly owned subsidiaries unless their mergers are referred to the tribunal and approved by it.

Conclusion

While a few significant changes have been proposed, companies may see the need to obtain multiple approvals from different regulators as a difficulty. However, the 30-day limit set by regulators will, hopefully, ensure that they respond in a timely manner. At the same time, the 2013 Act provides a complete and effective transparency that ensures the protection of stakeholders’ interests, while at the same time avoiding unnecessary disputes. The time frame for which the entire merger process will be involved will be determined once it has been tried and will take place after the tribunal has been established and the rules used. It would be fair to say that the 2013 Act aims to simplify and make M&A smoother and more visible. The new provisions should make it easier for companies that promote mergers as the spears have a good check system and balance to prevent abuse of these provisions.

References

- https://www.mondaq.com/india/corporate-and-company-law/289180/merger-regime-under-the-companies-act-2013

- https://taxguru.in/company-law/merger-amalgamation-companies-act-2013.html#:~:text=Section%20230(1),sanctioning%20the%20scheme%20of%20amalgamation

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications