According to Bloomberg Businessweek, Google has saved $3.1 billion since 2007 and boosted last year’s overall earnings by 26 percent. According to company disclosures, Apple, Oracle, Microsoft and IBM—which together with Google make up the top five technology companies by market capitalization—reported tax rates between 4.5 percent and 25.8 percent on their overseas earnings from 2007 to 2009.

The million dollar question is HOW?

It involves a tax avoidance strategy. These strategies might range from simple maneuvers to diabolically complex schemes of the shuttling back and forth of income earned overseas in order to reduce the tax burden of a company. And don’t be scandalised. These strategies are perfectly legal- exploiting the idiosyncrasies of national tax policies worldwide and milking loopholes in the law. Not necessarily ethical per se, but legal.

Coming back to the question at hand, Google and the Top 5 took the help of a few tax avoidance strategies to boost their earnings worldwide. One such ingenious scheme is the Double Irish with the additive Dutch Sandwich making for a sumptuous meal for the bigwigs in the USA. These path-breaking and delectable- sounding tax avoidance strategies are discussed below for the uninitiated.

First Things First: The Double Irish Arrangement

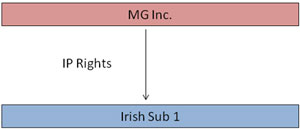

1. First we have a US Parent Company (lets say Microgoapacle, MG for short)

![]()

2. MG transfers its Intellectual Property Rights (meaning patents over inventions made by them, trademark related rights, or copyright on software or code – it could be anything depending on the business) to a subsidiary (child) of MG in Ireland

“Ah!”, you’d say, “and why would MG do that?” The fun part is yet to come.

Effect of transferring IP Rights to Irish Sub 1:

If MG assigns the rights over its intellectual property in Italy to Irish Sub 1, which would mean that the subsidiary would have all the rights over the invention in Italy that MG enjoys in the US. Irish Sub 1, in return (at least on paper) would market the product in Italy and pay for it from the profits arising from its sale.

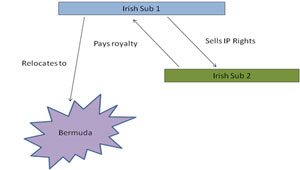

3. The Bermuda Triangle: Where money goes once, never to be found again

Irish Sub 1 relocates to Bermuda and becomes a double tax resident. This means two things:

- According to US tax laws, IS 1 is still resident in Ireland.

- According to Irish tax laws, the company is resident in Bermuda, since Ireland’s laws of taxation do not mandatorily require that companies incorporated in Ireland be resident there. Instead if the company is controlled and managed from outside Ireland, the company may elect to begoverned by the tax laws of that other country.

What can be the advantages with respect to tax-reduction by this relocation? Before we answer that question we need the help of another twist.

MG Inc. then sets up a second subsidiary namely IS 2 in the diagram above. According to Irish provisions (explained in point 2 above), this means that even if it is assumed to be controlled and managed by the parent company, i.e., MG Inc., since it was incorporated in Ireland, it can opt to be governed by either Irish or American tax law. It chooses Irish.

IS 1 then sells the IP Rights given to it by MG Inc. to IS 2. So now IS 2 can commercially exploit the rights. In return, Irish Sub 2 pays Irish Sub 1 royalties for the intangible assets gained by it.

Why this twist?

- There is no income tax in Bermuda!!! Bermuda is one of the tax havens of the world, and hence the royalties received by IS 1 in payment for the IP Rights “sold” to IS 2 is free from tax!

- The IRS in the US cannot tax income of IS 2 (profits from commercial exploitation of IP Rights) as it elects to be governed by Irish Laws!

- Income received from commercial exploitation of the IP right by IS 2 is now taxable @ 12.5% compared to 35% in the US, as IS 2 is tax resident in Ireland.

- The outflow of money from IS 2 to IS 1 is not taxed as no withholding tax is charged for flux of money within the EU. IS 1 if you remember, is incorporated in Ireland and so is IS 2. So the transfer of royalties is seen to be a transaction between two Irish companies and is hence tax free!

Now for the Dutch Sandwich…

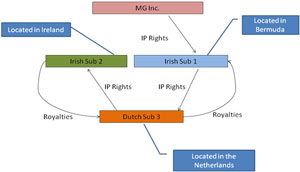

Now keep the Double Irish setup in your mind and make the following modifications:

- Instead of selling IP Rights to IS 2, IS 1 sells them to a subsidiary of MG Inc. incorporated in the Netherlands, Dutch Sub 3 (DS 3).

- DS 3 then sells the IP Rights to IS 2, forming a sort of loop de loop in the middle of the Double Irish Agreement.

- The royalties paid by IS 2 to DS 3 are then channelled to IS 1.

Advantages of the Dutch detour

- Royalties paid by IS 2 to DS 3 are not chargeable by virtue of being a money transfer within the EU (from Ireland to the Netherlands).

- Netherlands takes only a small fee in the royalty paid by DS 3 to IS 1, i.e. from Netherlands to Bermuda, hence the royalty reaches Bermuda almost untaxed.

- Bermuda is income tax free zone, hence no tax on royalties received by IS 1.

The author Milinda Sengupta is currently studying at the Ram Manohar Lohia National Law University (RMLNLU), Lucknow

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Thanks for this easy to understand explanation.

[…] How Google, Microsoft, Apple and other US tech giants save billions (here) […]