In this blog post, Saanvi Singla, a student of University Institute of Legal Studies, Panjab University, explains the concept of money laundering and lists some of the key techniques which are predominantly used for laundering money.

Introduction

Money laundering is the procedure of changing the returns of wrongdoing and defilement into apparently true blue resources. In various legitimate and administrative frameworks, in any case, the term government evasion has gotten to be merged with different types of budgetary and business wrongdoing, and is in some cases utilized all the more for the most part to incorporate abuse of the money related framework (including, for example, securities, advanced monetary standards, MasterCards, and customary coin), including terrorism financing and avoidance of worldwide assets. Most of the tax evasion laws transparently merge government evasion (which is worried about the wellspring of assets) with terrorism financing (which is worried about the destination of assets) when managing the money related framework.

Few nations characterize government evasion as muddling wellsprings of cash, either purposefully or by just utilizing money related frameworks or administrations that don’t distinguish or track sources or destinations. As Money Laundering is a worldwide phenomenon, several techniques exist through which the said crime takes place all around the world.

Techniques used

There are many techniques through which money laundering can take place. Some of the most common techniques used in money laundering are-

-

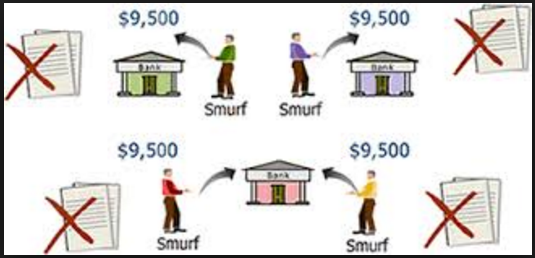

Deposit structuring/smurfing

This procedure includes making various deposits of little sums beneath a reporting limit, either by countless detached investors or to an extensive number of accounts. The cash is then by and large, exchanged to another record. Once in a while a few gathering accounts are utilized, and every one of them courses their assets to another account, thus the cash continues revolving. Nations, to which these assets are exchanged, regularly discover the assets being quickly expelled as cash from the beneficiary records.

-

Cash deposits followed by telegraphic transfers

Large cash deposits might be made by medication traffickers or other people who have smuggled criminal property out of the nation where the wrongdoing started. Frequently the cash deposit is immediately trailed by a telegraphic exchange to another ward (which could be the first nation where the wrongdoing was submitted), in this way bringing down the danger of seizure.

-

Connected Accounts

Recognizable proof necessities have a tendency to hinder, or possibly make it troublesome for criminals from opening accounts in false names. Be that as it may, accounts may at present be held in the names of relatives, partners or different persons working for the benefit of the criminal. Different strategies are used to shroud the beneficial owner of the property including the use of shell organizations, quite often fused in another locale and experts, for example, legal advisors or seaward consolidation specialists. These methods are regularly consolidated with a few layers of exchanges and the utilization of various records, hence making endeavors taken after the review trail of the supports more troublesome.

-

Collection Accounts

Collection amounts are utilized by a wide range of ethnic gatherings. Foreigners pay a considerable measure of little sums into a solitary record, and the gathered assets are then sent to another country in a solitary exchange. Frequently, the remote records get installments from various obviously detached records in the source nation. While this payment technique is regularly used for legitimate purposes by migrants and workers who send cash to their nation of origin, it can be, and is, utilized by criminal gatherings to wash their illegitimate assets.

-

Payable-through Accounts

Payable-through Accounts are demand deposit accounts maintained at financial institutions by foreign banks or corporations. The foreign bank funnels the deposits and cheques of its customers (usually individuals or businesses located outside the country) into a single account that the foreign bank holds at the local banks. The foreign customers have signing authority over the account as sub-account holders and can thereby conduct normal international banking activities. Many banks offering these types of accounts have been unable to verify or provide any information on many of the customers using these accounts. Payable-through accounts, therefore, pose a challenge to “know your customer” policies and requirements and suspicious activity reporting guidelines.

-

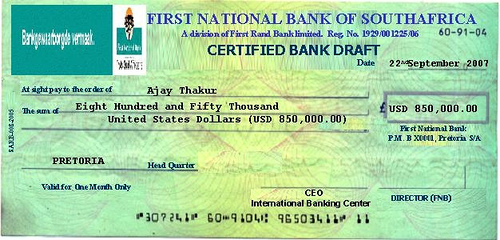

Bank Drafts and Similar Instruments

Bank drafts, money orders, and cashier’s cheques purchased for cash are useful for laundering purposes because they provide an instrument drawn on a respectable bank or other credit institution and so break the money trail. Breaking this trail is of critical importance to the money launderer, as it makes it impossible – or at least very difficult – for an investigator to establish where laundered funds have ended up. This reduces the ability of the law enforcement authorities to seek a judicial order to appropriate such funds.

-

Back-to-Back Loans

Back-to-back loans arrangements of action can be utilized for smuggling cash. A cash launderer exchanges his/her criminal proceeds to another nation as security or guarantee for a bank credit, which is then sent back to the first nation. This strategy not only gives laundered cash the presence of a genuine loan, however regularly gives charge focal points.

-

Bureaux De Change

Bureaux de change (or equivalent) services – such as telegraphic transfer facilities and exchange services, which can be used to buy or sell foreign currencies, to consolidate small denomination bank notes into larger ones, or to exchange financial instruments such as traveler’s cheques, Euro cheques, money orders and personal cheques which can be attractive to money launderers. Criminals will be attracted to bureaux de change in jurisdictions where they are not as heavily regulated as traditional financial institutions, or where they are not regulated as traditional financial institutions, or where they are not regulated at all. Even when regulated, the degree of regulation is often less training within bureaux de change and their internal control systems to guard against money laundering, to be less strong than in other financial institutions.

This weakness is compounded by the fact that most of the customers of the bureaux de change are occasional, making it more difficult for them to ‘know their customer’, thus, making them more vulnerable to money launderers.

-

Remittance Services

Remittance systems operate in a variety of ways. Often, the remittance business receives cash, which it transfers to the banking system of another account held by an associated company in the foreign jurisdiction. There, the money can be made available to the ultimate recipient. Another technique commonly used by money remitters and currency exchanges is for the criminal organization to receive the funds in the destination country in the local currency, which is then sold to foreign business people who need currency to fund the legitimate purchase of goods and export. The attractiveness of this avenue in particular countries is often encouraged by the existence of strict exchange control. Remittance services are a feature of many ethnic groups; they often charge a lower commission rate than banks for transferring money to another country and have a long history of being used for money laundering, since they are often subject to few, if any regulatory requirements compared to institutions, such as banks, which an equivalent service.

-

Credit and Debit Cards

Structured cash payments for outstanding credit card balances is the most widely recognized use of Visas for tax evasion, frequently with moderately substantial payments as installments and in some cases, with money installments from outsiders. Another method is to use loans from Visa records to buy cashier’s checks or to wire assets to outside destinations. On some events, loans are kept into investment funds or current records. A substantial number of distinguished situations include the utilization of lost or stolen cards by outsiders.

Laws made for Money Laundering

Many laws have been made to tackle the problem of Money Laundering. The Indian Legislature made the Prevention of Money Laundering Act, 2002. This act has been amended multiple times so that it can meet the needs of the hour.

Conclusion

These are a few main techniques through which the market of money laundering is flourishing all around the world. It is very important to understand these techniques to understand the concept of money laundering. By understanding these techniques, new laws can be made to tackle the problem of money laundering.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications