Kashish Khattar is a 4th-year student at Amity Law School, Delhi. This article is a discussion revolving around Venture Debt and how it works in the Indian startup sphere.

Introduction

Venture Debt allows the business to get money for a steady cash flow even if they are not creditworthy to get a loan typically due to the loss of any tangible asset in hand. Venture Debt fills the gap created between the venture capital and traditional banks loans. This is done by understanding the business model of the startup, seeing there is a concept in place and assuring that there is a good chance of success. The Venture Debt funds give out the steady cash flow that the business demands with a set of typical specific conditions that include a higher rate of interest and share warrants that would enable them to buy company’s shares at a discount in the next round of equity investment.

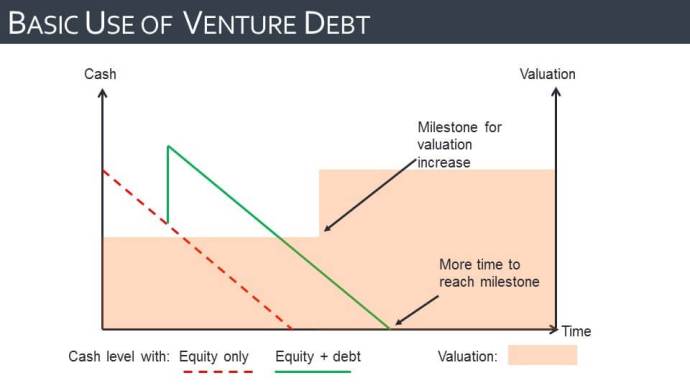

Venture Debt works because equity is expensive, the startups basically work in intangible assets and usually have no collateral to access the required finance for their growth. It is typically seen that venture debt has a lot of uses. Equity is mainly used up for R&D purposes or some long-term investments. However, debt is used for various other reasons such as capex and working capital. The biggest reason for an Indian startup founder to take up debt as an option is because it does not dilute the stake of any early stage investor or founder. It also gives them a lifeline of around 3-4 months before the next round of equity funding.

Venture Debt v. Venture Capital

Venture debt is typically meant for a more mature business who refuses to give more equity or seats at the table at that point of time. Venture debt is mostly seen in startups after they are done with their Series A and B round and now just need a capital inflow to grow the company in the required strategic direction. Further, they do not want the founder’s stake to be diluted after a point. Venture debt can be seen as a cheap form of raising funds. A higher share of the pie can be used at the time of a strategic sale or a public listing. Venture debt providers are not as involved as typical VCs in the management of the business and thereby reduce the administrative pressure for a founder. However, Venture Debt is more or less interrelated with Venture Capital. The startup ecosystem has to be mature enough to let venture debt gain traction. It particularly takes around 10-15 years to kick in, as can be seen from the market scenario of the country. Venture capital emerged in the early 2000’s and the venture debt boom seems to have happened around 2015-16.

How venture debt is seen in India

Venture Debt is essentially seen as a bridge without diluting equity in the Indian startup space. Venture Debt typically works as typical ‘bank loans’ except there is no collateral involved and those startups are not making any kind of profit. However, this kind of debt comes with a fixed coupon, a tenure and a timeline on how to pay back the principal and interest after the initial moratorium phase. It has been procured by popular names in the startup-sphere such as Snapdeal, Faasos, Portea, Rivigo, Myntra, Freecharge, Practo, Yatra, UrbanLadder, OYO Rooms, Byju’s, Swiggy, Zoom Car, Helpchat, UrbanClap, BigBasket, Yatra.com, Pepperfry, Ninjacart etc. Venture Debt gives the startup some time to grow. Venture Debt is seen as something of a segment that is growing in the startup space since 2015.

Click here

How does it work?

A venture debt firm typically gives out a loan of around three years and charges an interest rate which can range from 14% to 18% with monthly repayments of principal and interest. Venture debt is mainly pledged against the goodwill or brand value of a startup, their Intellectual Property Rights or a type of lien on their fixed assets. Further, the funds that are dealing in venture debts build an equity kicker in the form of various share warrants that are typically linked to the last-round valuation or issued at a discount to the next round’s valuation. This adds up to the internal rate of return (“IRR”) of a fund which can attract more investors.

Venture debt can be seen as a safe product from a fund’s point of view, venture debt loss ratios globally amount to 2-4% unlike 30% in the case of venture capital. That is the reason why traditional conservative institutional investors like insurance and pension funds are quite open to the idea of investing in venture debt funds. The risk taken by a debt firm is quite minimal as compared to a VC firm. A venture capitalist has to get creative and really believe in the vision of startup to invest millions in it and then wait for it to get back to them tenfold. The risk is bigger and so is the reward.

Venture Debt is quite the opposite as compared to Venture Capital, it is short-term and straightforward. A venture debt firm just looks at the startup to figure out if they would be able to make payments against their principal, interest and would they be able to make it to their next round of funding. Venture debts can give returns independent of the fact that Venture Capitalist has made any kind of money or got an exit.

Banks and Venture Debt

Venture Debt was used to fill in the space created between Venture Capital and traditional banks loans, so why would banks invest in Venture Debt funds?

The answer lies in the one thing that makes banks tick – interest. Banks can earn a good amount of interest by investing in a venture debt fund, it is a low hanging fruit for banks with attractive returns. Venture debts can be seen as a low-risk investment with higher returns. With the venture ecosystem set to grow exponentially, banks don’t want to be left behind. Further, the RBI now allows banks to invest up to 10% of the paid-up capital or unit capital in Category I or Category II Alternative Investment Funds. Private Equity and Venture Debt funds fall under Category II, which makes way for banks to start investing in the ever-growing Venture space.

The interest rate related to a venture debt fund is quite higher than traditional lending and brings an amazing opportunity to earn higher yields. The funds are also said to be quite flexible as a venture debt fund pays banks interest rate on a quarterly basis from the debt fund. These funds as discussed above have provisions regarding equity warrants which have a potential to bring in more yields if the venture turns out to be successful. Further, all the headache regarding the operations is taken by the venture debt fund – the banks are getting better returns with little to no efforts. Quite a large number of successful ventures can turn into potential big business clients for the banks, establishing an early relationship with a particular bank. An early relationship can quite easily establish a long-lasting source of income. The idea of partnerships of banks and a successful venture is also not unheard of. For example, BigBasket was connected by a specific venture debt fund with several banks to help them develop a modern supply chain in the agricultural sector.

However, the investment in venture debt funds is not an easy path as discussed, the investment may sound lucrative but with the NPA problem looming large over the banking sector. It can be seen as a risky investment in technologies and intangible assets, a forum where banks hold no type of expertise. Further, Indian banks are still too traditional with their lending principles. In addition are their highly regulated risk mechanisms set up by the central bank. It can be quite a daunting task for them to invest in the venture debt space.

Conclusion

Venture Debt investors expect to deploy around USD 300 million in the Indian venture ecosystem which is expected to touch USD 3 billion in venture capital. As I have said earlier in the article, the growth of Venture Debt and Venture Capital are interrelated. Developed markets have a typical trend of forming 10% of the equity markets. It is quite important for the venture ecosystem to expand to let Venture Debt make an impact on the market. The role of all the stakeholders in the venture ecosystem in this growing segment is enormous. Venture Capital firms are already expanding their horizons and starting their own Venture Debt funds for an expanding business. Venture debt is also being seen as a way of M&A where the funds are giving out capital to businesses to acquire firms to expand. The scope of Venture Debt, in my opinion, is huge. It is to be seen as to how the market adjusts to this segment and the various implications it has on the venture ecosystem as a whole.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications