This article is written by Srijita Adak, pursuing a Diploma in Advanced Contract Drafting, Negotiation, and Dispute Resolution from LawSikho.

Table of Contents

Introduction

With the help of the definition of banking under the Banking Regulation Act, 1948, we can assume that banking is not a very easy process to run. In this complicated process, to run the bank easily it is an essential obligation of a bank to deal with the working capital effectively. As the working capital is the operation liquidity of a business. It should neither be inadequate nor excessive. Working capital management strategies of a firm greatly affect the benefit, liquidity, and design soundness of the association. A fundamental objective of working capital management is to deal with the current resources and current liabilities of the firm so that a palatable degree of working capital is kept up with.

In the event that a business association doesn’t extend their networking capital enough, they need to fight for covering its bills. Yet, if they increment the functioning of working capital too much, the productivity of the association can be reduced. To stay away from issues, associations need to use sound decisions which crossover between how current assets and current liabilities are utilized. The reason behind the working capital management is to guarantee that adequate money is accessible to meet everyday income needs, pay wages and pay rates when they fall due, pay creditors to guarantee proceeds with provisions of labor and products, pay government tax assessment and supplier of capital-profits and guarantee the long-term endurance of the business organisation.

Working capital and working capital management

In short, working capital is the overabundance of current assets over current liabilities. Working capital has customarily been characterized as the overabundance of current resources over current liabilities. It is in this manner that it is said that the destiny of huge scope interest in fixed resources is regularly controlled by a generally limited quantity of current resources. As the working capital can be the lifesaver of an organization, on the off chance this lifesaver may break down. So, a company must have sufficient working capital.

Networking capital demonstrates the difference between current assets and current liabilities. Net Working limit demonstrates the liquidity position of the firm.

|

Working Capital/Net Working Capital = Current Assets – Current Liabilities. |

Current assets are assets that can be converted to cash in 1 operating cycle or a maximum 1 yr. Example- Cash, Accounts Receivables, Inventory (Raw Material + WIP Stocks + Finished Goods). Current liabilities are accounts payable (short-term liabilities payable in 1yr.). Example-bank loans, cash credit, overdraft, overdue – salaries, rent, etc.

Working capital management refers to managing the working capital of an enterprise. By calculating the current assets and current liabilities, net working capital can be overseen which is needed for working capital management. This ensures the availability of ample funds at the time of need.

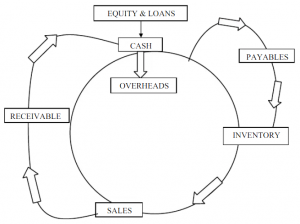

Working capital cycle

It is the timeframe that slips by where money starts to be used on the creation of an item and the assortment of money from a client. There are inventories, receivables, and payables and each one of them has two degrees- time and money. Exactly when they come to administering working capital time is money. In the event that you can get cash to move quicker around the cycle (gather monies due from indebted individuals all the more rapidly) or lessen the measure of cash restricted (decrease inventory level comparative with sales). The business will produce more money or it should acquire less cash to finance working capital. As an outcome, we could diminish the expense of bank revenue or we will have extra free cash accessible to help the expansion of deals, development, or speculation.

Banking sector

Banking sector is a stepping stool to different areas for their improvement and their development. Accordingly, a solid bank area is needed for the financial development of a country. After the changes in 1991, banks are developing by jumps and leaps. The amendment of the Banking Regulation Act in 1993 saw the evolution of new private sector banks. This fragment extensively comprises:

- Commercial Banks,

- Co-operative Banks.

Here we need to understand the commercial banking structure. It consists of-

- Scheduled Commercial Banks,

- Unscheduled Banks.

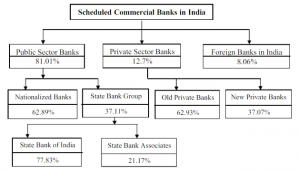

Scheduled Commercial Banks set up those banks which have been added to the second schedule of the Reserve Bank of India (RBI) Act, 1934. RBI accordingly adds those banks for this schedule that satisfy the guidelines put down vide region 42 (60) of the Act. This sector can be divided into-

- Public sector,

- Private sector,

- Foreign sector.

The main shareholders of the public sector are either Government of India or the Reserve Bank of India. The public sector consists of-

- State Bank of India (SBI) and its subsidiaries,

- Other nationalised banks.

The law administering banking exercises in India is known as the “Negotiable Instruments Act 1881“. The financial exercises are mentioned hereinafter:

- Taking deposits from public/others (deposits),

- Lending cash to the public (loans),

- Moving cash starting with one spot then onto the next (remittances),

- Going about as trustees,

- Going about as mediators,

- Keeping assets in safe authority,

- Assortment business,

- Government business.

The present situation of banks

At present, by and large, banking in India is considered as genuinely developed. Indeed, even as far as nature of resources and capital ampleness is considered, Indian banks are considered to have spotless, solid and straightforward accounting reports when contrasted with different banks in equivalent economies in their district. The Reserve Bank of India is a self-sufficient body, with insignificant pressure from the public authority. The expressed strategy of the Bank on the Indian Rupee is to oversee unpredictability expressed conversion scale and this has generally been valid with no expressed conversion scale. With the development in the Indian economy expected to be solid for a long while particularly in its administrations area, the interest for banking administrations especially retail banking, home loans and speculation administrations are required to be powerful. M&A, takeovers, resource deals and considerably more activity (as it is unwinding in China) will occur on this front in India.

The first run through a financial investor has been permitted to hold over 5% in a private sector bank since RBI declared standards in 2005 that any stake surpassing 5% in the private sector banks would should be checked by them. Presently, India has 88 Scheduled Commercial Banks (SCBs), 28 Public Sector Banks, 29 Private Banks (these don’t have government stake; they might be freely recorded and exchanged on stock trades) and 31 Foreign Banks. They have a consolidated organization of more than 53000 branches and 17000 ATMs. As indicated by a report by ICRA Limited, a rating office, the public sector banks hold more than 75% of absolute resources of the banking sector, with private and foreign banks holding 18.2% and 6.5% separately.

SBI

SBI’s roots can be traced back to the first bank of India, the Bank of Calcutta, which was founded in 1806. However, SBI’s direct predecessor was the Imperial Bank of India. The State Bank of India arose as a pacesetter, with its tasks completed by the 480 workplaces containing branches, sub workplaces, and three local head offices, acquired from the imperial bank. Rather than filling in as simple archives of the local area’s reserve funds and loaning to reliable gatherings, the State Bank of India obliged the requirements of the clients, by banking deliberately. The bank served the heterogeneous monetary necessities of the arranged financial turn of events.

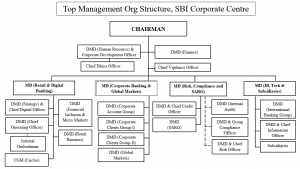

Organisational structure

The organisational structure of SBI is very strong. There are other private financial banks that were in a difficult situation in light of overburden and in the meantime SBI was dealing with multiple times of responsibility. You can discover SBI branches and ATMs in regions we won’t anticipate that they should be there.

Products and services

Individual banking

- SBI Term Deposits,

- SBI Loan for Pensioners,

- SBI Recurring Deposits Loan Against Mortgage of Property,

- SBI Housing Loan Against Shares and Debentures,

- SBI Car Loan Rent Plus Scheme,

- SBI Educational Loan Medi-Plus Scheme.

Different services

- Farming/rural banking,

- NRI services,

- ATM services,

- Demat services,

- Corporate banking,

- Internet banking,

- Mobile banking,

- Worldwide banking,

- Safe deposit locker,

- RBIEFT,

- E-Pay,

- Gift cheques,

- Treasury operations,

- Associates and subsidiaries.

Working capital management of SBI

To analyse working capital management, we need to know the working capital of SBI. So, to determine the working capital we need to analyse the total current assets and the total current liabilities. Then we have to subtract them.

-

Calculation of current assets of SBI from the Balance Sheet of SBI:

|

Particulars |

March 2020 (in USD) |

March 2019 (in USD) |

|

Cash & cash equivalents |

37,669,727 |

70,698,904 |

|

Loans and advances to banks |

21,301,184 |

103,239,935 |

|

Loans and advances to customers |

480,676,142 |

279,108,746 |

|

Investment securities |

109,471,373 |

148,714,650 |

|

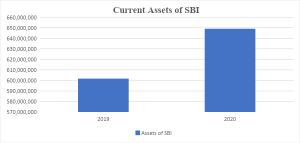

Total Current Assets |

649,118,426 |

601,762,235 |

-

Increase or decrease of current assets of SBI

|

Particular |

2019 |

2020 |

|

Current Assets |

601,762,235 |

649,118,426 |

|

Increase(/Decrease) |

47,356,191 |

|

|

%Increase(/Decrease) |

7.87% |

-

Current assets of SBI in graphs

-

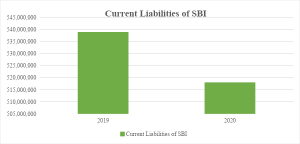

Calculation of current liabilities of SBI from the balance sheet of SBI

|

Particulars |

March 2020 (in USD) |

March 2019 (in USD) |

|

Deposit from customers |

438,352,611 |

484,045,968 |

|

Other borrowed funds |

71,500,000 |

46,089,650 |

|

Subordinated liabilities |

6,817,208 |

8,082,246 |

|

Current tax liabilities |

1,345,589 |

673,195 |

|

Total Current Liabilities |

518,015,408 |

538,891,059 |

-

Increase or decrease of current liabilities of SBI

|

Particular |

2019 |

2020 |

|

Current Liabilities |

538,891,059 |

518,015,408 |

|

Increase(/Decrease) |

-20,875,651 |

|

|

%Increase(/Decrease) |

-96.13% |

-

Current liabilities of SBI in the graph

-

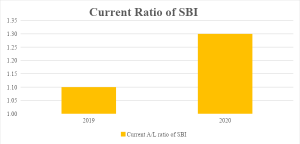

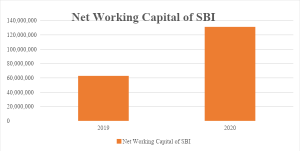

Networking capital and a current ratio of SBI

|

Particulars |

2019 |

2020 |

|

Current Assets |

601,762,235 |

649,118,426 |

|

Current Liabilities |

538,891,059 |

518,015,408 |

|

Net Working Capital |

62,871,176 |

131,103,018 |

|

Increase(/Decrease) |

68,231,842 |

|

|

%Increase(/Decrease) |

108.53% |

|

|

Current ratio |

1.1 |

1.3 |

-

Networking capital and current ratio in graph

Findings

This is an analysis of working capital management for the year 2019-2020. The findings of this analysis are-

- Here the current ratio for both the years is more than 1; So, the company can easily meet the short-term liability.

- In the year 2020, the current ratio is between 1.2-2 which is a healthy ratio that means the company has utilized its working capital efficiently. So, the funds are neither idle nor locked up in inventories or receivables.

- The working capital has increased by 108.53% in the year of 2020.

- As the working capital has increased in the year of 2020, the liquidity position is good.

- Working capital expanded due to augment in the current assets rather than expansion in the current liabilities.

- The company’s current assets have influenced the benefit of the organisation as it was in every case more than necessity.

- In both the years, the current assets are more than current liabilities which demonstrates that SBI has utilised its long-term assets for transient pre-requisite though long-term assets are more expensive than short-term assets.

- More current assets segments show that sundry debtors have a significant part in current assets which shows the efficient management of wasteful receivables.

Overall the organization has a great liquidity position and adequate assets to reimbursement of liabilities, however, the company has acknowledged a moderate monetary approach to keeping up with more current resources balance.

Suggestions

After analysis we can come up with some suggestions which can be utilized for the development of the company. They are-

- The company should keep up with appropriate administration in inventory.

- Current assets should not be surpassed over on the grounds that they may increment the investment of the organization. The networking capital ought to be in an equilibrium condition and it should not change unnecessarily.

- Organisation should raise assets through short-term origins for the transient necessity of assets, which is similarly prudent in contrast with long-term reserves.

- Organisation should take control of the debt holder’s assortment period which is a significant piece of current resources.

- Organisation needs to take control on cash balance since cash is non acquiring resources and can be expanding cost of assets.

All over the organization ought to deal with the NWC of the organisation so that it should improve the adequacy and proficiency of the organisation’s benefit.

Conclusion

Working capital management is a significant part of monetary administration. The investigation of working capital management of State Bank of India has uncovered that the current proportion is in an expanding pattern. The examination has been led on working capital administration which will assist the organization with dealing with its working capital productively and viably.

Overall the organisation has a great liquidity position and adequate assets to reimbursement of liabilities. Organisation has acknowledged traditionalist monetary arrangement and hence keeping up with more current resources balance. Organisation is expanding deals volume each year which is upheld to the organization for supporting it to sustain in India. From this analysis, we can see that the general working capital (WC) of the State Bank of India has expanded by in excess of 100% over the most recent years which is a critical pattern and this pattern gives a strong structure for the wellbeing of the organisation.

References

Books:

- Financial management by I. M. Pandey

- Financial Management by Dr. Satish Inamdar.

- Business Environment by K. Aswathappa and G. Sudarsana Reddy.

Websites:

- www.sbi.co.in

- www.rbi.org.in

- www.moneycontrol.com

- www.capitalmarket.com

- www.scribd.com

Students of LawSikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications