In this article, Mohammed G A who is currently pursuing M.A. IN BUSINESS LAWS, from NUJS, Kolkata and Hiteshi Wadhwani, a fourth year law student from SVKM’s NMIMS Kirit P. School of Law, Mumbai, discusse Corporate Social Responsibility in India.

INTRODUCTION

The concept of Corporate Social Responsibility (CSR) rests on the philosophy of give and take. As the corporate entities utilize valuable resources from the society in the form of raw materials, human resources etc., for its operations, the corporates should act as trustees of the society and must give back something for the welfare of the society. In common parlance, CSR is a term broadly used for defining the responsibilities of corporate world towards the society & environment. While the term CSR is not novel in this corporate world but its scope and meaning has endured major changes from considering it as a mere voluntary charitable activity in comparison with the obligations of the Corporate towards the outer world. There are many large corporate groups who have been actively involved in the CSR activities but regrettably, the number is relatively less. With the objective of inciting more corporate groups to contribute in the process of development of the society by way of CSR, the Government of India has actually implemented the concept of CSR in the new Companies Act 2013. On February 27, 2014[1], the Government of India has notified the guidelines for CSR spending under Section 135 Companies Act, 2013 and Schedule VII[2] of the Companies Act as well as the provisions of the Companies (Corporate Social Responsibility Policy) Rules, 2014 (CSR Rules) which has come into effect from 1 April 2014.

This scope of this article begins by developing a general understanding of the concept of CSR, based on global practices, Indian tradition, and the object and provisions of the Companies Act, 2013. It further emphasises the key features of Section 135 of the Companies Act, 2013, Schedule VII of the Companies Act 2013 and the Companies (Corporate Social Responsibly) Rules, 2014 and highlights its implications to companies.

CSR IN GLOBAL CONTEXT

There is no universally accepted definition for the term CSR, but to understand the meaning of it in simple words, one might go through the definition which has been given by the European Commission. The definition states that “CSR is the responsibility of the enterprises for their impact on the society…Enterprises should have in place a scheme to integrate ethical, social, environmental and consumer concerns in their business and core strategy, in close collaboration with their stakeholders”.[3]According to the Unites National Industrial Development Corporation (UNIDO), “Corporate social responsibility is a management concept whereby companies integrate social and environmental concerns in their business operations and interactions with their stakeholders”.[4]

The concept of CSR has been introduced all across the world but different countries have different ways of application. But the common thing is that all the countries use the LBG model to measure the real value and effect of their community investment to the society and business. In developed countries like USA CSR team in the Bureau of Economic and Business Affairs heads the Department’s involvement with U.S. businesses in the advancement of responsible and ethical business practices. In US corporate community contributions by US companies are ten times higher than those of their British counterparts[5] and further, US companies typically disclose CSR activities on their websites like the provision of combating climate change or providing better health care which has not appeared until recently on the websites of European companies. In EU, the CSR policy is built upon guidelines and principles laid down by the United Global Compact, United Nations Guiding Principles on Business and Human Rights, ISO 26000 Guidance Standard on Social Responsibility and OECD Guidelines for Multinational Enterprises.

The institutional context of CSR for Countries such as Japan, South Korea and Taiwan, was in terms similar to that of European Continent. They are characterized by a high bank and public proprietorship, masculine and long-term service, and coordination and control systems based on long-term relations and partnerships rather than markets. The Japanese ‘Keiretsu’, Taiwanese conglomerates or the Korean ‘Chaebol’ have a legacy of CSR analogous to European companies comprising social services, life-term employment, and health care as a consequence of response from the regulatory and institutional environment of business but not merely due to voluntary corporate policies.

In the developing countries, many multinational companies have been the major driving force for the recent surge in CSR activities in these developing nations. For example, campaigns against Nike’s labour practices in its Asian supply chains and Shell’s role in Nigeria had sparked substantial changes toward more responsible CSR practices in MNCs. Further, the domestic companies in the developing countries have contributed to CSR activities such as improvement of the infrastructure of education, health, and transport etc. Likewise, as the example of the Grameen Bank[6], instituted by Nobel Peace Prize winner Muhammad Yunus substantiates, a vital topic on the CSR agenda is the inspiration of small-scale entrepreneurship through micro-credit, and the financial empowerment of women and other disregarded minorities.

CSR IN INDIA

Philanthropy and CSR are not a new concept for India or Indian Companies. CSR in India has traditionally been seen as a philanthropic activity, which was more of a kind of voluntary spend rather than a statutory obligation under any of the statutes. If we look at the Indian heritage, there were three types of philanthropic or charitable activities which were traditionally practised namely Dana, Dakshina and Diksha. Dakshina was one which was given in exchange/return of something; Diksha was something thing which was given for your own enlightenment and Dana was the purest form of charity which was done without expecting something in return. Keeping in view of Indian Tradition, this was an activity which was voluntarily performed by the people without any deliberation. As a consequence of this, there is limited documentation on specific activities related to this concept. Further, the corporates entities in India such as Tata can self-esteem themselves on more than one hundred years of reliable business practices, including far-reaching philanthropic activities and society involvement.[7]

India is the first country in the world to have a statutory compliance requirement on CSR spending whereas, in other countries like UK, France, Germany etc., there have been voluntary guidelines. The Companies Act, 2013 has instituted the idea of CSR under Sec 135 of the Companies Act, 2013, to the forefront and through its disclose-or-explain directive, is promoting greater disclosure and transparency. The Act stipulates that companies which meet a certain set of criteria will have to spend at least 2% of their average profits in the last three years towards CSR activities. Schedule VII of the Act, which lists out the CSR activities, advises communities be the focal point. On the other hand, by conversing a company’s relationship with its stakeholders and assimilating CSR into its core operations, the CSR rules suggest that CSR needs to go beyond communities and beyond the concept of philanthropy. In case, entities are unable to comply with the CSR provisions under the Act, they would be required to give explanations/reasons for not spending the amount on CSR activities. The approach is to ‘comply or explain’. If they fail to do so, they would face action, including a penalty.

CSR under the Companies Act 2013

Some of the key features of CSR under the Companies Act, 2013 have been analyzed under the below subheadings

CSR provisions and applicability

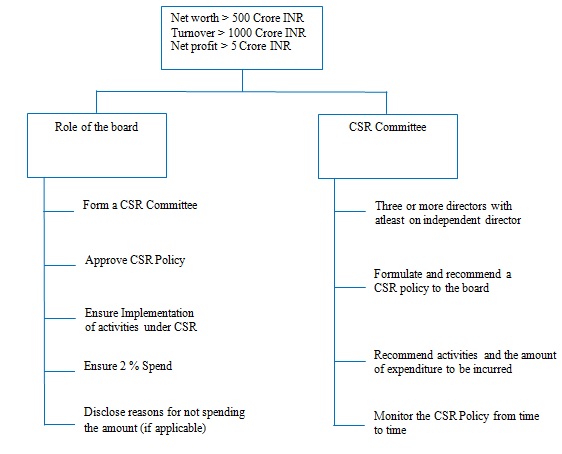

According to Section 135, Companies Act, 2013, the CSR provisions will be applicable to private limited and public limited companies, as well as their holding and subsidiary companies and foreign companies that have offices in India and meets any of the following criteria:

- Company must have a net worth of INR 500 crore of more in any financial year;

- Company must have an annual turnover of INR 1,000 crores or more in any financial year;

- Company must have a net profit of INR 5 crore or more during any financial year.[8]

Companies that meet any of the aforesaid criteria must spend at least two percent (2%) of their average net profits made during the previous three financial years on CSR activities.

An inclusive definition of CSR

While the Companies Act used CSR as a nomenclature without actually defining it, the notified CSR rules have defined the term “CSR” to mean and include but not limited to:

- Projects or programs relating to activities enumerated in the Schedule; or

- Projects or programs relating to activities undertaken by the Board in pursuance of recommendations of the CSR Committee as per the declared CSR policy subject to the condition that such policy covers subjects specified in the Schedule.

This inclusive definition of CSR is of importance as it permits the companies to involve in projects or programs relating to activities enumerated under the Schedule. It also gives flexibility to the companies by permitting them to choose their ideal CSR engagements that are in accordance with the CSR policy.

CSR Committee and Policy

Every qualifying company will be required to constitute a Committee (CSR Committee) of the Board of directors (“Board”) consisting of 3 or more directors, including at least one independent director.[9] The CSR rules 2014, states that an unlisted company and a private company which are not required to appoint an independent director shall constitute a CSR committee without an Independent director.[10] A private company having only two directors shall constitute its CSR committee with two such directors.[11] In the case of a foreign company, the CSR Committee shall consist of at least two persons wherein one person shall be Indian resident and another person shall be nominated by the foreign company.[12]

The CSR Committee shall articulate and endorse to the Board, a CSR policy which shall specify the activity or activities to be undertaken by the company; recommend the amount of expenditure to be incurred on the activities referred and monitor the CSR Policy of the company.[13]The Board shall take into considerations of the suggestions made by the CSR Committee and approve the CSR Policy of the company.[14]

Role of the board and the CSR committee:

Computation of Net profit

Every company incorporated under Companies Act will have to report its net profits accrued during the financial year for the purpose of ascertaining the criteria stated under Section 135(1) of the Companies Act, 2013. There are a distinct set of rules governing the Indian and Foreign Company in this aspect.

(a) Indian Company: The methodology for computation of net profit has been explicitly provided in the CSR Rules. According to the CSR Rules for the determination of the ‘net profit’, of a company profits made by the company from its overseas branches or dividend income received from another Indian company have to be disregarded. Further, the 2% CSR is to be computed as 2% of the average net profits made by the company during the last three financial years.[15] Also, the computation of net profit is in accordance with Sec 198 of the Companies Act, 2013 which is mainly net profit before tax.[16]

(b) Foreign Company: CSR rules states that the net profit of a foreign company incorporated in India shall be determined in conformity with the profit and loss account and balance sheet of a foreign company which will be formulated in accordance with Section 381(1)(a) read with Section 198 of the Companies Act.[17]

Scope Activities under CSR

Schedule VII of Companies Act, 2013, provides a wide spectrum of activities which may be undertaken by the body corporates in India. Apart from the specified activities, the Government may prescribe any other activity which it thinks proper to be included within the ambit of CSR.[18] The activities that can be done by the company to achieve its CSR obligations include

- eradicating extreme hunger and poverty;

- promotion of education;

- promoting gender equality and women empowerment

- reducing child mortality and improving maternal health,

- combating human immuno-deficiency virus, acquired, immune deficiency syndrome, malaria and other diseases

- ensuring environmental sustainability;

- employment enhancing vocational skills;

- social business projects;

- contribution to the Prime Minister’s National Relief Fund or any other fund set up by the Central Government or the State Governments for socio-economic development and relief and funds for the welfare of the Scheduled Castes, the Scheduled Tribes, other backward classes, minorities and women and

- such other matters as may be prescribed by the government of India.[19]

General Circular No. 21/2014 of Ministry of Corporate affairs had clarified that the entries in the Schedule VII have to be interpreted liberally so as to encapsulate the crux of the subjects listed in the said schedule. The items enumerated in Schedule VII of the act are based on broad concepts and expected to cover a wide range of activities. The General circular also provides an elucidatory list of activities that can be included under CSR. In a similar manner, CSR expenditure can be spent on many more activities which are relatable to the ones which are enumerated under Schedule VII.[20]

The Ministry of Corporate Affairs, in order to provide clarity to the execution of CSR, has enumerated the activities which shall not be treated as CSR activities. The following do not constitute as activities falling under CSR:

- Activities undertaken in pursuance of the normal course of business by the company;

- Activities undertaken outside India;

- Activities that are exclusively for the benefit of employees of the company and their families;

- One-off events such as awards/ marathons/ advertisement/ charitable donations/ sponsorships of TV programmes etc. would not be regarded as part of CSR expenditure.

- Expenses incurred by companies for complying with any Act/ Statute of regulations (such as Land Acquisition Act, Labour Laws etc.)

- Contributions made either directly or indirectly to any political parties under Section 182 of Companies Act 2013.[21]

Implementation of CSR

As per the Companies Act, 2013, the activities enumerated in Schedule VII can be executed in the following ways:

- It must be carried out within India, preferably at the local areas and the areas around where the company operates.

- It may be performed as CSR projects or activities or programs which may either be fresh or ongoing;

- It may be carried out with the aid of a registered trust or society, or a charitable company functioning within India which is established by the funding company, its parent, subsidiary or associate company; or which is not established by the funding company, its parent, subsidiary or associate company if it has a proven track record of undertaking similar activities for at least three years;[22] and

- It may be conducted in association with other companies provided that each eligible company is able to report its CSR activities individually.[23]

- It may also use up to 5% of its CSR spending in a financial year for training its own employees/personnel for implementing CSR activities or for developing the required facilities/capacities of their own personnel or implementing agencies.

Reporting

It is mandatory for the companies to publish the CSR report on their company’s official websites annually[24]. The Board of directors of the Company must prepare an annual report on the CSR activities of the company in a separate format specified in the CSR rules. The CSR report, inter alia, must contain a brief overview of the CSR policy, the composition of the CSR committee, average net profit in the preceding three financial years, 2% of the average net profit of the company, the amount of expenditure that was spent on CSR activities and any amount which have left unspent. In the case of a foreign company, the balance sheet failed under sub-clause (b) of Section 381(1) shall contain an annexure regarding report on CSR. If the company fails to spend the minimum required portion of its net profit on CSR activities, the reasons for failing to do so must be mentioned in the Board report.

Penalty for Contravention of CSR provisions

According to Section 134(3)(O) the companies Act 2013, the board of directors need to mandatorily disclose all the relevant information about its Company’s CSR policy and its implementation on an annual basis. Section 134(8) of the Act states that if the company fails to comply with the aforementioned provision, it shall be liable to pay a fine which shall not be less than Rs. 50,000 but may extend to INR 25,00,000. Further, every defaulting officer shall be punishable with an imprisonment for a term, not more than 3 years or with a fine which shall not be less than INR 50,000 but may extend to INR 5,00,000 or with both. This essentially infers that the Act penalizes a company for failure to disclose information about its CSR policy but does not hold them liable for not undertaking CSR activities.

However, Section 450 read with Sec 451 of the Act, which deals with general penalties for contravention of the rules and repeat offences, contains a provision for punishing a company or its officers in case no specific punishment is provided for a particular offence. Sec 450 of the Act states that if a company contravenes with any provisions of the Act or any rules thereunder, the company and any defaulting officer are liable to pay a fine which may extend to INR 10,000 and INR 1,000 per day if the contravention continues after the first fine.

According to Section 451 of the Act, where the defaulter is punished either with fine or with imprisonment and where the identical offence is committed for the second or successive occasions within a period of three years, then, that company and every officer thereof who is in default shall be punishable with twice the amount of fine for such offence in addition to any imprisonment provided for that offence.

FALL OF THE GIANTS: FAILURES TO THE CORPORATE GOVERNANCE

While the market has been super volatile in the current times, the issue before the pandemic also did not make any sky-rocketing performance by the companies. The failure of corporate governance by the most widely known companies in India has shaken the shareholders. The downfall of the major unicorns in the country has ensured that the surviving companies duly follow the corporate governance responsibility and ensure transparency in operations. While the major companies have been complaining of the new legislations under the indirect tax as a cause for their downfall, it is important to highlight over here that the lethargy of the companies in duly following the legislative guidelines cannot be used as an argument to justify their failure of corporate governance. The major giants such as café coffee day, Yes bank, DHFL are some among the few companies which were on the peak in the past but the same companies are on the verge of shut down due to insufficient funds and failure of working.

- FALL OF CAFÉ COFFEE DAY (CCD):

CCD was one of the major coffee giants of India with more than 1500 outlets across the country. It has been in business since the late 19th century and has a history of growing the most authentic coffee beans. While Starbucks was a huge giant of the west, CCD proved to be the one of our country. The company decided to go public in the year 2015 in order to increase the profitability and involve investments from the public but still had major debt toll. While the company was at a surge due to enormous loan and debt, the public offering of shares did not help the firm to change their financial aspects. In the year 2017, the company faced yet another setback where the tax department raided the company and the proprietor had to pay a whooping amount of Rs 2000 Crores to the tax department.

While the company was in heavy debt, the taxes raided from the company worsen the situation. The company was already facing losses in the previous year’s amounting to 50-60 Crores. Thereafter the proprietor due to such heavy setback suddenly disappeared in the year 2019 and was not heard of and thereafter his dead body was founded. The cause of such suicide was the enormous debt on his head and the inability to pay the same to the private lenders. The private equity investors forcing him to buy back the shares or give quick returns on the amount invested burdened the proprietor on another level. While we see rise in the number of stores and multiple people going to such food stores, the debt piling up came out to be strange news for all.

After such whooping loss, the company was sold to Blackstone legal entity in 2019 hoping that the financials of the company can get better, but the same has not been observed until now and this marked a clear learning for the investors to check up the financials of the company before investing. Also the companies were alerted after this incident to show case all the necessary details about the company to the investors. Even though the company went public in 2015, CCD still could not revive to a better position and India lost one of its own major coffee giants due to enormous debts.

- THE YES BANK FIASCO:

YES bank is yet another financial lending institution which worked efficiently until the major blunder happened. In March 2020, the Reserve Bank of India took over the complete control of Yes Bank operations in India. While the bank was formed as a non-bank financial company, it started its full fledged lending operations by the year 2003. The bank had been at the forefront of various corporate organizations that could not secure loans from other banks and was agreeing to the loan requests of major giants in the country without much seeing the financial conditions of the borrowers or the point that he belonged to the defaulter’s category.

The condition or the working capacity of the bank suffered huge setback due to the inability of the bank to raise capital in order to address the losses the bank had to suffer. There had been a huge out flux of deposits by the banks and the investors were also very disregarded because of the inability of the bank to provide for the interest on the assets pledged with the bank. The bank faced huge mis-happening of corporate governance where the loan was providing without checking the financials, the board taking decisions without informing the stakeholders, the promoters being the sole authority to take major decisions.

The RBI took complete control over the bank to ensure that the people who had been associated with it do not face a huge setback and hence had numerous meetings with the board to ask about ways in which the balance of liquidity and debt can be ensured. RBI even came up with the policy of telling investors to invest the bank in order to help the bank raise capital from the public markets. However the same did not prove to be a bug time success for Yes Bank because the investors were reluctant to invest in such banks which are in huge debts. Thereafter RBI was forced to seek the help of central government in order to provide an additional moratorium period on YES bank to ensure the bank comes back to its business some time soon.

- STANDSTILL OF JET AIRWAYS:

Jet Airways is one of the largest airlines of India until 2018 with more than 10 percent market share in the airline industry. But in the year 2019, it faced a huge debt setback and had to carry out its operations due to enormous debts and further the company even did not have enough money to pay their pilots and other employees. The company was in the debt if more than Rs 8000 Crores. There have been various airlines that have gone completely bankrupt such as the Kingfishers, the Deccan airlines, but Jet Airways proved to be in one of these lists shook the airline market. The major factor responsible for such downfall is the corrupt practices of its chairman and his lethargic attitude towards the fulfillment of corporate governance criteria.

The chairman and his family had the entire stake of the airline and as already discussed when the board is under the influence of the promoter, then the corporate malfunctions tend to happen because they have the power and capability to take decisions that profit them. The promoters of Jet Airways were also negligent in taking various decisions and majorly this was the reasons that two most prominent independent directors of Jet Airways resigned in the year 2018. While the TATA’s wanted to save the country’s airline and offered to invest in the company but the same was denied by the board giving insufficient reasons. The sole decisions were being made in the company for the welfare of promoters rather than the stake-holders.

Corporate governance ensures that the shareholders and the stakeholders are in the same loop as the promoters and the directors and that every decision should be well informed to every personnel of the company. The chairman of the company worked in such lethargic manner that he had the capability to deny the basic salaries to its employees after completion of their work and even denied them job security. The corporate social responsibility followed by the company was negligible and the enormous debt amount forced the employees to leave the job because even with the intervention of court, the company was unable to pay the basic to their employees.

GLOBAL PERSPECTIVE OF CORPORATE GOVERNANCE

- WELLS FARGO SCANDAL:

Wells Fargo is the major financial services company which has its headquarters based in the city of California, US. The banking service was known worldwide as the one who avoids committing any dumb mistakes that other financial lending institutions tend to do and was always appreciated to have been customer support system and cordial relations with the stakeholders. The institution was further always appreciated for the active engagement with the customers and an increase in the sales culture. The main mistake which led to the downfall of the company is the malpractices by their own employees who have been opening various bank accounts of the customers and have been selling debit and credit cards to the already existing customers without even their knowledge. There were also circumstances observed where the signatures of the customers were forged in order to sell their financial services to the customer.

There were more than five thousand employees who had been a part of this scandal and the bank has the liability to pay off more than $3 Million to the customers whose accounts have been hacked and money manipulated. It was highlighted in various reports that the heavy targets imposed by the bank of the employees surged the malpractices because of the pressure of opening up accounts. In the year 2016, the bank took off the liability by paying more than $180 million to the regulators who filed multiple law suits against the banks.

The main cause of this scandal was the inherent sales pressure by the banking sector on their employees with such altruistic sales target that they will have to resort to unfair means in order to complete the same and save their job. Further it is of utmost importance to highlight here that while the employees were excessively dealing in the sales of credit cards, etc, the successful corporate governance in the form of audit committees; the risk management task force would have highlighted the discrepancies if any and would have highlighted the unscrupulous practices. But due to lethargy in enforcing the corporate governance mechanism, the banking company had to face a lot of turmoil.

- COLLAPSE OF CARILLION:

Carillion is one of the leading construction company of the United Kingdom and has always believed in making a better tomorrow for all. The company was the most renowned one and had multiple projects handing varying from Canada to Iran. But in the year 2018, after a sudden financial failure, the company became incapable in performing any of the given projects. The company in itself had more than forty thousand employees and revenue more than 4 billion Euros for each financial year. While with the downfall of the company, not just the practices came to an end, the small employees and their salaries were also put up at stake.

The major problem of the collapse was the low profit margin of the company and an increase in debts where the board of the company was unable to take up this issue and manage the risk factor. The financial council of the UK looked into the audits of the company in previous years which clearly did not give any red flags highlighting the financial unsoundness of the company. The cash flow to the company was very meager and majorly the money was spent on the acquisition of raw materials and distributing services. The company has been major involved in relying on additional contracts to minimize the losses but the same did not work well for the company.

The additional problem highlighted in this case if the inability of the board to decrease the debt and additionally increasing the debt ratio of the company by taking up different contracts. Corporate governance with the help of various stakeholders ensures that the debt to equity ratio is balances and excessive debt should be dealt in an efficient yet swift manner. Without an efficient check mechanism, even the big giants cannot be saved and eventually collapse and hence it is of major importance to highlight the concept of corporate governance in the company to ensure smooth and healthy functioning.

PM CARES: UNDER THE AMBIT OF CORPORATE SOCIAL RESPONSIBILITY?

While the pandemic was at the surge in India, the central government came up with the initiative of PM cares fund which basically invited help in monetary manner from various people across the world that shall help the government in combating the virus. The prime minister of our country is the chairman of the fund. Furthermore, the amount donated by the people is not disclosed by the government and the government claimed it to be private fund where the government shall not be accountable to give any public disclosure. Even though in the recent times, the fund has been subjected to various questions due to lack of transparency and the accountability, there have been various companies who have been donating their bit in the name of corporate social responsibility these funds.

Ministry Of Corporate affirs circular dated April 10th, 2020

The Ministry of Corporate Affairs as per the circular dated 10th April,2020 answered various question related to CSR and the PM cares fund where they said the fund is under the ambit of CSR initiative by the companies. Moreover if the companies have donated their bit to the state relief funds, then the same shall not be considered as CSR as the state initiative is not included in the Schedule VII of the Companies Act, 2013. The contributions that have been made to the national as well as the state disaster management authority shall be covered under the ambit of CSR. The circular further highlights that it is the moral obligation of the companies to pay wages to their employees and helping the staff in the lockdown period is the moral duty of the company and the same not to be included under CSR. The circular highlighted that the ex-gratia payment in addition to the wages if paid to the employees or the daily wage workers, then the same can come under the ambit of CSR.

While the circular initiated the payments from the companies in the name of CSR, the denial that the contributions to the state relief funds was not given any appropriate reason. Also as per the researcher, the ministry of corporate affairs should have mandated on the companies to provide for adequate salaries to the employees as a measure under CSR rather than considering as a moral duty because until and unless the legal compliances are placed, the companies do not think about the stakeholders at large. Further the need of the hour to combat the pandemic in our country would be to help the people on the ground level rather than donating to such organizations.

The basic help from the companies to provide for insurance covers to the employees, helping the employees family who tested positive in a financial manner, helping the employees receive mentally when they lose their loved ones, giving bit temporary paid leaves so that people when they test positive, acquiring basic medicines and other needs for their employees can prove to be some highly helpful CSR initiatives that the companies can perform. It is always better to know where the money of the organization is spent and whether it is spent for the upliftment of the people rather than giving up to the government organizations that are not even transparent in their actions.

CONCLUSION

From the above analysis, it is evident that CSR is a noble initiative wherein the corporate entities which reap the benefits of resources available at the society helps to fill the gap of socio-economic inequality prevalent in the country and address the problems faced by the society at large. In most of the countries, CSR activities was a voluntary obligation by the companies or by regulatory. India is the first country in the world to have a mandatory statutory compliance requirement on CSR spending, which was incorporated under Section 135 of the Companies Act, 2013 and has come into effect from 1 April 2014. As a consequence of this, various companies have taken on extensive projects addressing the socio-economic concerns and have supplemented the government’s efforts of sustainable development and engage the corporate world with the country’s development.

However, there are certain lacunas like; there was no tax clarity on the CSR spending, ambiguity on the computation of financial accounts of foreign companies, an absence of clarity on the regulations of CSR vis-a-vis foreign contribution. Even though there are certain lacunas, they should not be permitted to become an obstacle in implementing the true spirit of CSR. Thus, the government and corporate entities must mutually work together for an effective implementation and addressing their concerns.

BIBLIOGRAPHY

STATUTES

- The Companies Act, 1956

- The Companies Act, 2013

RULES

- Companies (Accounts) Rules, 2014

- Companies (Corporate Social Responsibility) Rules, 2014

SCHEEDULES

- Schedule VII of Companies Act, 2013

NOTIFICATIONS

- Ministry of Corporate Affairs. Schedule VII. [GSR 130 E] dated 27th Feb, 2014.

- Ministry of Corporate Affairs. Corrigenda to Schedule VII. [GSR 261 (E)] dated 31st Mar, 2014.

- Ministry of Corporate Affairs. Enforcement Notification S.O. 902(E) dated 26th Mar 2014.

- Ministry of Corporate Affairs. Further Amendment to Schedule VII. [GSR 568 (E)] dated 06th Aug, 2014.

- Ministry of Corporate Affairs. Companies (Corporate Social Responsibility Policy) Amendment Rules, 2014. [GSR 644(E)] dated 12th Sep, 2014.

- Ministry of Corporate Affairs. Further Amendments to Schedule VII. [GSR 74 (E)] dated 24th Oct 2014.

- Ministry of Corporate Affairs. Companies (Corporate Social Responsibility Policy) Amendment Rules, 2015 [GSR 43(E)] dated 19th Jan, 2015.

- Ministry of Corporate Affairs. Companies (Corporate Social Responsibility Policy) Amendment Rules, 2016. [GSR 540 (E)] dated 23rd May, 2016.

- Ministry of Corporate Affairs. Exemption to Specified IFSC Private Company [GSR 09(E)] dated 04th Jan, 2017.

- Ministry of Corporate Affairs. Exemption to Specified IFSC Public Company [GSR 08(E)] dated 04th Jan, 2017.

CIRCULARS

- Ministry of Corporate Affairs. Clarifications with regard to provisions of Corporate Social Responsibility under Section 135 of Companies Act,2013.General Circular No. 21/2014 bearing No. 05/01/2014-CSR. (Issued on 18th June, 2014)

- Ministry of Corporate Affairs. Clarification with regard to the provisions of Corporate Social Responsibility (CSR) under Section 135 of Companies Act, 2013. General Circular No. 36/2014 bearing No. 05/01/2014-CSR. (Issued on 17th Sep, 2014)

- Ministry of Corporate Affairs. Constitution of a high level committee to suggest measures for improved monitoring for the implementation of Corporate Social Responsibility policies by the companies under Section 135 of Companies Act, 2013. General Circular No. 01/2015 bearing No. 05/09/2014-CSR. (Issued on 3rd Feb, 2015)

- Ministry of Corporate Affairs. Frequently Asked Questions (FAQs) with regard to Corporate Social Responsibility under Section 135 of Companies Act,2013.General Circular No. 01/2016 bearing No. 05/19/2015-CSR. (Issued on 12th January, 2016)

- Ministry of Corporate Affairs. Clarifications with regard to provisions of Corporate Social Responsibility under Section 135 of Companies Act,2013.General Circular No. 05/2016 bearing No. 05/01/2014-CSR. (Issued on 16th May, 2016)

BOOKS

- A Ramaiya, Gudie to Companies Act: Providing Guidance on the Companies Act, 2013 (18th edition, LexisNexis 2015)

- Taxmann’s, A Comparative Study of Companies Act 2013 and Companies Act 1956

(Taxman Publication Pvt. Ltd., 2013 edition)

ARTICLES

- Elankumaran, S., Seal, R., & Hashmi, A. 2005. Transcending Transformation: Enlightening Endeavours at Tata Steel. Journal of Business Ethics, 59(1): 109-119.

- Brammer, S., & Pavelin, S. 2005. Corporate community contributions in the United Kingdom and the United States. Journal of Business Ethics, 56: 15-26.

- EC, Green Paper, Promoting a European Framework for Corporate Social Responsibility, COM (2001) 366 (18/07/2001), para 20.

- CII and PWC. 2013. Handbook on Corporate Social Responsibility in India. Available at: https://www.pwc.in/assets/pdfs/publications/2013/handbook-on-corporate-social-responsibility-in-india.pdf

WEB SITES

References.

[1] Press Release dated 27th February 2014; http://pib.nic.in/newsite/erelease.aspx?relid=104293

[2]Schedule VII deals with the activities which may be included by companies in their CSR policies

[3] EC, Green Paper, Promoting a European Framework for Corporate Social Responsibility, COM (2001) 366 (18/07/2001), para 20, available at http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52001DC0366&from=EN. Accessed on 21 March 2017

[4] http://www.unido.org/csr/o72054.html. Accessed on 21 March 2017

[5] Brammer, S., & Pavelin, S. 2005. Corporate community contributions in the United Kingdom and the United States. Journal of Business Ethics, 56: 15-26

[6] http://www.grameen-bank.net/

[7] Elankumaran, S., Seal, R., & Hashmi, A. 2005. Transcending Transformation: Enlightening Endeavours at Tata Steel. Journal of Business Ethics, 59(1): 109-119

[8] “Any financial year” referred under Sub-Section (1) of Section 135 of the Act read with Rule 3(2) of Companies CSR Rule, 2014, implies ‘any of the three previous financial years’

[9] Section 135(1) of the Companies Act

[10] Pursuant to Section 149 of the Companies Act, 2013 and Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 5(1(i))

[11] Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 5(1(ii))

[12] Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 5(1(iii))

[13] Section 135 (3) of the Companies Act

[14] Section 135 (4) of the Companies Act

[15] Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 2(1)(f)

[16] Frequently Asked Questions (FAQs) with regard to Corporate Social Responsibility under Section 135 of Companies Act,2013.General Circular No. 01/2016 bearing No. 05/19/2015-CSR. (Issued on 12th January, 2016)

[17] Section 198 of the Companies Act, 2013 deals with calculation of profits; Companies (Corporate Social Responsibility Policy) Rules, 2014, Proviso to Rule 2(1)

[18] The Companies Act, 2013, Schedule VII

[19] The Companies Act, 2013, Schedule VII

[20] Clarifications with regard to provisions of Corporate Social Responsibility under Section 135 of Companies Act,2013.General Circular No. 21/2014 bearing No. 05/01/2014-CSR. (Issued on 18th June, 2014)

[21]General Circular No. 21/2014, Ministry of Corporate Affairs, (June 18, 2014), http://www.mca.gov.in/Ministry/pdf/General_Circular_21_2014.pdf

[22] Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 4(2); See Ministry of Corporate Affairs, Notification Companies (Corporate Social Responsibility Policy) Amendment Rules, 2016. [GSR 540 (E)] dated 23rd May, 2016

[23] Companies (Corporate Social Responsibility Policy) Rules, 2014; Rule 4(3); See Ministry of Corporate Affairs, Notification Companies (Corporate Social Responsibility Policy) Amendment Rules, 2016. [GSR 540 (E)] dated 23rd May, 2016

[24]Companies (Corporate Social Responsibility Policy) Rules, 2014, Rule 8 and 9

Allow notifications

Allow notifications