This article has been written by Nisha Sharma pursuing a Startup Generalist & Virtual Assistant Training Program from Skill Arbitrage.

This article has been edited and published by Shashwat Kaushik.

Table of Contents

Introduction

Indeed, it is essential for any e-commerce business to come up with a good marketing strategy for their aspiration to grow and prosper in this competitive digital environment. This well-designed plan can not just bring potential customers but can also retain them as lifetime buyers, leading to continuous growth and increased profitability. This article will look at the key elements and best practices needed to create a successful e-commerce marketing plan. There are going to be actionable insights and useful tips on how to optimise the website for search engines, make use of social media platforms, and run personalised email campaigns in order to enhance the online presence, reach out to the target audience, and increase sales.

This article will discuss why it is important to use analytics to understand customer behaviour and preferences and how this can be used for targeted marketing. We are going to learn how engaging content can help customers connect with the brand emotionally, which in turn increases their trust and creates loyalty.

We will also elaborate on how important mobile optimisation is as well as strategies for ensuring a seamless shopping process on any device. Regardless of whether one is a beginner or wants to improve what is already there, this reference guides through all the intricacies involved in e-commerce promotion while getting one’s venture ready for sustainable growth.

By the end of this article, you will have a comprehensive understanding of the essential elements that make up a robust e-commerce marketing strategy and be equipped with the tools and knowledge needed to implement these strategies effectively. Let’s dive in and unlock the potential of your online business.

Before we conclude this article, we shall find out all the key components that form a strong strategy used in e-commerce marketing by gaining enough tools and information to successfully utilise them. Let’s get started to unleash the capabilities of your online business, if you have one.

What is e-commerce marketing

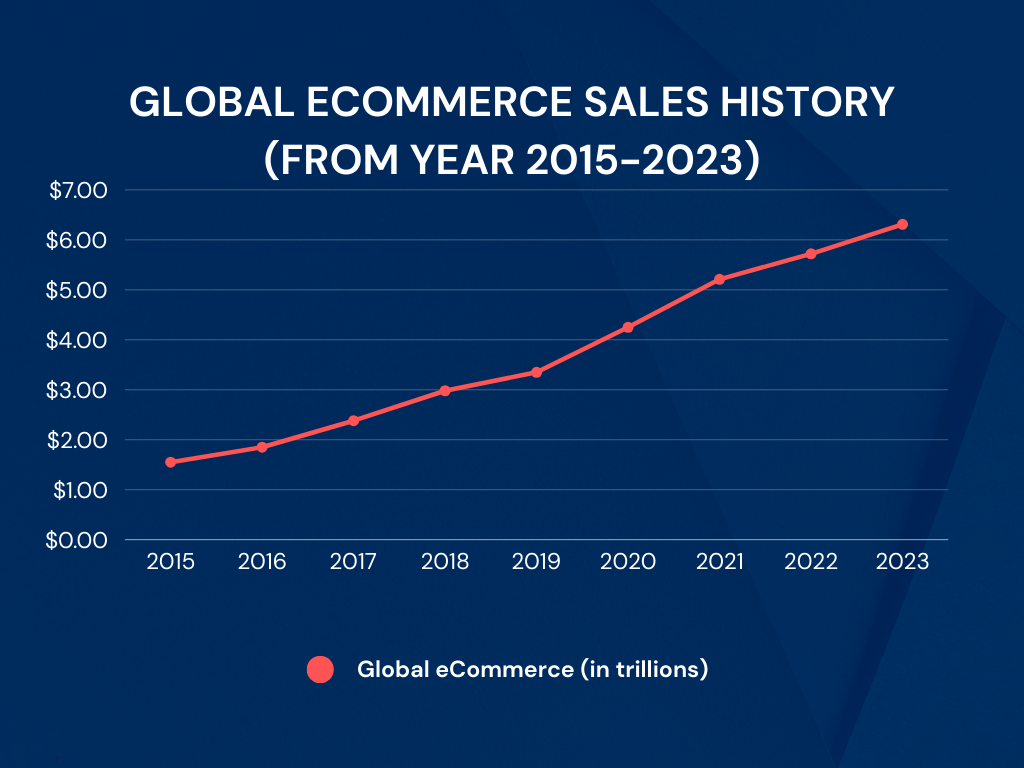

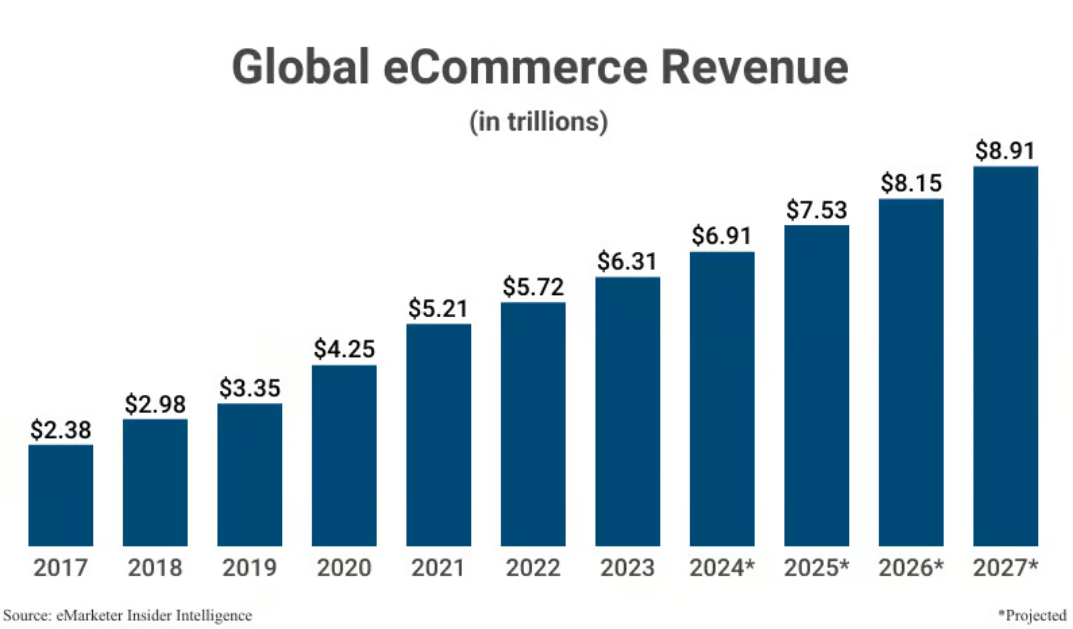

Graphs showing global retail e-commerce sales in 2023 totaled $6.31 trillion, up 10.4% YoY

E-commerce marketing is a dynamic and multifaceted realm within the digital landscape, encompassing a myriad of strategies aimed at driving traffic to online stores, fostering conversions, and forging enduring customer loyalty. In essence, its purpose is to transform passive product observers into passionate product advocates or, in some cases, brand ambassadors.

The tactics employed in e-commerce marketing are as diverse as the channels through which they are executed. Search engine optimisation (SEO), with its focus on enhancing a website’s visibility in search engine results pages (SERPs), plays a crucial role in attracting organic traffic. Content marketing, through the creation and distribution of valuable, engaging, and informative content, aims to capture the attention of potential customers and nurture their interest in the brand.

Social media marketing leverages the power of various social media platforms to connect with customers, build relationships, and promote products or services. Email marketing, with its ability to deliver personalised messages directly to the inboxes of subscribers, offers a direct line of communication with customers and is highly effective in driving conversions.

Pay-per-click (PPC) advertising allows e-commerce businesses to place targeted ads on search engines or other websites, paying only when a user clicks on the ad. Affiliate marketing involves partnering with other websites or individuals to promote a brand’s products or services in exchange for a commission on each sale generated.

Influencer marketing, by tapping into the influence of popular social media figures, helps brands reach a wider audience and build credibility. These promotional techniques, when used singly or in combination, can significantly impact e-commerce marketing campaigns.

The ultimate objectives of e-commerce marketing extend beyond mere traffic generation. They encompass enhancing customer interaction, fostering engagement, and, ultimately, driving sales and business expansion within the digital ecosystem. By aligning marketing strategies with these objectives, e-commerce businesses can unlock their full potential and achieve sustainable growth in the competitive online marketplace.

What’s the difference between e-commerce and digital marketing

The following table explains briefly the nitty-gritty of e-commerce and digital marketing and how they are intertwined and yet different from one another.

| E-commerceE-commerce refers to the buying and selling of products or services online and involves the transfer of money and data to complete the financial transaction electronically. E-commerce businesses take different forms and sizes. When it comes to forms, they can be as follows:Business-to-Consumer (B2C): A transaction between a business and a consumer. A typical example is buying shoes from an online retailer like Walmart, Target, or Sephora. Business-to-Business (B2B): Businesses mainly transact with each other online. This includes companies like Hubspot, Slack, and Microsoft. Consumer-to-Consumer (C2C): Sales between buyers and sellers on platforms like eBay and Amazon are involved. One example is selling things on Facebook Marketplace or Craigslist. Direct-to-Consumer (DTC): Examples of this are companies that offer subscription-based services such as Netflix or Dollar Shave Club. Consumer-to-Business (C2B): Business buyers buy products or services from individual customers who are in a retail business, like photographers who in turn sell stock photos on iStock or influencers offering marketing services. Business-to-Government (B2G): These are transactions between enterprises on the internet and governments, such as selling legal software to municipal councils or even social security packages to the same groups. Consumer-to-Government (C2G): In order to enable online payment using government websites, e.g., utility firms, there are cases where firms sell their products or services directly to the government. In terms of size, an e-commerce business can be either an enterprise, mid-market, small business, or startup. The buyers of the e-commerce business enjoy the benefits of product accessibility anytime, flexibility in terms of location, a wide range of choices, and speedy purchase. The sellers bear low costs, low or no overhead, no excess stocks, keep up with the current trends, and low cost promotion. | Digital marketingDigital marketing is the act of promoting and advertising a brand with the aim of creating a nexus between the offerings of their products or services and the demands of prospective customers.The process of digital marketing includes:Set goals. Draw up a budget to create a timetable. Investigate the audience. Make a plan for every channel.Put it into action and check for effectiveness.Make adjustments if necessary. Types of Digital Marketing:Search Engine OptimizationContent MarketingSocial Media MarketingEmail MarketingMobile MarketingPaid Media PromotionAffiliate Marketing Benefits of Digital Marketing:Assist brands in reaching their target audience with the right message in a timely manner. Systematic and planned targeting leads to increased brand awareness and greater customer engagement. Consistent publishing of relevant content frequently helps in speedy brand expansion. maximises audience reach. Personalised branding through social media and email marketing. Multiple channel options at the same time. |

What is an e-commerce marketing strategy

Global e-commerce sales are expected to reach $6.9 trillion in the year 2024 (an increase of 9.56% from total e-commerce retail sales of $6.31 trillion in the year 2023), and the same is projected to reach $8.91 trillion in the year 2027.

With the focus on the above graph, we can reflect that this data would not be possible if there had not been a strong marketing strategy behind every e-commerce business.

So, what is an e-commerce marketing strategy?

The strategy that helps the e-commerce business promote their brand to gain recognition, reachout, and retention, resulting in selling products and services online by adopting different digital marketing tactics, is known as e-commerce marketing strategy. Hence, an effective e-commerce marketing strategy aims at drawing in prospective customers, turning them into buyers, and holding them in order to thrive in the marketplace. In brief, an e-commerce marketing strategy integrates some digital methods to enhance sales done online.

Briefing a few tactics: Search Engine Optimization (SEO) entails optimising the site so that it ranks higher and becomes more visible in search results. Content marketing involves initiating valuable information, such as blog posts, videos, or even infographics, so as to attract viewers. Social media marketing is promoting and selling products through social media platforms like Facebook, Instagram, Twitter and Pinterest for promotion purposes and to attract visitors. In email marketing, emails are sent to targeted audiences, whether they contain new products or special offers to encourage customers to shop again. In Paid Promotion, Pay-Per-Click (PPC) ad uses sponsored content that is seen by more people. Affiliate marketing involves working with associates who advertise the goods, and influencer marketing aims to increase sales by relying on people who direct others to merchandise.

We are going to elaborate on the above in addition to a few more in the article.

Benefits of implementing an e-commerce marketing strategy

When companies implement an e-commerce marketing strategy, they enjoy so many benefits.

- There is the possibility of reaching out to many people at once through the internet and the ability to capture new prospects globally. This can be done via Search Engine Optimisation (SEO), which helps in increasing one’s ranking on the search engine results page (SERP), hence attracting more visitors who are not paid for, i.e., organic visitors.

- Assists advertisers target their message more specifically. Tools such as email marketing, social media advertising, and pay-per-click (PPC) ads, among others, enable businesses to make their communication appeal to different groups, increasing their participation and conversion rates.

- It generates quantifiable outcomes and analytics. While e-commerce platforms and marketing tools provide information about consumer behaviour, campaign outcomes, and purchasing patterns, such data helps companies rethink their approaches by pinpointing where they may have gone off track through advertising or other modes of promotion, thus enabling them to make more informed decisions aimed at raising their returns on investments (ROI).

- Improving the customer experience is one of the key benefits of a good e-commerce marketing strategy. Through delivering individualized suggestions, seamless navigation, and prompt and responsive feedback, businesses are able to gain trust and confidence from customers, resulting in repeat purchases and further brand advocacy.

- Geography does not confine e-commerce companies from scaling and being flexible in their online business. By adapting e-commerce marketing plans to meet different markets, products, or even lifestyles, this guarantees that there will be continuous growth that sustains the enterprise in light of changing currents within the internet arena.

Creating time-tested, strong marketing strategies for e-commerce success

There is a huge inquisitiveness in people to learn individual marketing strategies, but they fail to develop a coherent plan without realizing that cohesiveness among several strategies helps to achieve continuous results.

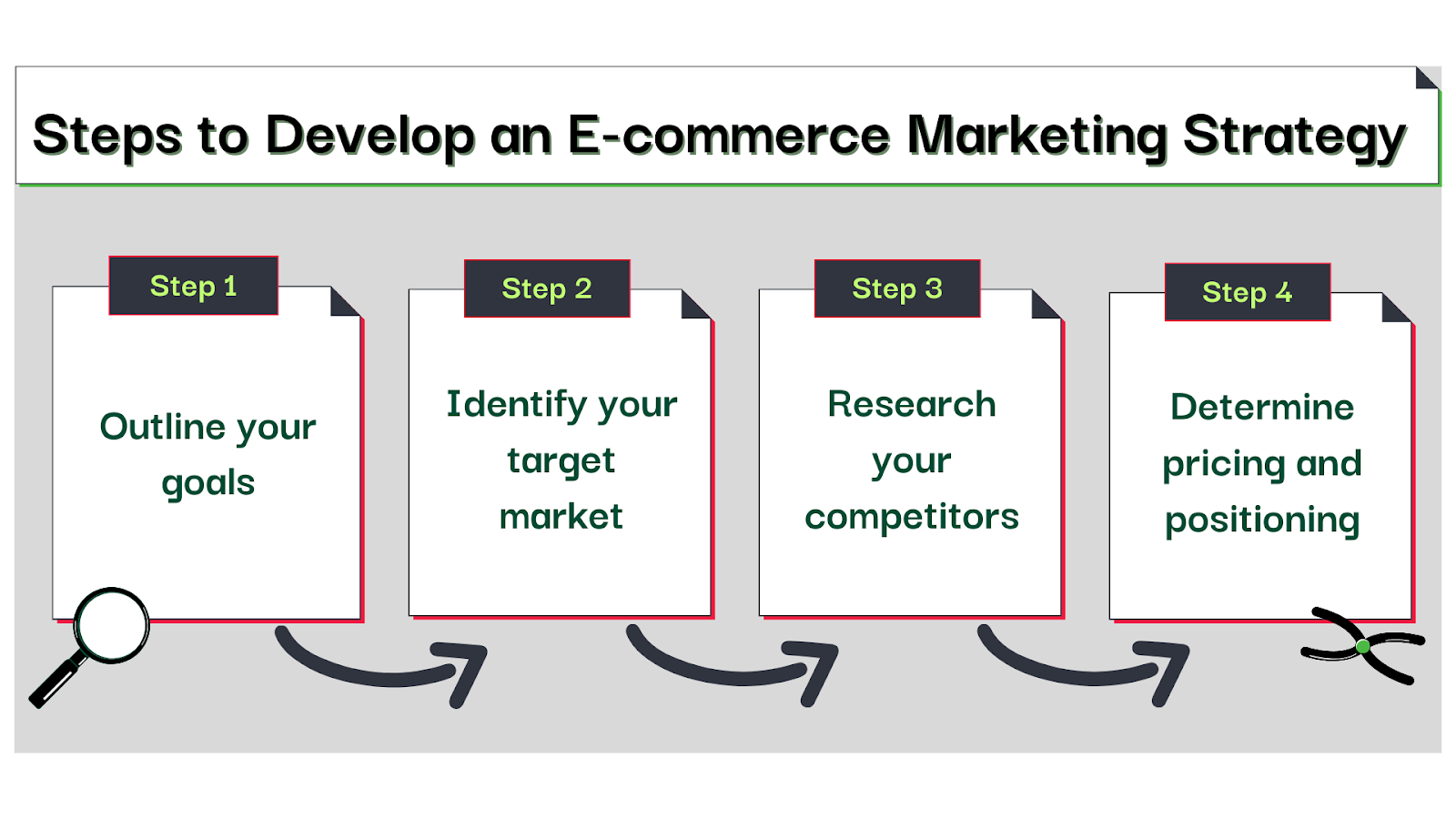

Follow these four steps to develop an e-commerce marketing strategy

- Outline your goals. Identify broad one-year goals, such as increasing site traffic, doubling return visits, or product line expansion. Be specific about your goals, e.g., 1,000 visits a month.

- Identify your target market. Specify the demographics of your desired customers, using age, gender, location, income, and interests. If you have an audience, use surveys. Otherwise, use research to identify their characteristics.

- Research your competitors. Examine websites of competitors, product details, and their marketing strategies. Employ Ahrefs SEO tool to identify their sources of traffic. To avoid being left behind due to market fluctuations, ensure that you monitor the activities of your competitors.

- Determine pricing and positioning. Ensure your prices align with what your ideal customers are willing to pay in order to prevent them from considering you to be too expensive. Place your products in the right position based on information about your rivals.

Improve your website’s visibility through robust SEO

A report by Backlinko says that the #1 organic result is 10x more likely to receive a click compared to a page in the #10 spot, and the below graph demonstrates that SEO is the highest-converting e-commerce traffic channel.

Considering SEO to boost online visibility is an enriching marketing strategy for e-commerce. Around 43% of e-commerce traffic comes from organic Google search results. Below are some steps that can be followed in order to make use of SEO to increase the online visibility of an e-commerce site and boost its traffic.

Keyword research

- Try tools like Keyword Magic Tool from SEMrush, Keyword Generator from Ahrefs, Google AdWords Keyword Planner, and more in your keyword research.

- Pay attention to long-tail keywords that describe your products.

- Aim for keywords that can bring in good leads while being less competitive.

On-page SEO

- There should be a unique title tag as well as a meta description for every single product page.

- The product descriptions should be detailed, keyword-rich, and free from plagiarism.

- Ensure that the URLs are keyword-rich and without numbers or irrelevant characters.

Technical SEO

- Increase the speed of your website in order to provide a better user experience and enhance its search ranking.

- Ensure that the site is available across all platforms with responsive design and is mobile-friendly.

- Install an SSL certificate (HTTPS) to protect your website.

Content marketing

- Ensure having a section for blogs and articles that are optimized with keywords.

- Exploit the benefits of including buying guides, product comparisons, and how-to tutorials.

- Let your visitors leave reviews and ratings for your products.

Link building

Image by Parveender Lamba from Pixabay

- You can make use of internal links to facilitate navigation on the site and distribute page rank.

- Guest blogging, influencer marketing, and partnerships help in acquiring backlinks.

Local SEO

- Claim and enhance your Google My Business listing.

- Motivate clients to give ratings.

- Apply local keywords to your content for it’s visibility on the SERP.

Analytics and monitoring

- Utilise Google Analytics and Google Search Console in order to maintain track of the performances.

- Observe and act on the keyword rankings, traffic sources, and user behavior.

- Constantly optimize your SEO strategy based on data.

Social media integration

- Adding social media buttons to every product page encourages easy sharing of product information.

- Encouraging customers to share their experiences with the products creates user-generated content, which enhances SEO.

Utilise these SEO strategies to enhance online visibility, attract more organic traffic, and eventually increase sales on your e-commerce website.

Get involved through content marketing

Content marketing is prevalently used in e-commerce businesses to attract, engage with, and retain customers. Content like blogs, articles, product descriptions, videos, podcasts, and many more aims to educate people about the product or services, create brand recognition, promote consumer interaction, and raise money for the business. There are several key techniques for a good content marketing strategy.

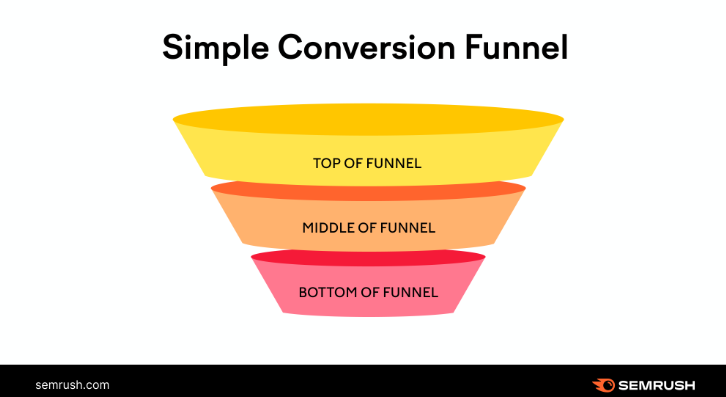

Customise content to Sales Funnel Stages

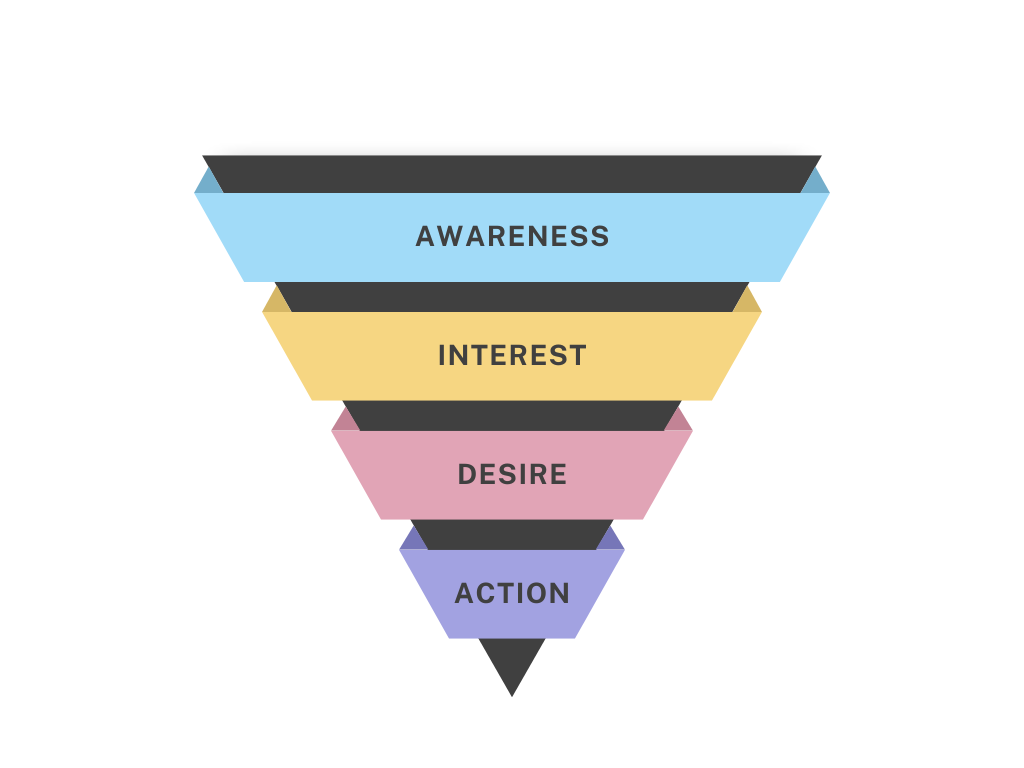

- TOFU means the starting point for sales experience. In this stage, sellers provide information about their goods to potential customers by means of blog posts and videos that are educational. At least they try to make people interested in what they offer before buying it later.

- According to MOFU, sellers should provide systematic product comparisons and detailed case studies so that buyers may evaluate their products without any problems.

- A call-to-action can encourage people to buy products at BOFU, which is often the last but not least stage in converting visitors into customers who make purchases online.

Publish buying guides and FAQs

- Develop comprehensive buying guides to enable shoppers to make purchases wisely.

- Include frequently asked questions (FAQs) to build trust and credibility.

Videos as favourite fontent

- Video content is the favourite of the content types among the audience, as 52% of the marketers acknowledge video gets the best ROI.

- Features and benefits can be shown via product demonstrations and instructional videos.

- Utilise customer feedback and recommendation videos to build trust.

- Use live streaming and sharing on social media to engage with real time audience.

- Share footage from behind the scenes and promote content that is user generated.

- Develop seasonal campaigns and revise strategies as per the performance.

Create and embed interactive content

- Use infographics, e-books, newsletters, whitepapers, case studies, and more to create dynamic and memorable content to boost user participation as well as brand loyalty.

- Use augmented reality in your content to provide an impressive visual experience with the products.

- Use quizzes, surveys, and interactive videos to increase customer participation.

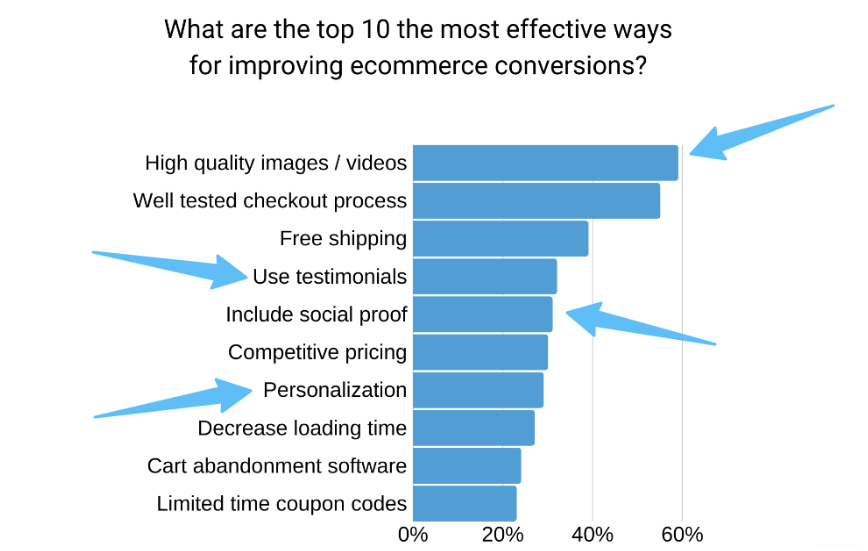

- Social proof can be used as an important tool to gain trust of prospects.

Provide comparative analysis

- Render comparison pages so that potential buyers compare your products with competitors.

- Emphasise distinctive advantages to help people make correct choices.

- Develop trust and loyalty through open and impartial comparisons that sway customers towards buying your products.

Encourage involvement of different stakeholders

- Conduct live chats through social channels like Instagram, Facebook, YouTube, etc. to generate awareness about the brand and product(s).

- Conduct podcasts and webinars talking about the product or service, its benefits, and how it can add value to consumers’ lives.

- Providing original content continually can attract new visitors, serve as value additions to the existing ones, and keep them engaged for retention and repeat purchases.

- Brainstorming with the team to discuss the strategy of the content can enhance the quality of the content being served.

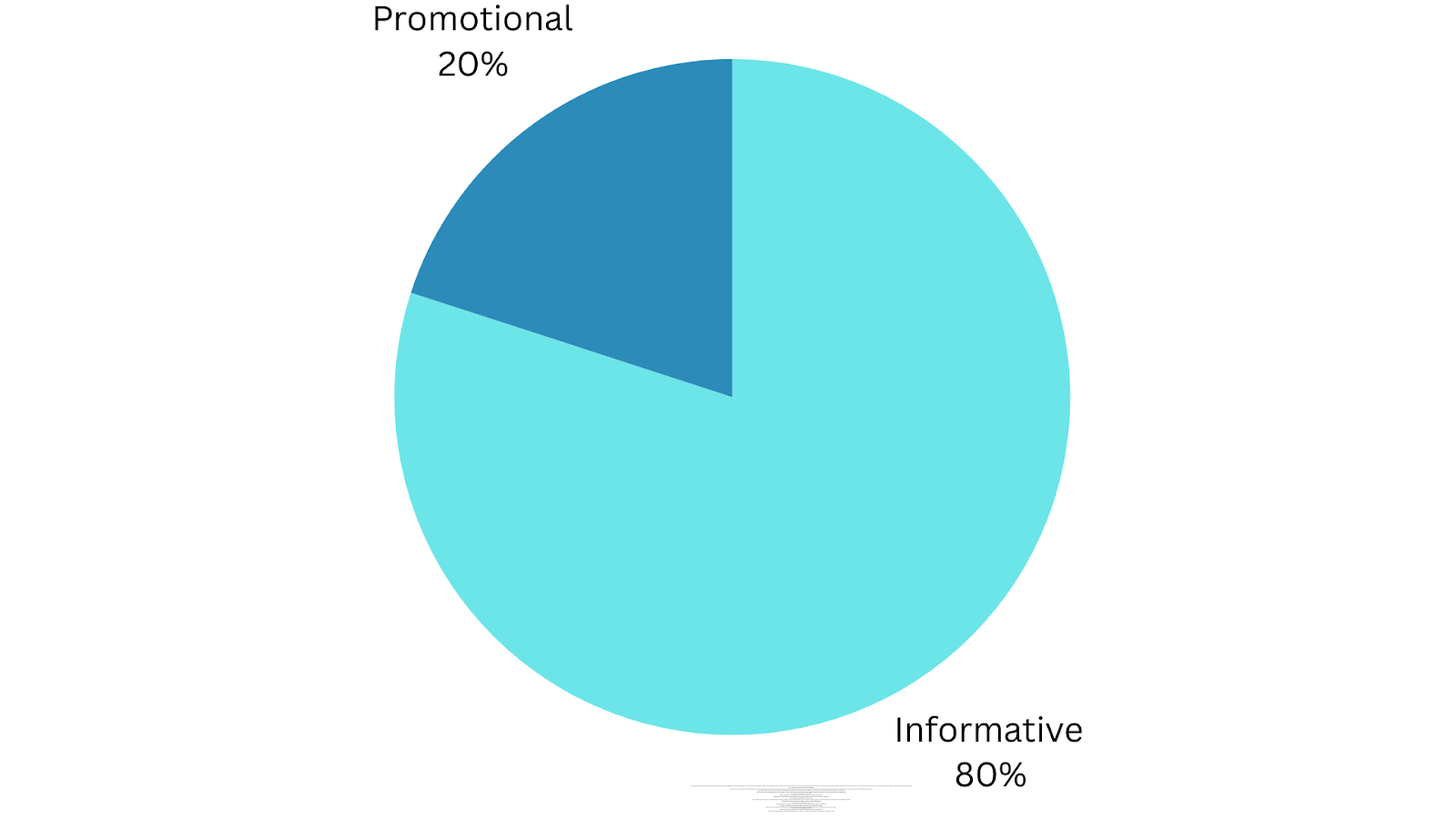

Pareto’s 80/20 rule leads us to the wisdom that 80% informative and 20% promotional content can help in creating relevant, intriguing, and unique content.

- User feedback tools can be used to collect questions, thoughts, and topics from your audience. Heatmap tools can be used to identify the behaviour of visitors in different parts of your website and create content accordingly to catch their interest.

Implementing such content marketing strategies can help e-commerce businesses generate impressions that can be long lasting for them in terms of results in different forms.

Harness the power of social media marketing

Image by Gerd Altmann from Pixabay

Leveraging social media marketing as an e-commerce marketing strategy can significantly enhance your online presence, engage customers and drive sales. Here’s how you can effectively use social media marketing for your e-commerce business:

Choose the Right Channel

- Understand what online preferences and behaviors are typical for the people you want to reach.

- Consider using media such as Facebook, Instagram, Pinterest and TikTok, each of which has strengths in its own way.

- Instagram really shines when it comes to visual content but Pinterest is great for using product pins to attract traffic.

Generating engaging content

- Product features are put on the spot with appealing explainer videos and images of high quality.

- One good way to create trust among the members of the community is by driving people to come up with their own content.

- For instant interaction and promotions, make use of Instagram Stories and Facebook Live.

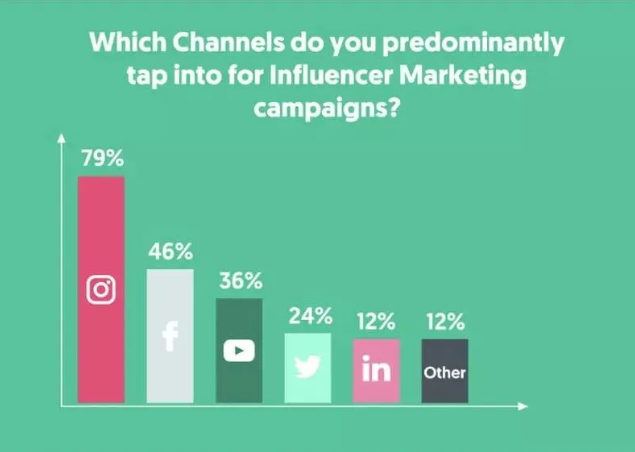

Utilise influencer marketing

The Influencer Marketing Benchmark Report 2024 says that more than 85% of marketers find influencer marketing effective.

- Collaborate with influencers who share the same principles as your brand.

- Leverage the power of influencers when trying to make the visibility and credibility of products better recognised.

- Ensure an authentic and uncontrived feel for the influencer’s recommendations.

Run targeted ads

- Customise audiences by employing demographics, interests, and behaviours.

- Devise retargeting strategies aimed at visitors and users of the website content.

- Send targeted product reminders to escalate sales.

Engage with your audience

- Give and respond to feedback, comments, and messages to make connections strong and grow community.

- In order to maintain active followers, create interactive content such as polls, quizzes, or contests.

Offer exclusive promotions

- Offer some special discounts or promotions for your social media followers.

- Announce some flash sales so as to encourage immediate purchases.

Analyze and optimise

- Use social media analytics tools to track engagement, reach, and conversion metrics.

- Analyse top-performing content to continuously improve strategy.

- Develop a posting content calendar that aligns with audience interests and A/B test new ad formats.

One can improve the awareness focused on his or her e-commerce business, create a personal touch aimed at customers’ interaction, and improve the sales level by using social media marketing efficiently.

Reaching out the prospects creating automation fu

Developing an automation funnel for a successful e-commerce marketing strategy passes through different phases and each of them has its own software for improving efficiency and outcomes. Here is the whole process and common funnel applications:

Awareness

- Consistently post and schedule content across social media platforms using tools like Buffer, Hootsuite, or Sprout Social.

- For those new subscribers, establish your brand presence and share valuable information by using automated email series from Mailchimp, HubSpot, or ActiveCampaign.

Consideration

- You can automatically score leads based on how they interact with your web site and emails by making use of customer relationship management (CRM) systems such as Salesforce, HubSpot CRM, or Zoho CRM.

- Based on user behaviour and preferences, personalise email content automatically using Mailchimp, HubSpot, or Klaviyo.

Conversion

- Tools like Klaviyo, Omnisend, or the inbuilt features of Shopify can be used to send automatic reminders to customers who have not purchased the items that were added to their cart, including providing them a reason for purchasing.

- Google Ads, Facebook Ads, or AdRoll enable the delivery of personalized ads to your site visitors autonomously.

Retention

- Keep clients engaged by using tools such as Mailchimp, HubSpot, or Klaviyo for automating feedback requests and thank-you emails.

- Employ Smile.io, LoyaltyLion, or Yotpo software to control loyalty points through reminders for rewards and supply special terms of offers to loyal clients.

Analytics and optimisation

- Data collection and reporting can be automated with tools such as Google Analytics, HubSpot, or Mixpanel in order to track the performance of campaigns.

- Set up automated A/B testing for email subject lines, content, and ads using software like Optimizely, VWO, or Mailchimp for continuous improvement in results.

These automation tools allow the smooth management and growth of contacts, the lead conversion process, and customer retention, hence supporting a consistent growth and increase in ROI for your e-business.

Email marketing is evergreen

Image by Ron Hoekstra from Pixabay

With about 4.3 billion people using email every day and 60% of them stating that emails influence their purchase decisions, email marketing is a very effective strategy to nurture leads, drive conversions, and increase customer retention for e-commerce businesses, with the lucrative benefit of being cost-effective. Through email marketing, for every $1 spent, there’s a return of $36, which concludes that it generates the ROI, which is 1.5 times more than SEO and 18 times higher than PPC.

It has been found that 76% of consumers get frustrated after receiving generalised communications from brands. Email marketing helps in approaching prospects with a personal touch. Email marketing tools like Mailchimp, Klaviyo, Drip, Omnisend, ActiveCampaign, SendinBlue, GetResponse, AWeber, ConvertKit and Mailerlite can play an empowering role in the growth of e-commerce businesses. Below are some ways of achieving email marketing implementation effectively:

Lead capture and segmentation

- You should consider putting the opt-in forms in the right areas on your site to gather emails.

- Based on demography, behaviour, geography, and interests, categorise email subscribers into buyer personas according to what they bought.

- Write messages that can be personalised for different groups in your target market.

Welcome series

- While sending welcome emails to new subscribers, make sure you start by introducing your brand and the main products.

- New subscribers should be provided with immediate rewards, like exclusive deals, freebies, discounts, coupon codes, or content.

Educational and nurturing content

- Develop drip campaigns with email sequences that are automated for educational content.

- Make sure the customers are informed about the products, industry trends, and problem-solving techniques.

Promotional campaigns

- Make email messages personalised using customers’ choices and behaviours.

- Use discounts, promotions, and timed deals, including flash sales, as incentives.

Abandoned cart recovery

- It’s been found that around 70.19% is the average cart abandonment rate. Send automated emails with reminders containing pictures of products as well as checkout links.

- Give rewards, such as free shipping or discount codes, to encourage purchases.

Customer feedback and reviews

- When the user buys something, follow up with a thank-you note requesting their opinion and feedback.

- Use support mechanisms that improve belief, such as the user’s testimonial and online comments.

Cross-selling and upselling

- Recommend related or complementary products to customers using their purchase history and browsing behaviours.

- Develop email campaigns in which bundled products are featured at lower prices to increase the value of orders and grow total sales volumes.

Automated customer support

- Videos and pictures that are captivating should be used to elaborate on features of products.

- Foster community trust by encouraging user-generated content.

- Reward repeat customers by conducting customer loyalty programs.

- Real-time interaction and promotions are possible through Instagram Stories and Facebook Live.

Personalisation and dynamic content

- Apply segments of interactive content to craft customised emails that include information such as subscriber names, locations, or even past transactions.

- Utilise mail triggers according to certain actions or behaviours, such as email clicks, website visits, and the period during which a product was last purchased.

Analytics and optimisation

- Observe important parameters in email campaigns, such as open rate, click rate, conversion rate and revenue.

- Running A/B tests on content, titles and calls to action (CTAs) helps enhance effectiveness of email strategies.

Businesses can use email marketing in e-commerce to engage with customers in real time, increase revenue and maintain lasting relationships with them.

Reachout to interested customers by retargeting

Retargeting is an effective strategy in e-commerce marketing aimed at tapping and converting idle clientele formerly exposed to your webpage or interested in the goods you sell. This is how you should employ retargeting strategies for improving the e-commerce performance of your business:

Understand Retargeting Basics

- Use cookies and tracking pixels from Google ads and Facebook ads on the website.

- Segment visitors based on their actions, like the items they viewed, added to the cart, or the particular pages they visited.

Create compelling retargeting ads

- Keep showing ads for products viewed by customers when they visited your website.

- Ensure the items have strong and unique visual representations.

- Add CTAs like “Shop Now” or “Buy Today.” This has an HTML element, but it is not written in a valid way.

Offer incentives

- Emphasise discounts or promotions.

- Present a waiver of shipping fees or discounts on shipping rates.

- Prompt for urgency in shopping.

Utilise multiple channels

- Make use of the Google Display Network and other advertising services.

- Use retargeting methods on platforms such as Facebook, Instagram, or Twitter.

- Deliver personalised messages via email to users who have shown an interest.

Frequency and timing

- Make sure that potential customers get just enough valuable information.

- Once a customer has abandoned their cart, do not wait for more than a few days to follow up with an advertisement that immediately shows up.

Measure and optimise

- CTR, conversion rates, and ROAS can be monitored using analytics tools.

- Ad creatives, copy, and offers can be tested.

- Based on performance insights, targeting, creatives, and offers can be optimised.

Maintain brand consistency

- It is important that advertisements are a true reflection of your brand.

- Every ad should have distinct advertising pages as a way of enhancing interactivity and conversion rates.

Address customer concerns

- Ads should include customer ratings, reviews, and security badges, which can help boost their conversion likelihood by fostering trust among potential customers.

- Increase the likelihood of conversion among potential customers while trying to create a trusting environment.

These retargeting strategies can work for you to recapture the interest of potential customers, encourage them to return to your site and ultimately increase your e-commerce sales.

Confirm the mobile optimisation

Mobile users should be a priority in optimising e-commerce marketing since much online shopping occurs using such devices. Let us now look at what you need to do to ensure that your website is responsive and has all the necessary features for seamless shopping.

Responsive web design

- Verify that the site changes according to the scale of the screen in either portrait or landscape orientation.

- Enhance graphic elements and multimedia output to feature high-speed results and respect sharpness or clarity.

Simplified navigation

- To easily move from one place to another on handheld devices, you should have collapsible menus.

- Ensure that you have a big search box that can easily be seen if you want to get information quickly.

Fast loading times

- Employ WebP for compression when dealing with pictures.

- CSS, JavaScript and HTML need to be compressed into small sizes.

- Content delivery networks (CDNs) and browser caching ought to be used to hasten content delivery.

Mobile payment options

- Make the checkout process simpler by reducing the number of steps and enabling automatic completion.

- Provide multiple mobile payment options, such as credit and debit cards, Apple Pay, Google Pay, and other digital wallets.

User experience (UX) optimisation

- Create touch interfaces that have buttons that are appropriately sized.

- To make it easy to read, large fonts and high-contrast colours should be used.

Mobile-specific features

- Customise user experiences by using location-based services.

- Activate push notifications for promotions and updates.

Optimise for mobile SEO

- Check whether the device is optimised for better search results.

- Make sure Accelerated Mobile Pages (AMP) are available for faster mobile experiences.

Test and iterate

- Administer a number of usability tests on different types of mobile gadgets.

- In order to have different elements with A/B testing, one must supply mobile-friendly live chat choices.

- It’s essential to employ analytic tools for tracking mobile-user behaviour in order to pinpoint areas where enhancements may be made.

Mobile app development

- Crafting an app that is specialised for mobile devices will provide consumers with personal satisfaction.

- Key among the features should be customised item suggestions and easy ordering of things that have been bought before.

Customer support for mobile users

- Provide options for live chat that are mobile friendly.

- Make customer support easily accessible through the phone, email, and social media.

Mobile optimisation enables customers to purchase merchandise and services simply across all devices, thereby boosting connection levels in your online store and enhancing revenue.

Voice search optimisation

More consumers turn to voice assistants like Siri, Google Assistant and Alexa to search for products and make purchases, increasing the significance of voice search optimization for e-commerce businesses. Here is how you can use voice search for e-commerce marketing purposes:

Understand voice search behavior

- Make the content better by using conversational enquiries along with long-tail keywords.

- Begin with searches starting with “why,” “when,” “what,” “who,” “how,” and “where.”

- Improve ranking by aligning with user intention when it comes to content.

Optimise content for featured snippets

- Use scheme marking to help search engines understand your content.

- Respond to customers’ questions directly and straightforwardly.

- Improve customer experience with thorough explanations.

Focus on local SEO for voice search

- Utilise local dialects and keywords to pull in local voice searches.

- Improve Google My Business listings by using specific location, product and service information.

Create conversational content

- Create FAQs written in a conversational manner to help sort out some basic questions.

- Make blog posts that respond to customer queries and give insights about products.

Improve site speed and mobile optimisation

- Make sure fast loading times are achieved on both desktop and mobile platforms.

- Utilise responsive design for improved usability and increased user satisfaction.

Use long-tail keywords

- Put natural long-tail keywords into product descriptions, blog posts, and content.

- Examine voice search patterns to identify appropriate long-tail keywords.

Leverage structured data markup

- Employing structured data marking will give you detailed information on the products.

- Applying local business schemas will help you be more visible when using local voice search queries.

Monitor and analyse performance

- To track voice search performance, use Google Analytics, Google Search Console and SEO tools.

- Optimise based on insights and data that stem from user behaviour.

Optimise for conversational AI platforms

- Google Analytics, SEO tools, and Google Search Console are the tools that can be used to monitor how well a website is ranking for voice searches.

- Improvements should be made by using the information obtained from studying user behaviours.

Stay updated with voice search trends

- Stay tuned for the latest developments in voice search technology.

- Study your competitors’ moves and adjust your tactics in order to remain competitive.

By applying these strategies for optimising voice search, you will enhance your e-commerce marketing, thus making it easier for people to find your products during searches and attracting a wider spectrum of online buyers who make use of voice assistants in shopping.

Paid media promotion

PPC (Pay-Per-Click) advertising is a highly effective e-commerce marketing strategy to enable businesses to drive targeted traffic to their websites and increase sales by paying only when someone clicks on their ads. Here’s how to leverage PPC advertising for your e-commerce business:

Understand PPC basics

- Use social media channels, including Google Ads, Bing Ads, Facebook Ads, Pinterest Ads and Instagram Ads.

- Get familiar with different ad types like search, display, shopping and remarketing ads.

- Match different types of ads with business objectives so as to improve performance during campaigns.

Conduct keyword research

- Tools such as Google Keyword Planner, Ahrefs, or SEMrush to search relevant keywords.

- For higher targeting potential with less competition, focus on long-tail keywords.

- To improve conversion rates, closely align search queries to user intent.

Create effective ads

- Create appealing headlines incorporating primary keywords.

- Make small ads that give prominence to product advantages and finish with powerful CTA.

- It is necessary to improve engagement rates and conversion rates using site links, callouts and structured snippets.

Optimise landing pages

- Make sure the landing pages confirm the advertisement content and key words.

- Enhance page load times, optimize mobile navigation features and simplify pages for accessibility.

- Utilise direct CTAs that spur sales while lowering bounce rates.

Budget and bid management

- Establish PPC campaign budgets depending on the marketing goals.

- Opt for bid tactics: manual CPC, automated bidding, or else target CPA.

- As the performance metrics change, amend bids to ensure proper use of resources.

Targeting and segmentation

- Age, gender, and location may be some of the distinguishing factors of the target market.

- Conduct retargeting campaigns to re-engage with users who visited your website.

- For creating customised ads, segment the audience according to their previous behaviour.

Monitor and analyse performance

- Monitor KPIs, including CTR, conversion rates, CPC and ROAS.

- Use A/B tests to try different ad creatives, headlines, and landing pages.

- Always check performance reports for trends and opportunities for optimization.

Optimise campaigns

- Keep off-topic searches away with the help of negative keywords.

- Discover the right time to show ads.

- Choose suitable locations and develop geo-targeting strategies.

Leverage shopping ads

Google Shopping is among the best eCommerce marketing strategies in 2024. These ads are so impactful that it’s been recorded that businesses attract nearly 85% of all clicks on Google Ads and Google Shopping campaigns.

- Enhance product feeds by using the right titles, images, prices, and descriptions.

- Google Shopping ads generate 76.4% of retail search ad spend. Make use of this in order to be easily found in search results.

- Use dynamic retargeting to display personalised ads that feature items viewed by the visitor before.

Stay updated

- Stay tuned for PPC platform updates and new feature releases.

- Observe the industry norms and keep up with the trends in competitive campaigning.

- Modify strategies to reflect shifts in consumer behaviour and market dynamics.

So, direct traffic and conversions, targeted advertising, cost-effectiveness, and immediate impact are some of the key benefits of PPC in e-commerce. You can utilise these PPC advertising strategies to generate targeted traffic for your e-commerce site, thereby increasing brand awareness and boosting sales.

Affiliate marketing

In affiliate marketing, for the purpose of upscaling sales, an individual or business may collaborate with other individuals or organisations (also referred to as affiliates) who advertise their products and get paid for each purchased item or performed activity. It has been observed that 81% of brands use affiliate marketing. Here are some tips on how to start using affiliate marketing effectively in your web shop.

Set up an affiliate program

- Opt for a partner advertising platform such as ShareASale, CJ Affiliate, or Rakuten Marketing.

- If necessary, apply plugins intended for WordPress, such as AffiliateWP.

- Formulate a compelling commission structure that is either anchored on sales percentages or fixed sums.

- Specifically, detail program needs, including payment timing and advertising guidelines.

Recruit affiliates

- Recognize appropriate affiliates, including bloggers, influencers, or industry professionals.

- Present them with an appealing proposition emphasizing the benefits of the offer.

- Post your offer on affiliate networks for increased chances of getting more partners.

Provide marketing materials

- Create banners and graphics that affiliates can use on websites and social media.

- Give direct links that lead to distinct products for easy promotion.

Track and manage performance

- Tracking tools should be used to monitor clicks, conversions and sales.

- Affiliates should be updated on their performance and improvement areas regularly.

- Fraudulent practices should be detected and prevented to maintain credibility.

Motivate and support affiliates

- For high performers, competitive commissions and bonuses are available.

- Affiliates can get support from the provided training resources, like webinars.

Compliance and ethics

- Ensure that your affiliates comply with the FTC disclosure requirements.

- Observe affiliate content for the purpose of keeping the brand consistent and honest.

Analyse and optimise

- Use metrics like average order value, conversion rates and ROI to measure the success of affiliate program.

- Feedback from affiliates should be taken care of for continuous improvement.

Build relationships

- Build a forum or social media group to share experiences and tips.

- Have constant communication with affiliates to foster engagement and teamwork.

Diversify affiliate channels

- Collaborate with bloggers, YouTubers and social media influencers for diverse content.

- Partner with coupon and deal websites to attract price-conscious shoppers.

- Collaborate with email marketing affiliates to expand audience reach.

Monitor competitor programs

- Study your competitors’ affiliate programs to understand their approaches.

- Refine your own program in order to stay competitive and appealing to affiliates.

You can create a successful affiliate marketing program that drives traffic, increases sales and enhances your brand’s visibility in the e-commerce space by adopting these strategies.

Conclusion

Any organization that intends to excel in the e-commerce industry must come up with a strong marketing strategy for selling goods and services online or through any platform that uses electronic communication. These types of strategies must combine several aspects, such as search engine optimization (SEO), content marketing, social media interaction and tailor-made client satisfaction approaches. Search engine optimization increases visibility on search engines, bringing organic traffic, while content marketing is about building brand authority and developing trust with customers. Through social media platforms, it is possible to reach out to customers and create a community where customer loyalty is built.

Personalization improves the quality of customer service by adapting to the needs of an individual and using data generated insights, making marketing efforts more specialized, increasing their efficiency for better customer loyalty. Consistence analysis and improvement of these techniques help in adaptation to shift trends in markets and consumer behaviors.

A powerful marketing strategy for e-commerce can easily be expanded to enable business growth and allow for smooth entry into new markets. It makes purchases and ROI better, as it also helps in the development of strong bonds with customers that last for a long time and facilitates the return of customers as well as referrals. The businesses can attain long-term development, increase brand passion and stay ahead of competition in the online space.

References

- https://capitaloneshopping.com/research/ecommerce-statistics/

- https://www.wordstream.com/serp

- https://burstcommerce.com/guides/e-commerce-marketing-strategies/#what-is-ecommerce-marketing

- https://ahrefs.com/

- https://backlinko.com/google-ctr-stats

- https://zipdo.co/statistics/ecommerce-seo/

- https://www.semrush.com/features/keyword-magic-tool/

- https://ahrefs.com/keyword-generator

- https://ads.google.com/intl/en_in/home/tools/keyword-planner/?subid=in-en-adon-awa-sch-c-bsb!o3~b4d568bffe74170a0c330e270d0573ad~p71078830187~&&msclkid=b4d568bffe74170a0c330e270d0573ad&gclid=b4d568bffe74170a0c330e270d0573ad&gclsrc=3p.ds

- https://www.forbes.com/sites/forbesagencycouncil/2017/10/30/the-value-of-search-results-rankings/?sh=ae8f9f244d3a

- https://blog.hubspot.com/marketing/what-is-ssl

- https://www.google.com/intl/en_in/business/

- https://www.techtarget.com/searchcustomerexperience/tip/E-commerce-marketing-strategies-for-your-business

- https://www.semrush.com/blog/tofu-mofu-bofu-a-practical-guide-to-the-conversion-funnel/

- https://wifitalents.com/statistic/ecommerce-seo/

- https://www.threekit.com/blog/6-brands-using-augmented-reality-in-ecommerce

- https://www.mayple.com/blog/social-proof-ecommerce

- https://blog.hubspot.com/service/customer-feedback-tool

- https://www.mayple.com/blog/ecommerce-marketing-strategies

- https://www.oracle.com/in/cx/marketing/what-is-ab-testing/#:~:text=A%2FB%20testing%E2%80%94also%20called,based%20on%20your%20key%20metrics.

- https://www.oberlo.com/blog/email-marketing-statistics

- https://blog.adnabu.com/shopify/ecommerce-marketing-strategies/

- https://www.litmus.com/blog/infographic-the-roi-of-email-marketing

- https://www.mckinsey.com/capabilities/growth-marketing-and-sales/our-insights/the-value-of-getting-personalization-right-or-wrong-is-multiplying

- https://www.semrush.com/blog/buyer-persona/#a-buyer-persona-definition

- https://baymard.com/lists/cart-abandonment-rate

- https://ads.google.com/intl/en_in/home/campaigns/display-ads/?subid=in-en-adon-awa-sch-a-bdb!o3~239a4cfc8a351e91806c2a66c6bf167b~p71078811791~&&msclkid=239a4cfc8a351e91806c2a66c6bf167b&gclid=239a4cfc8a351e91806c2a66c6bf167b&gclsrc=3p.ds

- https://www.cloudflare.com/learning/cdn/what-is-a-cdn/

- https://www.semrush.com/blog/amp-pages/

- https://business.adobe.com/blog/basics/digital-marketing-metrics

- https://www.designrush.com/agency/digital-marketing/trends/ecommerce-marketing-strategies

- https://webmarketsupport.com/affiliate-marketing-statistics/

- https://www.ftc.gov/system/files/documents/plain-language/1001a-influencer-guide-508_1.pdf

- https://www.business.com/articles/ecommerce-marketing-strategy/

- https://www.semrush.com/blog/ecommerce-marketing/

- https://www.semrush.com/blog/what-is-a-call-to-action/

- https://blog.hubspot.com/marketing/ecommerce-marketing

- https://influencermarketinghub.com/influencer-marketing-benchmark-report/

- https://mailchimp.com/resources/ecommerce-marketing/?ds_c=DEPT_AOC_Google_Search_ROW_EN_NB_Acquire_Broad_DSA-Rsrc_T5&ds_kids=p80322580036&ds_a_lid=dsa-2227026702184&ds_cid=71700000119083212&ds_agid=58700008729598297&gad_source=1&gclid=Cj0KCQjw1qO0BhDwARIsANfnkv9T5yL2PxvCUExkUvl79xBzi1Q5gwkqmmkEJWUoDizY0u9XxrvosyAaAimeEALw_wcB&gclsrc=aw.ds

- https://www.constantcontact.com/blog/website-10-ecommerce-marketing-strategies/

- https://www.designrush.com/agency/digital-marketing/trends/ecommerce-marketing-strategies

- https://burstcommerce.com/guides/e-commerce-marketing-strategies/

- https://beprofit.co/a/blog/difference-between-digital-marketing-and-e-commerce

")

")

Allow notifications

Allow notifications