This article was written by Nikita Hora fourth year law student of O.P Jindal Law University. Want to share your law school experience? Email your write up to [email protected].

Centre of International Trade and Economic Law (CITEL) is a center run by O.P Jindal Law University. As the name suggest it works in the area of international trade and economic law.

We often prefer buying imported products or in our daily life use so many Chinese good or on every iphone its written designed by Apple California and assembled in China. But does these imported products needs only contract between the seller and the buyers. Is it that simple, because all countries have their rules and regulations moreover the rate of the currency also changes mostly everyday? Is there no scope of conflict between the trading companies? If there is any conflict then how does it get resolved? Is there any body in the world that controls all the countries inter-trade policies?

The answers of these above questions are hidden in International Trade Law. There are a lot of rules, regulations, soft laws, guidelines, treaties etc involved between the trades between the countries. World Trade Organisation (WTO) is the body that has come up with global rules of trade between nations. If there is any conflict between the countries then WTO acts like a tribunal that is called as the dispute settlement body. In other worlds WTO can be also called as forums of trade negotiation. WTO also monitories national trade policies(How it does is mentioned below as CITEL helps to do). It also gives technical assistance and training for developing countries helps to cooperate with the international organization.

In CITEL the first task was exploring the WTO websites as it contains all the relevant rules and regulation required. WTO contains all the key information on trade statistic, trade arrangement and policy, WTO commitments, disputes, WTO commitments, reviews, import and exports, notification, etc of 128 countries.

When WTO was formed in 1986 it only had a system of trade rules and no services were included. On 1 January 1995 General Agreement on Trade and Tariff replaced WTO as the organization was overseeing multilateral trading systems. Those countries who have signed these agreements have officially become the members of WTO. The WTO websites all trade and services topic customs evaluation, tariff and non tariff, import and exports duties, etc of 128 countries. Even it contains all the documents, case laws, and precedents of the disputes that have come in front of WTO. To get the specific and correct information there is intense research skills required and knowledge regarding the concepts and terms.

I have being helping and have an authorship in TPMR (Trade Monitoring Policy Reports) that is useful for the people in IIFT. TPMR is published quarterly of Brazil, China, United States and European Union. In the report we analysis the trade arrangement and policies, regional and international agreement amongst the countries for trade,details about measures which affects imports and exports, investment regime as they are not uniform in all the nation, increase or decrease in taxes which one of the factor that effects the trade and dispute settlement where WTO mostly sets up the tribunal to resolve the matter.

Recently Prime Minister NarendraModi is visiting Japan, often MsSushmaSwaraj (Foreign trips) is out of India they go to various countries to strength relations and sign treaties which affects the trade. The report contains the recent treaties and what effect they in have in which sector of the economy. Often there are reasons when import and exports reduce or stops of poor quality increase in prices etc that is essential information and has to be mentioned in the reports.

So preparation of good reports requires good drafting and intense research skills and understanding and the analyzing the economies.

I have got an opportunity to analysis the free trade agreement (FTA) and Bilateral Trade agreement (BTA) signed between the countries. Recently I have analyzed a FTA of India- Korea that focuses on the movement of Indian Professional in Korea. It needs the understanding of Comprehensive Economic Partnership Agreement (CEPA). It was about the different categories working visa and for the time period that Korean government provides to Indian professional from 160 sectors such as IT. According to Industry body FICCI (Federation of Indian Chambers of Commerce and Industry) the agreement will improve the market access for Indian services providers and professionals.

Korea aims for massive inflows of information technology (IT) workers, engineers, and English teachers as both sides agreed to allow temporary migration of professional workers, which may be threats to local employees in the related sectors, local media expected.

I was a rapporteur for the conference on Trade, Investment and Corporate Governance: Law and Policy in India China and got an opportunity to have escorted the Chairman of Confederation of Indian Industry (CII) where it got a lot of knowledge regarding the position of the economies, similarity and difference between China and India economies and what role and difficulties both the developing countries face in WTO.I got the knowledge of treaties and exception that both the countries have from each other in sector of trade.

Lastly for understanding the international trade and analyzing the economy it is essential to interpret the GATT agreement and have a basic knowledge of Anti dumping, Most Favored Nation (MFN). They are the 2 basic features that are found in most of the disputes. For the interpretation of GATT it is required to read a lot of case and precedent of disputes amongst the trading countries and effected parties.

Conclusion

Through this center I have enhanced my research and writing skills. I know when treaties (BITs, FTAs, MIT etc) have to be referred and how they are interpreted if there are any disputes amongst the countries.

Contact building, giving presentation was something that I learnt when I got an opportunity to attend conference through my center. The most important thing that I learnt is to do work under stress and complete the work on time. I am looking still working with the center on TPRM and on a recent project on India- U.S trade in Pharmaceuticals.

In this blog post, Nimisha Srivastava, a student of Gujarat National Law University, Gandhinagar, writes about temporary injunctions and explains when such orders can be passed by the court.

Interim or interlocutory orders are those orders passed by a court during pendency of a suit or proceeding which do not determine the substantive rights and liabilities of parties with respect to subject matter of the suit or proceeding. Latin maxim “Actus curiae neminem gravabit” which means “an act of the court shall prejudice no one” explains the rationale behind granting such orders. This principle can be found in Section 94(e) of the Civil Procedure Code (hereinafter referred to as the code) which says that ‘In order to prevent the ends of justice from being, defeated the Court may, if it is so prescribed,- (e) make such other interlocutory orders as may appear to the Court to be just and convenient.

Interim orders are necessary to deal with and protect rights of the parties in the interval between the commencement of the proceedings and final adjudication. They prevent abuse of process during the pendency of proceedings. Such interim orders may be summarized as follows:

Commissions: Order 26

Arrest before judgment: Order 38

Attachment before judgment: Order 38

Temporary injunctions: Order 39

Interlocutory orders: Order 39

Receiver: Order 40

Security for costs: Order 25

Payment in court: Order 24

It is a well settled principle of law that interim relief can always be granted in the aid of and as ancillary to the main relief available to the party on final determination of his right in a suit or any other proceeding. Therefore, the court undoubtedly possesses the power to grant interim relief during the pendency of the suit.

The law of injunction in India has its origin in the Equity Jurisprudence of England from which we have inherited the present administration of law. From the aforesaid historical background, it is manifest that the origin of the power to grant injunction is from equity, hence the exercise of the discretion by the Courts is to be governed mainly by equitable considerations. Injunction is stated in Order 39, Rule 1-5,

An injunction is a judicial process whereby a party is required to do, or to refrain from doing, any particular act. It is a remedy in the form of an order of the court addressed to a particular person that either prohibits him from doing or continuing to do a particular act (prohibitory injunction); or orders him to carry out a certain act (mandatory injunction).

Temporary injunction restrains a party temporarily from doing the specified act and can be granted only until the disposal of the suit or until the further orders of the court. It is regulated by the provisions of Order 39 of the Code of Civil Procedure, 1908 and may be granted at any stage of the suit. It remains in force till disposal of the suit or until it is revoked and ad interim temporary injunction remains in force till disposal of the petition for temporary injunction or until it is revoked .The provisions of temporary injunction as well as ad interim temporary injunction is contained in Rule 1 of Order 39 of the Civil Procedure Code.

Case: State of Orissa vs. Madan Gopal[1], an injunction is a judicial process whereby a party is required to do or to refrain from doing any particular act. Temporary injunction is mode of granting preventive relief by the court at its discretion. A temporary injunction is also known as interim injunction.

In Agricultural Produce Market Committee Case[2], the Hon’ble Apex Court has held that “a temporary injunction can be granted only if the person seeking injunction has a concluded right, capable of being enforced by way of injunction.”

Order 39 Rule 1 says that temporary injunction can be granted when:

a) any property in dispute in a suit is in danger of being wasted , damaged or altered by any party to the suit , or wrongfully sold in execution of a decree; or

b) the defendant threatens, or intends to remove or dispose of his property with a view to defrauding his creditors;

c) the defendant threatens to dispossess the plaintiff or otherwise cause injury to the plaintiff relating to any property in dispute in the suit .

In such cases, the court may, by order, grant a temporary injunction to restrain such act, or make such other order for the purpose of staying and preventing the wasting, damaging, alienation, sale, removal or disposition of the property or dispossession of the plaintiff, or otherwise causing injury to the plaintiff in relation to property in dispute in the suit as the court thinks fit, until the disposal of the suit or until further orders.

Rule 2:

According to the Rule 2 of CPC, temporary injunction may be granted where the defendant is about to commit a breach of contract, or other injury of any kind. Where the court is of the opinion that the interest of justice so requires, it may grant temporary injunction. Where the court is of the opinion that the very object of granting temporary injunction would be defeated by delay, it can grant an interim injunction in favour of the applicant. Chartered High Courts also have inherent power under their general equity jurisdiction to grant an injunction restraining a party from proceeding with a suit pending in another court.

To grant the order of temporary injunction is purely a discretionary power of the court .This discretion is to be exercised according to the established judicial principles and judicially. The following principles are laid down for consideration by the court while granting temporary injunction:

Prima facie case

Balance of convenience

Irreparable injury.

Prima facie case:

The expression “prima facie” means at the first sight or on the first appearance or on the face of it, or so far as it can be judged from the first disclosure. Prima facie case means that evidence brought on record would reasonably allow the conclusion that the plaintiff seeks. The prima facie case would mean that a case which has proceeded upon sufficient proof to that stage where it would support finding if evidence to contrary is disregarded. The Supreme Court in Marin Burn Ltd. v. R.N. Banerjee[3] held that ‘A prima facie case does not mean a case proved to the hilt but a case which can be said to be established if the evidence which is led in support of the same were believed. While determining whether a prima facie case had been made out, the relevant consideration is whether on the evidence led it was possible to arrive at the conclusion in question and as to whether that was the only conclusion which could be arrived at on that evidence.’

In Gujarat Electricity Board, Gandhinagar v. Maheshkumar and Co. Ahmedabad[4] wherein it was held that “Prima facie case” means that the Court should be satisfied that there is a serious question to be tried at the hearing, and there is a probability of Plaintiff obtaining the relief at the conclusion of the trial on the basis of the material placed before the Court. “Prima facie case” is a substantial question raised bona fide which needs investigation and a decision on merits. The Court, at the initial stage, cannot insist upon a full proof case warranting an eventual decree. If a fair question is raised for determination, it should be taken that a prima facie case is established. The real thing to be seen is that the Plaintiff’s claim is not frivolous or vexatious.’’

Uttara Bank vs. Macneill & Kilburn Ltd.[5]: The burden is on the plaintiff to satisfy the court by leading evidence or otherwise that he has a prima facie case in his favour of him. It is to be understood that relief of temporary injunction cannot be sought for some right which would arise in future. Similarly, an injunction cannot be obtained to restrain a party from filing a suit. In Seema Arshad Zaheer Case[6], the Hon’ble Supreme Court has indicated the salient features of prima facie case as under: “The discretion of the court is exercised to grant a temporary injunction only when the following requirements are made out by the plaintiff: (i) existence of a prima facie case as pleaded, necessitating protection of the plaintiff’s rights by issue of a temporary injunction; (ii) when the need for protection of the plaintiff’s rights is compared with or weighed against the need for protection of the defendant’s rights or likely infringement of the defendant’s rights, the balance of convenience tilting in favour of the plaintiff; and (iii) clear possibility of irreparable injury being caused to the plaintiff if the temporary injunction is not granted. In addition, temporary injunction being an equitable relief, the discretion to grant such relief will be exercised only when the plaintiff’s conduct is free from blame and he approaches the court with clean hands.” However, in the Best Sellers Retail India (P) Ltd. case, the Hon’ble Supreme Court observed that prima facie case alone is not sufficient to grant injunction and held that: “Yet, the settled principle of law is that even where prima facie case is in favour of the plaintiff, the Court will refuse temporary injunction if the injury suffered by the plaintiff on account of refusal of temporary injunction was not irreparable.”

Balance of convenience:

It is where there is doubt as to the adequacy of the respective remedies in damages available to either party or to both, that the question of balance of convenience arises. The court should issue an injunction where the balance of convenience is in favour of the plaintiff and not where the balance is in favour of the opposite party. The meaning of “balance of convenience” in favour of the plaintiff is that if an injunction is not granted and the suit is ultimately decided in favour of the plaintiffs. The inconvenience caused to the plaintiff would be granted than that which would be caused to the defendants if an injunction is grated but the suit is ultimately dismissed. Although it is called “balance of convenience”, it is really the “balance of inconvenience”, and it is for the plaintiffs to show that the inconvenience caused to them would be granted than that which may be caused to the defendants. Should the inconvenience be equal, it is the plaintiffs who suffer. In other words, the plaintiffs have to show that the comparative mischief from the inconvenience which is likely to arise from withholding the injunction will be greater than which is likely to arise from granting it. In granting a temporary injunction the Court should consider,

Firstly- The plaintiff makes out a prima facie case;

Secondly- That the plaintiff will suffer irreparable loss if the injunction prayed for is not granted; and

Thirdly- The balance of convenience lies in favour of the plaintiff.

Case: MT. AymumNessa v. md. Obaidul haque[7], temporary injunction should be refused in the absence of the above mentioned three principles. In the case of Orissa State Commercial Transport Corporation Ltd. v. Satyanarayan Singh[8], observed: ‘Balance of convenience’ means the comparative mischief or inconvenience to the parties. The inconvenience to the plaintiff, if temporary injunction is refused, would be balanced and compared with that to the defendant if it is granted. If the scale of inconvenience leans to the side of the plaintiff, then interlocutory injunction alone should be granted.

In Antaryami Dalabehera v. Bishnu Charan Dalabehera[9], as this point, it was held that balance of convenience, which means, comparative mischief for inconvenience to the parties. The inconvenience to the petitioner if temporary Injunction is refused would be balanced and compared with that of the opposite party, if it is granted.

In Bikash Chandra Deb v. Vijaya Minerals Pvt. Ltd.[10]: the Hon’ble Calcutta High Court observed that issue of balance of convenience, it is to be noted that the Court shall lean in favour of introduction of the concept of balance of convenience, but does not mean and imply that the balance would be on one side and not in favour of the other. There must be proper balance between the parties and the balance cannot be a one-sided affair.

Irreparable injury:

In Dalpat Kumar & Anr. v. Prahlad Singh & Ors.[11], the Supreme Court explained the scope of aforesaid material circumstances, but observed as under: “The phrases `prima facie case’, `balance of convenience’ and ` irreparable loss’ are not rhetoric phrases for incantation, but words of width and elasticity, to meet myriad situations presented by man’s ingenuity in given facts and circumstances, but always is hedged with sound exercise of judicial discretion to meet the ends of justice. The facts rest eloquent and speak for themselves. It is well nigh impossible to find from facts prima facie case and balance of convenience.”

In the case of Orissa State Commercial Transport Corporation Ltd. v. Satyanarayan Singh[12], the court observed: ‘Irreparable injury’ means such injury which cannot be adequately remedied by damages. The remedy by damages would be inadequate if the compensation ultimately payable to the plaintiff in case of success in the suit would not place him in the position in which he was before injunction was refused.

In this blog post, Garima Jain, a Research Associate and Academic Counsellor at iPleaders.in, gives a detailed analysis of the concept of leveraged buyouts and how they operate.

Introduction

Leveraged Buyouts (LBO) in the technology of globalization mergers and acquisitions have surmised sizeable consequentiality inside us and across borders. These sorts of acquisitions require a sizably voluminous amount of finance. Leveraged Buyouts have emerged as a mechanism to finance these acquisition deals. LBO is, therefore, a financing approach of purchasing personal service corporations with borrowed or debt capital. Cash is commonly borrowed through the acquiring company and the debt financing represents 50% or greater of purchase rate. Tangible belongings are utilized as security for borrowing with the aid of obtaining firm.

Because of the amount of debt involved in the purchase, LBO diverges from other types of acquisitions. A leveraged buyout is akin to buying a house utilizing a combination of a down payment and a mortgage – in both transactions we preserve cash by putting down a modicum in cash and then borrowing the rest. In an LBO, the “down payment” is called Equity (cash) and the “mortgage” is called Debt.

During the 1980s, as much as 90% of the acquisition charge was financed with debt, but degrees now are between 50% to 75% due to the higher requisites from the sources i.e. banks, excessive yield bonds and so on. The concept at the back of excessive debt level is that companies’ free cash drift is to be utilized to pay the debt payments and interest fees. High yield bonds and mezzanine debt have lower requisites than the financial institution mortgage. This implicatively insinuates that buyers having high yield bonds or mezzanine debt are less corresponding for having sizably voluminous loans. Certainly, the hobby quotes consequently are higher for such traders. Enterprise is moreover detailed to sell or exit in a span of five to 7 years after acquisition. LBOs can, therefore, be used by organizations to reap a lower tax protect through incremented debts.

In step with Jensen (1986 and 1989), LBO works as carrot and stick mechanism to improve the corporation’s cash float in addition to reducing fees. It is normally penned under Jensen’s incentive depth hypothesis. Management’s incremented possession and disposition to ameliorate fetches a right result; that is why the metaphor carrot is commonly applied. On the other hand, a high debt level and interest rate payments work as a “stick” to coerce the management to work harder. Jensen argues that accommodating debt payment acts as an incentive for managers to work strenuously.

Three special studies were made by Kaplan (1989), Muscarella and Vetsuypens (1988), and Smith (1989). They were fixated on working performance after the buyout. Studies revealed that the possession by management after two to four years led to an increment (lol, I think it should be increase) in operating profit by forty percent.

Decisions made by managers in the form of increasing investment options are important for valuation of the firm. If managers underinvest, there is a good risk of losing marketplace shares and advantages from the economics of scale (Grant, 1989). Alternatively, If the organization over-invests, it’ll lose price.

General rule or standard provisions on funds raised by private equity firms

Minimum Commitment:

Prospective constrained partners are required to commit a minimum amount of equity. Constrained partners make a capital commitment, which is then drawn down (a “takedown” or “capital call”) by the general partner to make investments with the fund’s equity.

Investment or Commitment Period:

During the term of the commitment period, constrained partners are obligated to meet capital calls upon notice by the general partner by transferring capital to the fund within a concurred-upon period (often ten days). The term of the commitment period customarily lasts for either five or six years after the closing of the fund or until 75 to 100% of the fund’s capital has been invested, whichever comes first.

Term:

The term of the partnership agreed upon during the fund-raising process is conventionally ten to twelve years, the first a moiety of which represents the commitment period, and the second a moiety of which is reserved for managing and exiting investments made during the commitment period.

Diversification:

Most funds’ partnership acquiescent stipulates that the partnership may not invest more than 25% of the fund’s equity in any single investment.

Characteristics of an LBO

Strong Cash Flow: Stable cash flow is essential as debt investors look for firm’s ability to repay debts and shell out/give periodic interest payments. Buyers and investors monitor cash flow through due diligence.

Low financial distress cost: Companies with high financial distress costs are not the best candidates for LBO as financial problem leads to bankruptcy.

Strong Market Position:Buyer and debt investors prefer a firm with strong market position. Therefore, they look for customer relationships, brand name, and better product and service.

Growth Opportunity: Growth increases will lead to an increase in sale which in turn will lead to an increase in cash flow. Thus, interest rates and debt repayments will be easier to meet.

Low capital expenditures: Low investment need improves the ability to increase cash flow.

Strong asset base:debt investors (usually banks) prefer firms with high asset base basically because it will work as a guarantee for their debt repayment.

Cash flow from operating and financial activities can be derived in the following manner:

Cash flow from operating activities – Cash flow from Investing Activities= Cash Available for Debt Repayment.

Mandatory debt, amortization, can differ but is normally 1% of the total debt. The remaining cash flow is used for optional debt repayments.

Cash Available for Debt Repayment – Mandatory Repayment= Cash Available for Optional Debt Repayment

The balance of the first year is the total debt, but for every year that passes and repayment is made.

Formulas:

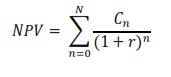

Return analysis is important while decision-making as it provides an answer to return on investment. IRR depends on many different things such as the future financial performance, growth rate, EBIT, the purchase price and the size of equity contribution.

C stands for cash flow at time n, and NPV is the present value of all future cash flow. The initial investment is C0 and NPV is the equity value at time N.

Cash return is the most important. It is a ratio of:

Equity value at exit ÷ Initial equity investment

Models of LBO Financing

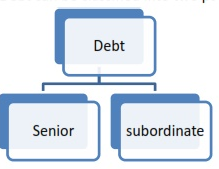

Debt:

Debt can be classified into two parts i.e.

Senior Debt: It is at the topmost rank. Specific assets secure debt. A breach of contract results in the takeover of assets automatically. The cost of debt is thus usually lower, and obligations imposed are quite stringent. Debt repayment for LBO requires a period of 7 years approximately through equal annual installments.

Subordinate Debt: In this type of debt terms are less stringent. At the end of the term, repayment is required in the form of one payment. Lending costs are typically higher as it offers less security to the lender. High yield bonds are publicly handed over to institutional investors using securities. Although they have stringent reporting requirements, they have a fixed rate and can be publicly traded.

High Yield Debts

Ranking

Usually Subordinated or unsecured

Interest Rate

Varies with credit quality, semi-annual payments

Maturity

10 years

Call ability

35% equity

Fees for underwriters

2.5 to 3%

Ratings

Usually B+ to CCC+

Covenants

Governed by Indenture

Marketing

Sold via prospectus

Process

Due diligence, price, documentation

Mezzanine Finance:

Mezzanine finance is utilized as an equity substitute to increment the financial leverage of transactions i.e. the ratio of debt to equity. Mezzanine capital is typically used to fund corporate magnification opportunities, such as an acquisition, incipient product lines, incipient distribution channels or plant expansions; for the company, owners to take mezzanine out of the company for other uses, or avail finance the sale of their business to management or another third party. Mundane features of all mezzanine instruments and products are that they offer a jeopardy/return profile that lies between debt and equity. Mezzanine investment may be more extravagant than traditional bank debt; it is not as stringent. It shares the same covenant package as a traditional bank deal, but the quantification characteristics are more tolerant. Mezzanine facilities are thus often customized or “engineered” to match the cash flow profile of each company

2. Loan Stock:

A term loan has a specified maturity and will during the period pay amortizations according to a schedule. On the date of maturity, a term loan is fully funded. An investigation should be carried out with company’s advisers whether or not loan stock is tax deductible.

3. Preference and Ordinary Share:

Preference shares provide a fixed dividend of the company’s equity which depends on the availability of adequate profits. Ordinary shares are the riskiest among the parts of an LBO capital structure. However, if the risk can be mitigated properly, then ordinary shareholders enjoy benefits.

4. Cash Sweep:

A cash sweep is simply a provision of certain debt covenants that stipulates that any excess cash (namely free cash flow available after compulsory amortization payments have been made) engendered by the bought-out business will be habituated to pay down principal. For those tranches of debt with provisions for a cash sweep, excess cash is utilized to pay down debt in the order of seniority.

5. Bank debt:

Bank debt has got the highest ranking and lowest cost of capital (interest rate). On the other hand, is has got a low flexibility because the borrower has to maintain a designated credit profile and keep certain financial ratios to get the impress. Bank debt, additionally referred to as senior secured credit debt, is a consequential part of the financial structure and will stand for the most astronomically immense part of the sources of mazuma. There are variants of loan inside the bank debt such as revolver credit facility and term loan facilities. They are not very different from each other. The revolver has the competency to recompense liberatingly and re-borrow during the time of the facility as long as it is in line with the conditions in the credit accidence. Homogeneous to the term loan, the revolver has amortizations and interest rate.

Conclusion

Frequently, in lieu of maintaining insolvency, the enterprise negotiates a debt restructuring with its lenders. The economic restructuring might entail that the fairness proprietors inject a few extra cash inside the business enterprise, and the creditors waive components of their claims. In different conditions, the creditors inject incipient coins and postulate the fairness of the corporation, with the existing fairness proprietors dropping their quotas and investment. The operations of the company are proof against the economic restructuring, despite the fact that economic restructuring requires paramount control interest and can result in clients losing faith within the organization.

The incapability to recompense debt in an LBO may be because of preliminary overpricing of the target company and its assets. Over-constructive forecasts of the sales of the organization to be bought out might also moreover result in financial misery after the acquisition..

Leveraged buyout is one of the intriguing routes for those investors who do not have high equity in their pocket and can acquire another target company. The investors can come up with control over the management of the target company. In case the investors have the experience to manage the target company business especially in the case of management buyout in which case the business of the target company will be run by insiders, then the investors can utilize the cash flow coming to such company to recompense the loan taken from the bank. However, there are certain risks if the investors cannot revive the business of the target company and conclusively the prospect of such cash flow for the interest repayment will not transpire. The high-interest rates from such loan may make it arduous for the investors to return the interest and the loan to the bank. In the case of management buyout, it can additionally cause conflict of interest among employees, executives, and the management team. Thus, the stability and experience of the investors are consequentiality factors for running the leveraged buyout investment.

‘R’ is a director of a billion-dollar company. At a board meeting of the company, ‘R’ learned that a famous value investor & billionaire ‘W’ is going to invest in the company. The information is privy only to the directors of the company. Soon after the meeting, ‘R’ calls up ‘RJ’ who heads an investment firm. He says ‘RJ’ that ‘W’ will invest in the company in a couple of days. Seeing that the news would favorably impact the share price of the company, ‘RJ’ purchases the shares of the company with an intention to sell them after ‘W’ has made the investment. As expected, ‘W’ makes the investment. Subsequently, ‘RJ’ sells the shares and makes a profit of nearly a million dollars. ‘RJ’ could not have made this profit without the confidential information that he received from ‘R.’

This is not an imaginary story. The above briefly describes the events which led to the conviction of Rajat Gupta for insider trading and securities fraud[1]. Insider trading involves the use of confidential information regarding a listed company for making beneficial transactions on the stock market. The confidential information is available only to “insiders” i.e.: people who are closely associated with the company – directors, employees, consultants, etc. and is not available to the average trader/investor/public. Given that the information is not known to the market (i.e., trader/investor/public), the impact of the information has not been factored into the share price of the company. The insider is aware of the information and knows it’s likely impact on the share price. When she uses this information by making favorable transactions in the securities of the company, she is said to have indulged in insider trading.

Insider trading is a serious offense when it comes to securities trading and is looked at very severely by stock market regulators. Insider trading creates an unequal playing field among investors; wherein some investors have access to such information which no other investor can access. In a certain sense, insider trading is a fraud committed by the insider on all the other investors. The insider makes illicit profits at the cost of others, and that gives motivation to the regulator to curb the practice. The whole system of the stock market is based on an efficient market hypothesis, which gets shattered through insider trading. As the justice system, the stock market must also be seen to be fair.

However, insider trading is not an easy offense to prove. Often, the insider does not trade in the shares directly as it would be a blatant violation of the law. Insiders use complex channels sometimes involving colleagues (as in Rajat Gupta’s case), domestic helps (as in Anil Kumar’s case[2]), family members and promoter companies (like in Ramalinga Raju’s case[3]), etc. Further, it is difficult to prove that it was only the confidential information that was the trigger for the dealing in securities and not something else.

It is in this light that regulators are expanding their arms when it comes to insider trading regulations. The law needs to be updated to accommodate more secretive communication and liberalised business environment.

Salient Features of the SEBI (Prohibition of Insider Trading) Regulations, 2015

The SEBI (Prohibition of Insider Trading) Regulations, 2015[4] were a much-needed update from the two decades old 1992 regulations[5]. Some of the salient changes between the two are as follows:

According to the regulations, an insider is someone who is either a connected person or is in possession/access to unpublished price sensitive information. In this regard, the definition of a connected person has been expanded and clarified. Included within the ambit are persons who don’t occupy a position in the company, but are involved in a contractual capacity with the company and are in touch with the company and its officers. They are in a position wherein they are aware of the operations of the company. Such a relationship (whether temporary or permanent) must allow (or reasonably expect to allow) access to unpublished price sensitive information.

The definition of price sensitive information has also been modified. The modified definition clearly states that the types of information mentioned therein are merely illustrative, and other types of information may also be included. Among the illustrations, ‘changes in the major managerial positions has also been added.

The 2015 regulations have also widened the prohibitions regarding communication and procurement of unpublished price sensitive information (UPSI). The new regulations state that an insider should not share UPSI not only on a listed company but also a company that is about to be listed.

Further, they prohibit the insider from allowing others to access UPSI, thereby including indirect methods of sharing information. The communication with other persons includes other insiders and hence the dealing of information is intended to be a need to know basis. Inducement and procurement of UPSI have also been prohibited.

Additionally, the 2015 regulations allow sharing of UPSI in cases of due diligence such as takeovers, mergers, and acquisitions. While sharing such information, the parties must enter into a confidentiality and non-disclosure agreement. Further, the parties shall not trade in the securities of the company when in possession of such UPSI.

The 2015 Regulations explicitly prohibit trading in securities while in possession of UPSI. However, the regulations provide for certain situations through which the insider can prove his innocence. These are – off market transactions wherein, both parties make a conscious and informed decision or when no UPSI was communicated by the person possessing the information to the person making the trade or when the trade was in pursuance of a Trading Plan.

The 2015 regulations introduce the concept of Trading Plans. There are certain persons who are perpetually in possession of UPSI. Such insiders may prepare a Trading Plan and present it to the Compliance Officer for approval. Once approved, the insiders can trade in accordance with the plan. This way, the impact of UPSI is neutralized as the trade was decided/finalized even before the availability of the UPSI.

Changes with respect to disclosure requirements[6] have also been made.

Conclusion

The new regulations have tried to address the problem of insider trading comprehensively. However, a lot needs to be done when it comes to implementing the regulations. As mentioned before, insider trading disturbs the underlining assumption that markets are efficient. If insider trading goes unchecked, then the losers in the market (especially retail investors) will lose faith in the market. To them, the market will appear like a loser’s game, and they would channelize their investments elsewhere[7]. This is in complete contradiction to the message that most governments and regulators wish to propagate i.e., channelling part of individual savings towards the stock market (through mutual funds, index funds, SIPs or the like) as opposed to gold, real estate, fixed deposits, etc.[8] So if the government wishes that more people invest larger portions of their savings in the stock market, then it would do well to curb insider trading.

This country has seen several financial scams[9] where retail investors have been cheated and have lost their life savings. Be it Harshad Mehta, Ketan Parekh, Saradha Chit Fund scam or Speak Asia. Indians perceive the stock market either has a giant that eats up out money or a wizard that doubles it in no time. It is the time that changed. Funnily, both are products of information asymmetry.

In this blog post, Ashutosh Singh, a student of Department of Law, University Of Calcutta, who is currently pursuing a Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata, provides investment information to foreigners intending to invest in mutual funds in India.

What is a Mutual Fund?

Before we get into the complexities relating to norms for foreigners investing in Mutual Funds in India, we need to get certain basics clear, and this is the definition and other key elements of a Mutual Fund. The SEBI (Mutual Funds) Regulations 1993 defines a Mutual Fund (MF) as a fund established in the form of a trust by a sponsor to raise money by the Trustees through the sale of units to the public under one or more schemes for investing in securities in accordance with these rules and regulations this is the official definition now let us deconstruct it into smaller parts. So typically we have to emphasize upon the following –

Mutual Fund – Every MF needs to be registered with SEBI structured as a Trust according to the provisions of the Indian Trusts Act of 1882 and the deed needs to be signed by the sponsor and the Trustees only then can it be registered under the Registration Act of 1908.

Sponsor-Is required to have a sound track record and contributing 40% of the net worth of the Asset Management Company (AMC), he is also liable for his acts and that of others.

Trustees– Each MF must have an independent board of trustees 2/3rd of who have to be independent without any relation to the sponsors of the fund. They are required to maintain all the systems relating to the auditors and registrars in place before any scheme is launched; they also have to prevent any differential treatment between the associates of the fund and individual unit holders.

Asset Management Company – The sponsor or the trustees are required to appoint an Asset Management Company to manage the assets of the fund. They have to comply with the mutual fund regulations and SEBI guidelines some of which include aspects such as – the AMC should at all times maintain a minimum net worth of a 100 million, the board of the AMC must have 50% such members who are not related in any manner either the sponsors or the trustees of the fund and also the chairman of the AMC must not be a trustee of any mutual fund etc.

Custodian- Every mutual fund under the mutual fund regulations id requires to have a custodian appointed to carry out the custodial services of the fund the precursor to be being appointed as a custodian includes the presence of the necessary infrastructure and organizational strength. It must also be made clear that the custodian must have no relation to the AMC and must be registered with SEBI under the Custodian of Securities Guidelines, 1996.

So a diagrammatic representation of a general mutual fund would appear like this-

Securing Investments

Now having discussed the basic structure we move on with foreigners investing in mutual funds, there are three ways of securing investment under this head they are –

Ownership of AMC and mutual fund – This happens when international players like Prudential of UK, Alliance, ANZ Grind lays decide to set shop in the domestic market by having their own Asset Management Companies . in doing so they have to be careful towards the foreign investment guidelines prescribed by the Foreign Investment Promotion Board (FIPB), under the current rules this form of asset creation comes under the NBFC – non-banking finance activity in accordance with the sectorial capitalisation norms:

What this cap on capital investments have done is that a lot of foreign investors have adopted the joint venture model of investment through the direct route and this requires no prior approval of the FIPB.

Offshore mutual fund route – This method of investment is suited for those foreign investors who are not willing to enter the domestic market themselves but are willing to participate in the domestic capital market operations. They are done by setting up of funds in a favorable tax jurisdiction the monies for this fund are raised from overseas investors and are invested into the domestic Indian mutual funds. The scheme is structured as such that all units are available to the overseas fund, and then these funds are invested in securities of Indian companies. The AMC along with the overseas fund both need to be registered with SEBI. SEBI looks into the following criteria before granting sanction -.

The overseas fund must be a categorically a broad fund

Approval of RBI and the Ministry of Finance under section 115ABof the Income Tax Act of 1961.

The scheme under this category must report its net asset value on a monthly basis.

The Investment Management Agreement must be recorded with SEBI.

This method of funding has been successfully undertaken by the UTI to raise funds from overseas investors and includes in itself the benefits which are provided under the DTAA (Double Tax Avoidance Agreement) Mauritius route.

Foreign Institutional Investors (FII) – For investment through this route, prior approval of RBI is under the guidelines of the Foreign Exchange Management Act 1999. SEBI, however, provides a single window clearance under this route for all operations in the domestic market under the SEBI (Foreign Institutional Investors) Regulation 1995. After obtaining permission under this, the FII are free to perform a wide array of activities like buy – sell securities issued by an Indian company, realize capital gains on an investment made through the initial amount , subscribe to or renounce right offerings of shares, appoint a domestic custodian, etc.

Now having mentioned the ways of obtaining foreign investment we must throw some light upon the recent developments in this field by the UK Sinha Committee report on Working Foreign Investment, the basic contentions of the report are as such –

The committee is called for the restructuring of the capital flow management system.

It is also called for a single window registration and investment administration process and a creation of a new category of investors called the Qualified Foreign Investor.

Providing such a framework of Qualified Depository Participants (DP) with a wide branched network responsible for enforcing OECD and standard KYC requirements.

The committee also prescribed detailed background checks for such high capital DP’s operating in the country,

It has also suggested the abolishing of NRI’s and FII’s as a separate investor class.

Globally countries including the likes of Brazil, South Korea, and Turkey do not fragment their markets by distinguishing between the types of investors.

Benefits due to these recommendations in the Mutual Fund Market –

The Global Depository Participants would meet the KYC requirements.

The mutual funds would not have to go through the hassles of setting up of an offshore vehicle for marketing their products.

The cost of compliance would come down, significantly.

The Prevention of Money Laundering Act, 2002 guidelines for suspicious transactions, would be dealt with by the DP’s.

Foreign Investment Routes

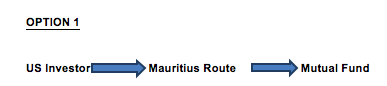

Now we discuss the two basic routes for foreign investment assuming the foreign country of investment to be the United States of America.

Capital gains tax is not taxed in India as well as Mauritius per DTAA between India and Mauritius.

Capital gains tax is to be in India.

Now comparing these two models of investment the first option is more favorable from the point of view of the foreign investor because –

No withholding of tax in India if invested through the Mauritius route and no capital gains tax as Mauritius is a tax heaven.

Subjects of countries with whom a bilateral trade treaty exists are subject to no tax or favorable tax as compared to those of other countries which in this case is Mauritius.

Thus the need for a residence-based system of taxation instead of a source based system was recommended by the committee.

Thus, these are the various aspects which along with the sectoral compliances are to be kept in mind by a foreign investor while investing in Mutual Funds in the Indian market.

This blog post by Divya Kathuria, a student of Raffles University, provides an overview of the subsidiaries that are eligible to lend money by way of an ECB.

What is ECB?

ECB stands for External Commercial Borrowings and to put it as simply as possible; money borrowed in India from foreign or external sources and the purpose of borrowing that money is for using it in commercial activities. These are the loans from non-resident lenders. So, the definition of ECB has the following ingredients:

Money is borrowed.

The borrowed money is from foreign sources.

The borrowed money is to be used for commercial activities in India.

It is important to note that all the above-mentioned ingredients have to be cumulatively present to call a borrowing as ECB. Also, before getting on to who are the eligible lenders by way of ECB; let us be acquainted with certain basics of ECBs.

What are the Different Foreign Sources?

ECB can be raised by borrowers from internationally recognized sources such as:

International banks (to provide commercial bank loans),

International capital markets,

Multilateral Financial Institutions (such as IFC, ADB, CDC, etc.)/ Regional Financial Institutions and Government owned Development Financial Institutions,

Export Credit Agencies,

Suppliers of Equipment,

Foreign Collaborators and

Foreign Equity Holders (other than erstwhile Overseas Corporate Bodies).[1]

Regulations

ECB guidelines and policies are regulated by various government departments that are, Department of Economic Affairs, Ministry of Finance besides Reserve Bank of India. The policy deals with the eligibility criteria of the organizations that can access the international financial markets, the funds that can be availed through ECBs for every type of entity, their maturity periods, how those funds have to be used that is, their end use and also, conversion of ECBs into equity.

The Reserve Bank of India has now recently permitted issuance of rupee-denominated bonds overseas as well (“RDBs”) by its circular dated September 29, 2015, as the investment and repayment of RDBs in the rupee, will enable the transfer of currency risks from the borrower to the investors.

Advantages for a Company to Apply for an ECB

Cheaper funds: It is cheaper than the domestic debts because of the lower interest rates.

Large availability of funds: The international market is a better option as there is an abundant availability of funds and helps in satisfying large requirements because the availability of funds is large as compared to domestic funds.

Foreign Currency funds: Companies always need funds in foreign currency to expand their business abroad and therefore, this might prove fruitful for this purpose as well. Also, the borrower gets freedom from the exchange risks.

Routes for ECBs

Any borrower who wants to access ECB can do so under two routes, namely:

The automatic route

The approval route.

A corporate, other than a financial intermediary, registered under the Companies Act, 1956 or 2012 can access ECB under the automatic route up to US Dollar $ 500 million in a financial year both for rupee expenditure as well as for foreign currency expenditure for permissible end-uses.[2]

However, the ECBs not covered under automatic route can be accessed through approval route on the case by case basis by RBI.

This policy is mainly operationalised through circulars of RBI.

Who can Lend in the New Framework?

The Reserve Bank of India (RBI) issued a Circular dated 30 November 2015 which made a new framework for External Commercial Borrowings (ECB) and replaced the existing guidelines issued about at least ten years ago. The main aim of the new framework is to liberalize and further improve and encourage the long-term ECBs denomination not only in foreign currency but also, denominations in INR.

For this purpose, RBI has categorized various kinds of ECBs very innovatively. These have been categorized as ‘Track I’, ‘Track II’ and ‘Track III’ under the new framework. Also, there have been various amendments made in respect of other ECBs having an average maturity of fewer than ten years.

Track I

It includes those companies which have Minimum maturity criteria as:-

Three years for ECB up to USD 50 million or its equivalent.

Five years for ECB beyond USD 50 million or its equivalent.

Borrowers are:-

Companies in manufacturing, and software development sectors.

Shipping and airlines companies.

Small Industries Development Bank of India (SIDBI).

Units in Special Economic Zones (SEZs).

Export-Import Bank of India

The recognized Lenders are:-

International banks.

International capital markets.

Multilateral financial institutions (such as IFC, ADB, etc.) / regional financial institutions and Government owned (either wholly or partially) financial institutions.

Export credit agencies.

Suppliers of equipment.

Foreign equity holders.

Overseas long-term investors such as:

prudentially regulated financial entities;

Pension funds;

Insurance companies;

Sovereign Wealth Funds;

Financial institutions located in International Financial Services Centres in India

Overseas branches/subsidiaries of Indian banks (added recently)

Track II

It includes ECBs which have Minimum Average Maturity period of 10 years irrespective of the amount.

The borrowers are:-

All entities listed under Track I.

Companies in the infrastructure sector.

Holding companies.

Core Investment Companies (CICs).

Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (INVITs) coming under the regulatory framework of the Securities and Exchange Board of India (SEBI).

Recognized lenders under this category are all entities listed under Track I except for overseas branches / subsidiaries of Indian banks.

Track III

It also includes ECBs which have Minimum Average Maturity period of 10 years irrespective of the amount that is, same as Track I.

The borrowers are:-

All entities listed under Track II.

All Non-Banking Financial Companies (NBFCs).

NBFCs-Micro Finance Institutions (NBFCs-MFIs), Not for Profit companies registered under the Companies Act, 1956/2013, Societies, Trusts and cooperatives (registered under the Societies Registration Act, 1860, Indian Trust Act, 1882 and State-level Cooperative Acts/Multi-level Cooperative Act/State-level mutually aided Cooperative Acts respectively), Non-Government Organisations (NGOs) which are engaged in microfinance activities1.

Companies engaged in miscellaneous services viz. research and development (R&D), training (other than educational institutes), companies supporting infrastructure, companies providing logistics services.

Developers of Special Economic Zones (SEZs)/ National Manufacturing and Investment Zones (NMIZs).

The recognized lenders are:-

All entities listed under Track I but for overseas branches / subsidiaries of Indian banks. In the case of NBFCs-MFIs, other eligible MFIs, not for profit companies and NGOs, ECB can also be availed from overseas organizations and individuals.

Conclusion

This major set of revised guidelines on ECB has been announced to boost the overseas flow of funds in a liberalized regime with few end-use restrictions unlike earlier. These will also lower down the risk of the borrower. The major advantage is that the Indian entities can avail for ECB through INR denominated bonds and then, the lenders will bear currency risk. Through this new framework, the main intention appears to be to attract the lenders overseas, and that is the reason to cut cost for short-term overseas borrowings.

[2] http://www.finmin.nic.in/the_ministry/dept_eco_affairs/ecb/ecb_index.asp?pageid=2, Ministry of Finance, Government of India, ‘ External Commercial Borrowings.’

In this blog post, Vivek Chattopadhyay, a final year law student of School of Law, KIIT University, provides an outline of the dire condition of the Indian Economy in terms of Money Recovery and Debt Collection so as to bring out the alternative means available at their disposal.

Overview of Money Recovery and Debt Collection in The Indian Economy

India being a developing economy is plagued with a lot of fundamental problems against which there has been no real development for a long time. Of these, the most basic of problem is that of “contract enforcement”. While lack of legal awareness and general education amongst the people of this country is a big factor, the other reason is inefficient, costly and a glacially slow legal system. While getting into contracts, most people do not even consider the remote possibilities of what may happen in the future in case of breakdowns or even if some do, they do not tend to question the terms and conditions or even what are the means available to enforce that agreement in the event the other party does not honor the agreement. According to a World Bank survey, India ranks second last, i.e., 189 out of 191 countries for contract enforcement as per the latest statistics.

Quantitatively speaking, the amount of unclaimed money just sitting in several bank accounts total to over Lacs of Crores. This not only include amounts such as a little over 64,000 Cr. Of unclaimed deposits and 3,500 Cr. Of unclaimed insurance money but also a whopping 30,000,000 Cr of unpaid bills!

Debt Recovery Tribunals, which only banks get to access, have a staggering success rate of under 25%! No wonder there is so much unclaimed money in the economy.

The difficulty in money recovery and contract enforcement leads to a massive uncertainty which is a big cost of doing business in India. Uncertain cash flow is a major factor for businesses closing down in India. It renders the entire business environment ineffective and pulls down India’s score in the Ease of Doing Business Index released by the World Bank. If the Government undertakes to have a more systematic approach to money and debt recovery in general, not only large corporations but also small enterprises will be benefitted with massive competitive edge over others as a whole. Therein lies the purpose of the guide, to not only make aware but also to provide solutions to long standing problems involved with Debt collection and Money recovery. Court systems in India are glacially slow and a business owner should not opt for it unless they have exhausted all other means. In business, time is crucial and everything depends upon the timeliness and reliability of information. Getting stuck with an expensive and slow litigation is a thing no one wants and so this guide, to make them aware of the alternative means they can take to recover their dues.

Money Recovery and Debt Collection in India: Why is it so Difficult?

Issues with Money Recovery

Some of the most common problems with money recovery start from the very inception of the agreement with things like certainty of terms of the agreement, financial background of the parties entering into it, etc. Some of these, the more important and crucial ones are covered below so that the reader can understand and timely avoid these pitfalls.

Problems with Oral Contracts

The problems with Oral contracts is that they are not written down anywhere meaning, there is no paper trail to follow and prove its existence in the event of things going bad. The most basic thing a business owner can do is to avoid entering into oral agreements altogether. This strategy should be quite sound for most situations but what about those instances where the accepted trade practice is oral contracts? For such instances, the best thing to do, is to have witnesses who can attest the existence of such contracts in the event of a breach.

Faulty Written Agreements

One might think that shifting from Oral contracts to written ones might possibly solve all your woes but guess what? Written ones have even more problems. Unlike oral ones where if you can prove the existence of such an agreement, your job is done, but in written ones, that’s just the very beginning of the entire process.

The problem mainly with written agreements is that many parties do not have the habit of asking questions about terms and conditions, and that a great majority of contracts are very poorly drafted. Many a times people enter into agreements which turn out to be null and void at the very beginning leading to cancellation of the entire thing and the person who lent the money is left with no recourse.

Always ask as many questions as you can before signing something. If something sounds fishy, question it! If you feel something is vague, question it! Questioning something will not only clear your doubts but also keep the opposite party always on their toes and they’ll think twice before trying to cheat you.

Issues with Jurisdiction

Jurisdiction is critical because it tells you where you can or have to go to enforce a certain contract. If a contract is executed in Delhi that specifies the governing jurisdiction as the State of New York, in the event of a breach, almost never would the aggrieved be willing to go to New York to enforce it.

As a standard practice, there is almost always going to be a pre-determined jurisdiction governing the agreement. You should look into this particular jurisdiction and adjudge whether it would be favorable for you in the event you need to enforce it. In the rare instances where jurisdiction is missing, law in general says, it shall be the jurisdiction of where the contract is being entered into.

Click Above

Instances of Cheating

No matter how careful you are, sometimes, things just don’t work out. This may be attributed to two aspects namely (a) Being Acts of God and (b) Being Act of Cheating. For the former, there nothing as party to the contract you can do since it is something which is much beyond the scope of foreseeable outcomes. But, in case of the later scenario breaches can be attributed to the acts of the other party.

Figuring something out on the face of it might be a bit difficult so the best thing as a contracting party a person can do is to look into the background of the other party to get a rough idea of the character of the other party and decide accordingly.

Bankruptcy of the Borrower

With cheating out of the way, there is another thing that may happen, i.e., Bankruptcy. Bankruptcy relates to the other party being completely unable to execute the contract due to a complete cash crunch and possible insolvency from his end.

The best way to avoid such a scenario is to look into the balance sheets and financial statements of the other party at the point of signing. If things seem sketchy, it’s advisable to either not enter into the contract or to ask for Indemnifiers or Guarantors.

Issues with Corporates

The main problem with corporates is a lot of red-tapism, communication gaps and inefficient management. As a contracting party, a person can have two types of relationships with a corporate. The first being an investor relationship, the second a business relationship. For the former, although the SEBI Act, Securities Contract Regulation Act and the Companies Act lays down fixed timelines, the main problem is that the investor is not aware of his right at the time of signing the agreement

The best way to know the rights an investor has is to either go through the SEBI website once or attend any of the SEBI camps aimed at increasing investor education so that the investor can assert his rights and take what is owed to him.

For the later bit when there is a business relationship, red-tapism is the primary problem where the best thing to do as a contracting party is to establish a proper person of contact in the higher management and get things done through that person so that, there is minimum confusion and errors due to time lag and communication gaps.

Issues with the Slow Legal System

Let’s face it, the main reason why most business owners do not want to go through the entire court process is due to the painfully slow legal system. The remedy to this is to opt for alternative means in enforcing the contract such as through Legal Notices, F.I.Rs, and Complaining to regulator, etc., before heading to court.

Finally, if nothing works, then only the person should head to court to have his matter sorted out. The most effective way to end court proceedings quickly is to go for summary proceedings under Order 37 of the Civil Procedure Code. Summary proceedings are all based on written statements from both parties without any unnecessary trial hearing and this drastically reduces the time lag from filing to judgment.

Expensive Arbitration

If there is an Arbitration clause in the agreement, a court will not entertain the suit. Then the only alternative the aggrieved has is to go for Arbitration. Although Arbitration is a much faster means than litigation, it is a much more costly affair than litigation. The best way to curb Arbitration expenses is to go for Institutionalized Arbitration since the institution have a fixed rate chart and the aggrieved has to pay only the amount which significantly reduces costs.

Expensive Lawyers

Another big reason why people don’t go for Money recovery is because of the rates charged by their lawyers. The general trend is that, the aggrieved is exploited into paying much more than he should be due to his lawyer. The easiest way to remove such difficulties is to contact Legal aggregators and such services who maintain a database of qualified and cheap lawyers willing to quickly settle their matters.

Remedies to Such Issues

Once a contract has been breached, the first thing an aggrieved party should do is refer to the contract to check his available remedies. There are a lot of things a person as an aggrieved party can do once a contract has been breached, which are discussed here in brief and in detail at a later chapter in this guide.

Civil Remedies Available

In terms of civil remedies, there are a lot of things an aggrieved party can do ranging from very simple things like sending a legal notice to things like initiating a civil suit for damages or debts due.

Civil suits take a tedious amount of time and should be resorted to only when the main relief the aggrieved is seeking is monetary in nature. For more serious consequences, without delay, the aggrieved should opt for criminal remedies.

Criminal Remedies Available

For seeking criminal remedies, the first thing to do is once the jurisdiction is established the agreement is to forthwith file an F.I.R with the local police station having jurisdiction over the matter and set things in motion. Once a sufficient amount of evidence has been gathered through police investigation, a criminal suit should be initiated for quick disposal of the matter.

Out of Court settlements

Finally, for high monetary value contracts, the best way is to settle differences and cut off loses through alternative dispute mechanisms such as Arbitration or Mediation. This is a method which is most effective against corporates as the matter can be resolved very expeditiously without furthering the loses they’d normally have to bear without having to resort to the tedious court process.

For Out of Court settlements, the contract needs to specifically speak of Arbitration/ Mediation/ Conciliation or both parties need to agree to it. Without the presence of either, an aggrieved cannot go for this method of Debt recovery.

Laws Currently in Place

The purpose of this chapter is to acquaint the aggrieved with relevant statutory information that he should know in the event there is a breach. One thing to be kept in mind throughout this chapter is that, if the aggrieved is going for a civil suit before a court, he should go for a Summary Suit under Order 37 of the Civil Procedure Code as those are heard and disposed off in a much more expedited manner. This, will in the long term, not only save time but also money and face of both parties. The most relevant provisions of selected statutes that an aggrieved should be acquainted with are discussed herein below.

Contract Act, 1872

The Indian Contract Act, 1872 is the mother law in Debt recovery as all such matters originate from a Contract. There are a number of provisions of this particular statute to be kept in mind while going to file your file your suit before a court of law namely:

Section 17: Fraud

““Fraud” means and includes any of the following acts committed by a party to a contract, or with his connivance, or by his agents,1 with intent to deceive another party thereto his agent, or to induce him to enter into the contract;

the suggestion as a fact, of that which is not true, by one who does not believe it to be true;

the active concealment of a fact by one having knowledge or belief of the fact;

a promise made without any intention of performing it;

any other act fitted to deceive;

any such act or omission as the law specially declares to be fraudulent.”

This section is applicable when there it is proven by some form of evidence that the breaching party planned to do so all along.

Section 18: Misrepresentation

““Misrepresentation” means and includes –

(1) the positive assertion, in a manner not warranted by the information of the person making it, of that which is not true, though he believes it to be true;

(2) any breach of duty which, without an intent to deceive, gains an advantage to the person committing it, or anyone claiming under him; by misleading another to his prejudice, or to the prejudice of any one claiming under him;

(3) causing, however innocently, a party to an agreement, to make a mistake as to the substance of the thing which is subject of the agreement.”

This section is applicable when there is a variation in the intended performance of the agreement due to a difference in the intention amongst the contracting parties.

Section 124: Contract of Indemnity

“A contract by which one party promises to save the other from loss caused to him by the contract of the promisor himself, or by the conduct of any other person, is called a “contract of indemnity”.

Section 126: Contract of Guarantee

“A “contract of guarantee” is a contract to perform the promise, or discharge the liability, of a third person in case of his default. The person who gives the guarantee is called the “surety”, the person in respect of whose default the guarantee is given is called the “principal debtor”, and the person to whom the guarantee is given is called the “creditor”. A guarantee may be either oral or written.”

These sections are applicable in the event there is an indemnifier or a guarantor present as discussed in the matter of possible bankruptcy.

Section 73: Compensation of Loss or Damage by breach of Contract

“When a contract has been broken, the party who suffers by such breach is entitled to receive, form the party who has broken the contract, compensation for any loss or damage caused to him thereby, which naturally arose in the usual course of things from such breach, or which the parties knew, when they made the contract, to be likely to result from the breach of it. Such compensation is not to be given for any remote and indirect loss of damage sustained by reason of the breach.

Compensation for failure to discharge obligation resembling those created by contract: When an obligation resembling those created by contract has been incurred and has not been discharged, any person injured by the failure to discharge it is entitled to receive the same compensation from the party in default, as if such person had contracted to discharge it and had broken his contract.”’

When a contract is breached, to enforce it in order to recover debts due, a suit needs to be instituted under this section.

Negotiable Instruments Act, 1881

The Negotiable Instruments Act, 1881 is specifically for those agreements which carry a promise to pay. Things like Cheques, Bills of Exchange, etc., would fall under the purview of this particular act. While approaching a court of law for any sort of enforcement against a Negotiable Instrument to recover debts and money due, this act would apply.

Section 91: Dishonor by non-acceptance

“A bill of exchange is said to be dishonored by non-acceptance when the drawees, or one of several drawees not being partners, makes default in acceptance upon being duly required to accept the bill, or where presentment is excused and the bill is not accepted. Where the drawee is incompetent to contract, or the acceptance is qualified the bill may be treated as dishonored.”

When the person to whom the Negotiable Instrument is presented does not accept it by any reason whatsoever except for lack of funds this section would apply.

Section 92: Dishonor by non-payment

“A promissory note, bill of exchange or cheque is said to be dishonored by non-payment when the maker of the note, acceptor of the bill or drawee of the cheque makes default in payment upon being duly required to pay the same.”

When the person to whom the Negotiable Instrument is presented does not honor it by virtue of lack of funds this section would apply.

Section 138: Dishonor of Cheques

“Where any cheque drawn by a person on an account maintained by him with a banker for payment of any amount of money to another person from out of that account for the discharge, in whole or in part, of any debt or other liability, is returned by the bank unpaid, either because of the amount of money standing to the credit of that account is insufficient to honor the cheque or that it exceeds the amount arranged to be paid from that account by an agreement made with that bank…”

This provision is much like the previous two with the only difference that, this is applicable only in case of Cheques. A bulk of contract enforcement matters under the Negotiable Instruments Act come under this provision.

Arbitration and Conciliation Act, 1996

This Act would apply only under two conditions where, (a) There is an explicit Arbitration Clause present within the agreement sought to be enforced or (b) When both parties agree to go for it in their best interests to avoid tediously slow litigation.

Section 7: Arbitration agreement

“In this Part, ‘arbitration agreement’ means an agreement by the parties to submit to arbitration all or certain disputes which have arisen or which may arise between them in respect of a defined legal relationship, whether contractual or not.

An arbitration agreement may be in the form of an arbitration clause in a contract or in the form of a separate agreement.

An arbitration agreement shall be in writing.

An arbitration agreement is in writing if it is contained in-

a document signed by the parties;

an exchange of letters, telex, telegrams or other means of telecommunication which provide a record of the agreement; or

an exchange of statements of claim and defence in which the existence of the agreement is alleged by one party and not denied by the other.

The reference in a contract to a document containing an arbitration clause constitutes an arbitration agreement if the contract is in writing and the reference is such as to make that arbitration clause part of the contract.”

This is the main provision that a party needs to keep in mind while approaching an arbitral tribunal for settlement of disputes. Without this particular clause present, unless there is consensus amongst both the parties, the aggrieved cannot go for Arbitration.

Indian Penal Code, 1908

If seeking Criminal remedies to enforce a contract for recovery of debt, this Act would apply. Through the Indian Penal Code, the aggrieved can go for criminal suits against the party that made the breach. The relevant provisions to be kept note of are:

Section 405 and 406: Criminal breach of trust and its punishment

“Whoever, being in any manner entrusted with property, or with any dominion over property, dishonestly misappropriates or converts to his own use that property, or dishonestly uses or disposes of that property in violation of any direction of law prescribing the mode in which such trust is to be discharged, or of any legal contract, express or implied, which he has made touching the discharge of such trust, or willfully suffers any other person so to do, commits ‘criminal breach of trust’ ” and“Whoever commits criminal breach of trust shall be punished with imprisonment of either description for a term which may extend to three years, or with fine, or with both.”

These provisions are applicable if the breaching party denies the existence of the contract as a whole.

Section 403: Dishonest misappropriation of property

“Whoever dishonestly misappropriates or converts to his own use any movable property, shall be punished with imprisonment of either description for a term which may extend to two years, or with fine, or with both.”

This provision is applicable when the breaching party by virtue of the breach attempt or successfully converts property of the aggrieved in his own name.

Section 415 & 417: Cheating and its punishment

“Whoever, by deceiving any person, fraudulently or dishonestly induces the person so deceived to deliver any property to any person, or to consent that any person shall retain any property, or intentionally induces the person so deceived to do or omit to do anything which he would not do or omit if he were not so deceived, and which act or omission causes or is likely to cause damage or harm to that person in body, mind, reputation or property, is said to ‘cheat’ “. and “Whoever cheats shall be punished with imprisonment of either description for a term which may extend to one year, or with fine, or with both.”

These provisions will apply when there is a proven case of cheating against the breaching party.

Presidency Towns – Insolvency Act Act, 1909, Provincial Insolvency Act, 1920 and Insolvency and Bankruptcy Code, 2015