This article on how to prepare for law firm job interviews is being republished from A First Taste of Law, which has now shut down.

It has been a long time since I have written on this blog, and some of you, the readers, keep reminding me to write. I was not getting the time to sit down and write something that you would like to read, or probably find useful. It’s time to make up for the lost time with a good post.

I decided to write about job interviews. Interviews are ubiquitous, it is something that almost everyone who goes through the education system faces at some point or the other. And it is one of the most misunderstood things in the world as far as most of the people are concerned.

What is the objective of a job interview?

The objective of the interviewee is to ‘do well’ and get through – for a job, a post, or perhaps a membership. Now, what constitutes ‘doing well’? A lot of time, one gets the feeling that they have done well, only to find out later that they were not selected. At other times, people feel dejected after the interview, only to get a good result afterward. And then you always find people with lesser qualification getting selected over those having superior academic records or qualification at an interview. Why does this happen? The interview always seems to be a big enigma.

There are a few basic things one need to understand about interviews. There are certain basic rules of meeting other people which applies to interviews as well. Beyond that, there is always a purpose for which you are being interviewed, and you must be a good fit for that purpose.

Let’s Imagine that You want the Job of a Life Guard.

Let us presume that you are excellent at swimming, and you are applying for a job that requires a lot of swimming – like that of a lifeguard. We have already presumed you have the necessary swimming skills for doing that job. Now if you have to appear for an interview to get this job, with many other similarly qualified swimmers, how would you differentiate yourself from the rest? This is the question that almost everyone faces – lawyers, engineers, typists and actors alike.

Apart from basic competence, what else do they look at in an interview? Well, while we can rationally generalize to an extent, it makes sense to narrow down to interviews that law students face for recruitment to law firms.

People know that they have to distinguish themselves, but they don’t know How.

That’s why people try to moot, debate, join societies, write articles and so on. They write about all these things in their CV. In their interview, they try to look and sound smart and intelligent. And very often they go wrong. Sometimes they do it right inadvertently. But from what I see, very few try to analyze the process and understand how it all works.

The fitting in and the distinguishing

There are two things that you should do in an interview – show that you fit in and distinguish yourself. Both at the same time. You have to fit into the role the employer perceives the employee to take, and you must still be different from the rest of the applicants.

Is it just academics?

Not really, but usually it is the most important factor as well as far as getting a job in a law firm is concerned. Even in the interview, they try to understand your knowledge of the law and problem-solving aptitude. In one of my interviews, I was given a problem and asked to solve it in 10 mins. I couldn’t solve it entirely, but I was able to show that I am thinking in the right direction and that I have a good knowledge base and the requisite problem-solving skills. The interviewer helped me by giving an important clue and I cracked it. I was selected.

In law firm job interviews for freshers, much of the interview is occupied by questions on law and your academic performance. Expect it. Even if you have not done great academically, you should have a plan of action to prove that you are otherwise good. Lots of people who do not do great academically get through to the best firms that way.

What is preparation?

Preparation is simply anticipating questions and preparing the best possible answer. Of course, you don’t mug up these answers – but you need to be able to say these things readily with confidence. You can not anticipate all the questions, so take help from your friends, parents, seniors – ask them to go through your CV and ask questions about your academics, extracurriculars, anything in you CV. That way you will find out the most likely talking points in your CV and yourself. Identify the interesting and positive talking points, and drive the interview towards these points. Tempt the interviewer to ask you the question you want to be asked. If you say, I am good at negotiating, the interviewer will ask you 90% of the time to give an example of a realm life negotiation you engaged in. Be prepared with a really good story.

Talking points

While making the CV, make sure to put in a lot of talking points. These are like full toss balls, given knowing that the interviewer will ask predictable questions based on these points. If you don’t want to discuss something in the interview, then be kind to yourself and don’t put it in the CV.

Ensure that the talking points are relevant to the job you are seeking. If you are applying to a firm which mostly does M&A, don’t write or talk about family law and IP law articles and papers you may have written. They just don’t care. They would like to talk about something that you have done which is related to corp law. Stuff the CV with those. And vice versa for an IP law firm.

Also, raise the relevant talking points as you speak during the interview, and wait for the interviewer to catch on to those. You can decide on your best talking points beforehand and spring them one by one as the opportunity comes.

Be sociable and friendly

Tons of otherwise good people don’t get jobs because they fail at this. Remember, you are going to work with clients in a law firm. Can you befriend a client? Can you take a client out on a dinner and convince her that you are a very good friend? If not, no matter how good you are at drafting or research, it will be difficult for a firm to retain you. They look for this quality during the interview. They think in the following lines:

Is this girl going to blend with the other associates or will she turn out to be another bitch?

Is this guy a liar? Or is he really as smart as he says he is?

This guys hands are shaking – is he always this nervous under pressure?

If you come across as a nice person, with a warm nice smile, polite but confident, the law firm already wants you – even if you are not in top half of your class. If you are a topper who comes across as a bookworm, too nervous or too arrogant, you know why you are not getting through to interviews while your peers do it effortlessly. This is why it is important to dress well for the interview, too.

Confidence

Be quietly confident – say what you want to say completely, cogently, in a full voice. There’s no better friend like confidence in an interview. If you appear confident, the interviewer already thinks you are alpha quality, who don’t get nervous even before an interview. They’d think you are one of those people who stroll in, make one feel good, walk out with what they want. Veni vidi vici type people. They think that because unlike so many people you have appeared before them – calm and confident. One of the most effective way of distinguishing yourself.

Observe the interviewer

As you speak, as you hear, make eye contacts as if you are giving them your full attention. Making eye contact also shows your confidence. Of course, don’t stare at them in a way that they think you are a pervert. Similarly, smile at appropriate moments but not in a crazy way so that they’d think you are mad. But most importantly, observing them gives you an idea as to how they are receiving your answers. Do they look happy? Do they look bored? Do they seem to be not understanding what you are saying? Are they not agreeing? If you are observing them properly, you’d know it from their expression and will be able to adjust your answer accordingly. Same for telephone interviews, only then you need to hear the tone of the voice carefully.

Know the need

What are you being hired for? Show that you have the ability to do it. Offer to demonstrate. Volunteer information that will help them in making a judgment. To know the need, you may want to do some research. Talk to seniors who are already in the firm. Those who have left the firm. Those who have relatives working there – in a law school, its not going to be difficult. Google the firm and read on internet.

Managing recommendations

This is extremely important. Law firms ask your seniors who are already there for their opinion about you. Are they going to say good things or bad things? It could be a decisive factor. If you are applying to a firm, is there someone who can give a bad review about you out of enmity? Call him long before the interview/shortlisting – and ask for advice about what to do. Listen with genuine concern, thank him a lot no matter how bad advice he gives and keep the phone down. Its a disarming approach. He’ll now have to be a real asshole to say bad things after you have approached him for help. People hate to admit to themselves that they are assholes. If you don’t approach them, however, they are morally free to give any bad opinion that they may have of you.

Do you have anything to share about the above points? Anything important that you think I missed? Please share them in the comments below!

The Junk bond King Mike Milken caused a number of unimaginable takeovers

A hardworking paperboy in Winnipeg, Canada to a jet-setting, big spending CEO in NYC. The world where numbers have significance only if they are followed by nine zeroes and preceded by dollar mark. A bidding war and boardroom drama. Sounds like a movie? Well, yes, but this is not one of your usual John Grisham’s thrillers made into a blockbuster, but a movie based on one of the ‘serious’ and most heavyweight business books. The book deals with one of the greatest takeover battles ever, and while the film may or may not attract the average movie goers, the book has some serious honey for budding corporate lawyers (and even veterans). We bet you’d like the movie, but don’t skip reading it either.

Without further ado, in today’s post I and Ramanuj shall deal with the 2nd book of the series, as promised earlier – Barbarians at the Gate, which has often been called the greatest business book of all time. The characters of this drama, as it is so common in the corporate world, were driven by an intense fervour for money, fame, power and the desire to be the best. They used fiercest of corporate strategies and the most sophisticated tools of financial wizardry. It did not matter that these strategies and tools had not been tested previously on such grand scale before, and no one knew what could ensue. The book has remained a favourite of many corporate lawyers and is widely recommended. With this post, we hope to introduce the book as well as a few concepts of takeover law and finance along with a great story of corporate profits and corporate ego.

The Cookie

Providing a background to the company and its chief executive is necessary. The book is about one of the biggest corporations in the United States of America in the 1980s – called RJR Nabisco. The company itself has been the product of the merger of two smaller companies – RJR, named after R.J. Reynolds, which manufactured cigarettes, and Nabisco – which was the leading maker of biscuits and cookies in America.

The CEO who loved ‘The Good Life’

RJR Nabisco was led by Ross Johnson, a man who had grown from rags to riches using his superb interpersonal skills – he knew when to be nice when to flatter, and how to persuade people. He was an incredible salesman. In a way, he was epicurean as well – he would party hard and binge drink late into the night with his favourites. Over a period of time, he had grown to become the chief of this corporation which held a very important place in the US corporate world. He was quite unorthodox in his behaviour – he would hate presentations and formal studies by his employees projecting the future growth of the company, which ran completely contrary to conventional wisdom.

A Dangerous Habit

The book gives an interesting name to a particular species of corporate activity where change is made for change’s sake – ‘shit stirring’. If there was nothing eventful happening with his company, Ross Johnson would get into shit-stirring mode: relocating workforce and managers, shuffling departments, changing something or the other. In the age of specialisation, it was really difficult to see how this could work – simply put, somebody’s ability as a maths genius doesn’t necessarily translate into a similar genius in poetry. Nevertheless, Ross was able to get things done the way he wanted, and also gave out the impression that something revolutionary is being done. It is very important for shareholders to watch out for ‘shit-stirring’ – a very active manager may be nothing but a shit-stirrer.

How Stock Prices work – and why they can be a CEO’s Nightmare

Every CEO closely tracks the price of his company’s shares on the stock market. The price of a company’s shares is determined by how much the company’s shareholders feel it is worth, and how much those who are looking to buy its shares are willing to pay for it. If people do not believe the company is doing well, few people will want to buy its shares, its present shareholders would like to sell its shares, and as a consequence, the share price will fall.

If, however, the company is doing well, a lot of people will want to buy its shares, and its existing shareholders will want to hold on to the shares, so those who want to buy the shares will have to pay more to exist, shareholders, and hence stock prices will rise. A CEO tends to assess his performance from the way the stock prices of his company move.

The Curious Case of RJR Nabisco

RJR Nabisco was a slight deviant from this expected behaviour. Although the company was doing well and its performance improving, its stock price remained low. A possible reason for it could have been that the market really did not expect tobacco companies to be very profitable in the long run, they expected some sort of anti-tobacco legislation that would make the companies’ operations less profitable by imposing higher taxes, or in some way disincentivise the manufacture of cigarettes.

If a company’s shares have a low price despite the fact that it is performing well, it can be vulnerable to an outsider buying such a large chunk of its shares that it can control the company. This is known as a ‘takeover’ in business jargon. Ross Johnson was worried about an imminent takeover. If somebody else took over his company, his position as the CEO would be threatened, particularly because he may not be able to justify a large part of his own expenses sourced from the company’s revenues (this, obviously, is another persistent malady in the corporate world – public companies being milked in form of unjustifiable corporate perks which can include anything from a private jet to a luxury yacht and these days, ‘bonuses’).

After a takeover, the new owner would try to cut costs and maximise his profits. In order to ward off such a threat, Ross Johnson thought that the best idea for him would be to buy the company himself. This would have put an end to his palpitations about the price of his company’s stock and let him breathe in peace. He could then focus on the long-term goals of the company.

To buy the company, Ross Johnson would have had to buy off most of the shares from its existing shareholders. RJR Nabisco was a listed company, as we know, which means that its shares were traded on stock exchanges. After Ross Johnson would complete buying its shares, the company would not be listed anymore as all the shares would be held by him and his group. The process is known as taking a company ‘private’ in business jargon. This was in the line of the philosophy preached by takeover finance legend Michael Milken of investment bank Drexel Burnham Lambert.

Milken and his followers in the Wall Street believed that companies controlled by a manager-owner perform much better than companies managed by professional managers mandated by a fractured majority of small and dispersed shareholders. This philosophy justified highly leveraged takeovers that often wrecked the financial stability of a company and hence were highly criticized at that time in the media as well as the Congress.

An introduction to the Leveraged Buyout

One may wonder how it is possible for an ordinary CEO to buy out a company of a size such as that of RJR Nabisco, one of the biggest in US at that time. The answer was found in the 1980s in a technique, known as the Leveraged Buyout (LBO) which was in vogue for doing such transactions. This implied raising a huge loan against the target company’s assets – factories, machinery, etc. as some form of security by promising very high interest yields. Large amounts of fund could be mobilised by this method as was demonstrated in several deals prior to that of RJR Nabisco. Since Ross Johnson was at the helm of affairs, he was in a position to do this, subject to the other directors’ affirmation.

Note that such a large amount of loan would have required tremendous cash to be paid off as interest. That, however, was not a problem, as RJR had strong annual cash earnings, generally called cash flow. The cash could be used to pay off the interest on the loan. An additional feature of a leveraged buyout is that some of the businesses of the company are sold immediately upon buying it out, so as to generate some immediate source of money to pay the most short term debts with higher interest, and keeping the long term debts with more borrower friendly terms for regular servicing from the cash flow of the company. Generally the most unwieldy businesses or those which fall outside the core competence of the company are sold first for paying off debts.

A company which may find itself facing a leveraged buyout is generally one whose stock price is undervalued – that is, where investors in the market, for some reason, believe that the company’s worth is not much and hence, there is less demand for its shares than there should be if perfect information was available to the market. Another way of looking at a company worth buying is when the replacement value of the company’s assets, that is, the price one would have to pay to buy similar assets individually from the market, is less than their value on the books of the company.

Successful completion of an LBO is usually followed by selling off its assets (factories, machinery, the manufactured stock, etc.) that individually would yield more money than selling off the shares of the company. Further, all attempts are made to cut costs of the company – any expenditure by the management which is may be too high and unjustified – such as corporate jets, and limousines, when they are not necessary and only for the ‘glamour’ quotient, is sought to be cut.

Often, those who complete an LBO do not want to keep the company forever. When the amount of indebtedness reduces and the operations of the company seem profitable again, it’s shares can be sold on the stock exchange again. This often happens at a very large premium, and is the primary source of profit for those who do an LBO.

Ross Johnson’s Customised Formula for his LBO

Strangely enough, Ross Johnson did not have any of the plans to cut costs on his mind – in fact he was expecting a very handsome remuneration for himself and his favourites pursuant to the LBO – twenty percent of the profits, which was about 2 billion US dollars!

The armoury of the Leveraged Buyout – the Junk Bond

Corporate enthusiasts may want to know some more on how a Leveraged Buy-Out works. Think of a simple marketplace. One buys what they can afford, and if they dont have enough money to buy, they don’t. With introduction of debt financing, one may also take a loan from a bank when they don’t have enough money on their own with the condition that they will pay a higher amount back in the future. Taking a loan makes sense when there is a possibility that one would make profits by deploying the borrowed money in some sort of business or transaction. The amount taken as a loan leverages the original money one had for investment, and one can keep the extra profit earned by deployment of the extra capital received as a loan as long as he pays back the loan with interest. This means one’s earning to capital ratio can drastically increase if they deploy borrowed capital and make profit in the transaction. The loan here works like a lever, multiplying the ability of the original capital to earn profits. More will be explained about leverage towards the end of this post.

A leveraged buyout implies that a very large proportion of the money paid for buying the company is essentially borrowed money. Leveraged buyouts were popularised and made possible by the acumen of a person named Mike Milken, who worked for a firm called Drexel Burnham Lambert and transformed the Wall Street in the ’70s and ’80s with his innovative financial tools and strategies, and made money like no one ever did.

The money in an LBO was raised at a really high rate of interest. This is because it was really risky, and if anything went wrong with the company, the money may not be repaid. Therefore, it had to offer high interest, so as to compensate for the increased risk. This is a fairly simple principle and it applies to ordinary transactions as well.

The instrument through which it was borrowed came to be known as a ‘junk bond’ – signifying that it could be, on account of the risk, a worthless piece of debt! Junk bonds were very popular for quite some time, as they offered huge returns to investors, and in the hands of Milken, it worked like magic.

Who are the Barbarians of the 1980s?

The analogy in the book is taken from the war between the Greeks and the barbarians of Dardania in Iliad, a mythological work of the famous Greek poet, Homer. The reference to barbarians, is used to allude to the firm KKR (named after its founders Kohlberg, Kravis and Roberts), presumably because of the unprecedented scale of the transaction – eventually they agree to buy the company out for 25 billion USD (and that is at the price levels of the late 1980s), which is still one of the largest LBOs of all time. The previous similar transaction was only about one-fifth the value of the present one. The biggest till date is LBO of TXU in 2007 ($45 bn), done by none other than Kravis.

Such a huge amount is astounding also because KKR, in this case, is not with the management’s side but against it, and hence there is complete lack of knowledge of RJR Nabisco’s internal affairs. KKR was never really told about how exactly the company is managed, and how it could be made more efficient, except for one isolated instance described in the book. They merely have some of their financial records, which can disclose numerical figures but fail to indicate the long-term value of a company. Numbers and financial statements can always be tweaked within the legally permitted boundaries, but they are seldom an accurate source of, say, whether employees are working optimally and how their morale and enthusiasm could be increased so that their output is better, and other such factors.

Initially, KKR, led by Henry Kravis in this deal, resented that Ross Johnson did not instruct them as his advisors, and instead consulted their smaller competitor – Shearson Lehman. KKR, of course, knowing that this would be the deal that would catapult their firm into a completely new league, decide to get into the fray nevertheless. They teamed up with Drexel Burnham Lambert, who were best equipped to raise junk bond debt, the magic money of that era, to launch a bid for the company.

A Clash of Egos, and Breakdown of Cooperation

Ross Johnson, however, noticed that KKR clearly have an edge in such transactions, and all of them – Johnson, his advisors Shearson Lehman and KKR, tried really hard to find a cooperative solution. However, talks repeatedly broke down over every kind of issue, big or small, but the key bone of contention remained the relative share that each advisor would take, both wanted a larger share of the pie for themselves, neither wanted to play second fiddle.

Corporate Strategy: KKR’s preemptive instruction, and a Master Dealmaker’s Hidden design

KKR were really eager to see that they get this one right, and hired the best of lawyers and investment bankers. Every side which made a bid, and every advisor to a side, had their own lawyers, which meant that a large number of America’s Wall Street firms were all engaged in the same deal at once. One firm left out in the fray was that of Bruce Wasserstein, an investment banker, probably the greatest deal maker of the 1980s.

KKR hired the services of Bruce Wasserstein (who has been called the Grandmaster of the Mergers & Acquisitions, or M&A era in the book), if not for assigning him a specific role, at least so that he was not instructed by a competing bidder, as they believed that his strategies could foil their plan. Lawyers too, were instructed just so that they are not hired by the opposing side. More on this is to come in the 4th post of this series on Skadden, as this was a common practice as far as Skadden, Arps was concerned.

Bruce Wasserstein was worried that KKR may pose a problem for him, on another deal that he was involved in – the Philip Morris (maker of Marlboro cigarettes) takeover of Kraft, if KKR decided to participate as a competing bidder. He knew that KKR could only be involved in one deal at a time. He played a very nifty move – he leaked out the some of the details of KKR’s plan to the media – so as to make KKR commit to the RJR deal. KKR could not in that case, participate in the bid of Philip Morris for Kraft. He had ensured that his battlefield was safe. In any deal, timing and the element of surprise is of paramount importance, which is why KKR did not take the leak too lightly, although it took them some time to find out who had caused it.

The Global Search for Banks and Lending Institutions

It’s interesting to see how the size of the deal was so big that at the time of launching their bids each bidder went on a global search for all the banks available, afraid that the number of banks capable of such a deal would be too few, and even amongst those who were capable, they may be hired by a competing bidder.

The Bidding Process

The strategies played at the bidding process were commendable. There were two ‘formal’ rounds of bidding – it was interesting to see how KKR suggested that they would pull out of the process, which made their competitors bid relatively low. At the end, they surprised everyone when they go for a clean sweep and bid really high. Their plan was not completely successful, as Ross Johnson’s group bid again, and there were more bids given by each side to match the other.

The bidding process was skilfully handled by Peter Atkins of Skadden, who was worried that any mishap during the same could lead to a headline making lawsuit, complicating matters for everyone involved as things would spiral out of control.

Takeover Defenses – The Golden Parachute

If the management of a company wants to shield it from potentially unwanted acquirers, it may enter into a contract stating that a certain minimum amount (which is normally very high) must be paid to it by the company, in case of unilateral removal. This is known as a golden parachute. The presence of such golden parachutes for the key managerial personnel of a company can increase the price an acquirer may have to pay by a huge amount, and thus discourage unwanted suitors. Ross Johnson’s golden parachute alone was over 50 million US dollars at that time, which he exercised, once his group lost the bid to KKR.

Winner Takes it All?

It can’t be said that the loser of the battle gets nothing. Bruce Wasserstein, who had been part of the firm known as Credit Suisse First Boston (CSFB), had left the firm with a colleague to found his own firm, named Wasserstein Perella. Since his departure, the mergers and acquisitions department of the firm had been faring unremarkably. It was upon the team at CSFB to dare and do something new, and put their firm back onto the map of great merger firms.

They did that by exploiting a loophole in the tax laws, which enabled them to present a very high bid. In fact, the bid was so high that Skadden, as the firm managing the auction, was instructed to evaluate its feasibility. Interestingly, that loophole had also been figured out by a partner at Skadden, who affirmed that the tax aspect seemed genuine. The bid, however, could not sail through as there were doubts whether the proposal could be implemented on time, but that was sufficient for CSFB to get numerous merger deals afterward, and recover from the shadow of its alumnus Bruce Wasserstein.

On the other hand, the book describes how KKR’s challenge began after it won the company, when it had to make it more profitable and repay the debt. It took quite some time, and was not an easy task.

The Follow Up

Some of us may be familiar with KKR, but many of us in India heard of them when they made news for contemplating a significant investment (well, not of the kind they did in the 1980s, and not for doing an LBO) in India’s leading coffee chain, Cafe Coffee Day (CCD).

A large part of RJR Nabisco’s business was sold off to Kraft. This has been in the news, as Kraft has also been involved recently in the takeover of Cadbury (the maker of the famous Dairy Milk and Bournville chocolates).

Problems with the technique of Leveraging

As already explained, leverage simply refers to debt. The problem with using a lot of debt for doing operations is that it acts as an amplifier – it multiplies the risk of profit and loss, so if there are profits, they are much higher than they would have been without the leverage, and losses much more devastating. For example, if I invest Rs. 100 in stock, and its value increases by 20 percent, I gain Rs. 20. However, if I borrow Rs. 900 over my money, and invest a total of Rs. 1000, the same increase shall yield a profit of Rs. 200 – which is in fact double of what I had invested. Now I can comfortably pay back the debt and keep highly enhanced profits. However, if there is a loss of 20 percent over the same amount – if I had invested Rs. 100 of my own, it would still left me with Rs. 80, but with Rs. 1000 as my investment, my loss is Rs. 200, which is double of my owned amount of Rs. 100. In other words, as investment bankers would call it, I would get ‘blown up’. Leverage played a major role in contributing to the current financial crisis and in going down of banks such as Bear, Stearns.

The book is unique in that it portrays the history of every institution involved in the takeover in great detail, and puts it in perspective. It is extremely well-written and much longer than the previous book – try it out for yourself to experience its unique flavour. Do come back next week for the write-up on Liar’s Poker and Wall Street Meat, which showcase investment banking firms of the 1980s and the 1990s and the practice of law the flourished around them.

In this blogpost, Kapil Chawla, BCS, PGDASDD, MBA, LL.B, Post Grad. Certificate in NLP from Inspirative Australia, a Life and Business Coach offering coaching services to Professionals & Entrepreneurs, writes about how neuro-linguistic programming helps lawyers.

Neuro Linguistic Programming (NLP) was developed in the US during the 1970’s by Richard Bandler and John Grinder. The origins of NLP include Behavioural Psychology, Psychometric Profiling, Gestalt Therapy, Sales Psychology and Quantum Linguistics. NLP has been used globally in Business, Education, Therapy, Coaching and Personal Development for over several decades with many senior professional, business and political figures being NLP trained. Some NLP Practitioners even call NLP as Study of Excellence.

NLP has to offer several techniques for lawyers to perform their functions. A lawyer requires a wide variety of skill set to excel in his profession. Some of the important skills a lawyer needs are Communication, Rapport Building, Confidence, Public Speaking, Sales and Quick Learning.

NLP in its tools box has various tools to help a lawyer in building the following skills:

Communication skills for Lawyers

Communication is one of the most important skill for the lawyers, be it written & spoken. These skills are main tools of business for the lawyers. NLP has various tools like Sleight of Mouth Pattern and Eliciting Subconscious Responses to improve the communication skills of the lawyers.

Rapport building skills for Lawyers

As a lawyer one needs to building rapport with not only with the client but also with the judge as well as the opposite counsel. And sooner the rapport is built the better it is for the lawyer. NLP has several techniques like Pacing & Matching and Mirroring to help the lawyers to instantly build rapport with anyone.

Learning skills for Lawyers

A lawyer is a lifelong learner who needs a sharp mind and focus all the time. NLP has several techniques for improving the learning state of any person. As NLP technique called the Hakalau, also called the peripheral vision helps to improve the learning state and bring high focus. There are various other techniques like Circle of Excellence for improving learning skills.

There is a lot more that NLP provides for lawyers for adding to and improving their skill set.

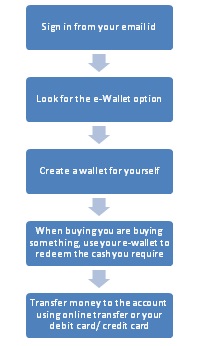

In this blogpost, Saumya Agarwal, Student, Amity Law School, Delhi writes about what are e-wallets, how is it used, benefits, uses of e-wallets and how are e-wallets governed in India.

What are E-Wallets?

E-Wallet refers to an electronic device that allows an individual to make electronic commerce transactions. E –Wallet is an online prepaid account where one can store his money and use it whenever he requires it again. As it is a preloaded facility. Consumers can buy a range of products. It is used to purchase items online with a computer or a smartphone. Nowadays, it is used to verify the holder’s credentials. For example, this e-wallet helps to authenticate the age of a person while he is buying alcohol.

E-Wallet is a feature exclusively for customers who have registered and established a My Account profile. E-Wallet allows you to store multiple credit card and bank account numbers in a secure environment. This saves the users’ time as he does not have to enter the card details again and again. This makes the payments faster, and user-friendly as the user does not have to type much.

How to use it?

To use an E-Wallet these steps have to be followed:

Information stored in the E-Wallet:

E-Wallet stores all of the basic information for credit card, debit card and electronic check processing. For credit and debit cards, this includes the card type, account number and expiration date. For electronic check, this includes the account type, bank routing number and checking or savings account number.

Benefits:

E-Wallet saves the time of the user. The user does not have to look for the credit card/ debit card every time he/she makes a payment. The information is pre-filled. Also, the user can have multiple accounts. He can quickly select another credit card in case he has saved more than one set up in the account. The user can store up to 10 credit/debit card profiles and up to 10 bank account profiles in E-Wallet. The user can pass on the benefits of the e-wallet to his friends and family simply by sharing his account id and the password. Further, the user can delete, edit the information if there is a change in the account number or the account has expired with ease.

Where are the E-Wallets used?

Recharging the Mobile Phones

Fly Prepaid

Utility Payments: Electricity bills, phone bills, hall seats

Online Grocery Stores

Buying Online

How are the E-Wallets/ Prepaid Payment Systems governed in India?

The prepaid payment systems are governed in India by the Reserve Bank of India, under the Payment and Settlement Systems Act, 2007.

According to Section 4 of the Act, no person other than the RBI shall commence or operate a payment system except under and in accordance with an authorization issued by the RBI under the provisions of this Act. The section applies to

The continued operation of an existing payment system on commencement of this Act for a period not exceeding six months from such commencement;

Any person acting as the duly appointed agent of another person to whom the payment is due;

A company accepting payments either from its holding company or any of its subsidiary company or any other company;

Any other person whom the Reserve Bank after considering the interests of monetary policy or efficient operation of payment systems, the size of the payment system or for any other reason, by notification, exempt from the provision.

Also, the RBI may authorize a company or corporation to operate or regulate the existing clearing houses or new houses of the banks in order to have a common retail clearing house system for the banks throughout the country.

Under Section 7 of the act, the RBI can issue or refuse to issue the authorization for operating the payment system under the act.

The things kept in their mind before issuing the authorization are:

The financial status, experience of management and integrity of the applicant

The procedure for setting of payment instructions

The manner in which transfer of funds may be affected

The terms and conditions including their security procedure

The need for the proposed payment system or the services proposed to be undertaken by it;

The technical standards or the designs

Interest of consumers, including the terms and conditions governing their relationship with the payment system providers

Monetary and credit policies

Such other factors as may be considered to be relevant by RBI.

Further, the authorization issued should be in a prescribed form as-

State the date on which it takes effect

State the conditions subject to which the authorization shall be in force

Indicate the payment of fees, if any, to be paid for the authorization to be in force

If it considers necessary, require the applicant to furnish such security for the proper conduct of the payment system

Continue to be in force till the authorization is revoked.

Every application for authorization shall be processed by the RBI as soon as possible, and efforts should be made to dispose of the application within six months from the date of filing of such application.

The RBI has the power to determine the standards of the functioning of the payment systems. Section 10 of the Act gives RBI the power to regulate the functioning.

The RBI may prescribe from time to time-

The format of payment instructions and the size and shape of such instructions

The timings to be maintained by payment systems

The manner of transfer of funds within the payment system

Such other standards to be complied with the payment systems generally

The criteria for membership of payment systems including continuation, termination and rejection of membership

The conditions subject to which the system participants shall participate in such transfers and the rights and obligations of the system participants in such funds.

Further, RBI may from time to time issue such guidelines as may be considered proper for efficient management of the payment systems or with reference to any particular payment system.

The RBI can revoke the authorization for the payment system, change the payment system by issuing a notice; it can call any system provider for such returns and documents or any other information in regard to the operation of his payment system. It also has the power to enter, audit and inspect any premises where a payment system is being operated. The information so received is confidential. The RBI has been given the power to generally give directions and any person to whom the directions are given should comply with them.

The definition of “industry” has evolved and expanded significantly over a period of time by the legislative acts and judicial decisions. The journey of such evolution has been symbolic primarily because of lack clarity in the legislative intent as embodied in the law and conflicting judicial approaches regarding the ambit of such definition. This paper shall be classified into four parts[1].

Part I

Section 2 (j) of the Industrial Disputes Act, 1947[2] can be divided into two components. The first component enumerates as the statutory meaning of ‘industry’[3]; the second component provides as to what does an industry includes[4] within its definition. This definition is not exhaustive and cannot be treated as restricted in any sense has therefore been subjected to immense judicial scrutiny. The landmark judgement is the Bangalore Water Supply case, enlarged the definition to a large extent and over-ruled case precedents which were a part of narrow interpretation, that is to say, before the Bangalore Water Supply case clubs[5], hospitals[6], universities[7], solicitor firms[8], government departments were excluded from the definition of industry but after the Bangalore judgement they have been declared as industry. The triple test of the Bangalore case forms the quintessential part of the amended definition of industry in 1982. The triple test provides that a) systematic activities b) organized by cooperation between employer and employees c) for the production of goods and services calculated to satisfy human wants and wishes would constitute industry. However, this test was subjected to exceptions, namely, industry does not include spiritual or religious services; absence of profit motive or gainful objective is irrelevant (although an organisation will not cease to be a trade or business because of philanthropy animating the undertaking) The main test is the nature of activity with emphasis of employer-employee relationship therefore all organized activities that satisfy the triple test will constitute industry including undertakings, callings and services, adventures’ analogous to the carrying on of trade or business. Thus, professions, clubs, educational institutions, cooperatives, research institutes, charitable projects and (vii) other kindred adventures will not be exempted from Section 2(j) of the Act, 1947 provided the triple test is fulfilled. The Apex Court also enunciated the dominant nature criterion or testaccording to which a limited category of professions, clubs, co-operatives little research labs, and even gurukulas may qualify for exemption if substantively no employees are hired but only in minimal matters some marginal employees are hired without disturbing the non-employee character of the unit. Also, lawyers volunteering to run a free legal services clinic or doctors serving in their spare hours in a free medical centre or if such services are supplied at a nominal cost and the those who serve are not paid remuneration based on master servant relationship then such an institution would not constitute industry even if servants, manual or technical, are hired.

PART II

In the aftermath of the Bangalore case, the legislature intervened and amended the definition of industry which although re-iterated the ratio of the Bangalore case but also excluded certain public utility services and welfare activities from its domain. The amendment (not yet enforced) provided that any systematic activity carried on by co-operation between an employer and his workmen (including independent contractor) for the production, supply or distribution of goods or services with a view to satisfy human wants( excluding spiritual or religious activities). The definition precludes hospitals or dispensaries; educational, scientific, research or training institutions; institutions owned or managed by organisations substantially engaged in any charitable, social or philanthropic service; khadi or village industries; any activity of the Government relatable to the sovereign functions of the Government including all the activities carried on by the departments of the Central Government dealing with defence research, atomic energy and space; number of individual employed in a profession or co-operative society or a society are less than ten. Further clarity in the definition of industry was enunciated in the case of Physical Research Laboratory case[9] in which it was held that a research institute, of the Government department, was not an industry although it carried out systematic activities with the help of employees but did not produce or distribute services to satisfy human wants and therefore there was absence of commercial motive. Also, the Apex Court has held that the Bangalore case is the law of the land and the proposed amendment is not binding yet (as it has not been enforced) therefore the Telecommunication Department of the Government is an ‘industry’ because it is engaged in a commercial activity and do not discharge any of the sovereign functions of the State[10]. Similarly, the functions which are carried on by All India Radio and Doordarshan cannot be said to be confined to sovereign functions as they carry on commercial activity for profit by getting commercial advertisements telecast i.e. except the sovereign function all other activities of employers would be covered within the sweep of term ‘industry’ as defined under Section 2(j) of the Act, 1947[11].

It is noteworthy to mention that a different and contradictory position was taken by Bombay Telephone Canteen Employees’ case[12] (followed theTheyyam Joseph’s case[13]) which the two judge bench observed that if the ratio of Bangalore case is strictly applied then it would yield catastrophic consequences and held that Telephone Nigam of Government is not an ‘industry’ because it is discharging sovereign functions. Along the same lines the Supreme Court faced a dilemma in the Coir Band case[14]primarily because on one hand if the function of the Coir Board is emphasized i.e. to promote coir industry, open markets for it and provide facilities to make coir industry’s products more marketable then it could be held that it is not an industry as its predominant purpose is merely to promote coir business. On the other hand if the tests laid down in the Bangalore case are applied then it is an organization where there are employers and employees to do some useful work for the benefit of others then the inevitable conclusion is that it is an industry. The Court resolved its dilemma by following the former reasoning and observed that not every organization which does useful service and employs people can be labelled as industry. The Court was also of the view that the Bangalore case provides a sweeping definition of industry which is not contemplated by the Act, 1947 and therefore that the matter must be placed before the Hon’ble the Chief Justice of India to consider whether a larger Bench should be constituted to re-consider the decision of Bangalore case. In the recent watershed judgement in Jai Bir Singh case[15]the Supreme Court expressed its concern regarding the excessive pro-workmen interpretation given in the Bangalore caseas it inadvertently overlooked the interests of the employer and ignored the main object of the Act, 1947 (regulation of employer-employee relationship by keeping in view interests of the employers, who has put his capital and expertise into the industry and the workers who by their labour equally contribute to the growth of the industry). Therefore, the Court observed that there was dire need to re-examine such a sweeping definition of industry and allow legislature to draft a more comprehensive definition that adheres to the demands of employers and employees in the public and private sectors.

PART III

The careful analysis of definition of industry as provided in Section 2(l) in the Labour Code on Industrial Relations Bill, 2015 suggests that the legislature has incorporated the elements of Bangalore case by explicitly ignoring the concerns raise in the Coir Band and Jair Bir Singh case. It states that any systematic activity carried on by co-operation between an employer and his workmen (including independent contractor) for the production, supply or distribution of goods or services with a view to satisfy human wants would constitute industry irrespective of whether any capital has been invested for carrying on such activity or whether such activity is carried out with or without profit motive. It excludes agricultural operations unless such operations are integrated with an activity which substantially would constitute industry. This definition is identical to the one proposed by the amendment in 1982, the only difference between the two is that the former exempted certain public utility services and welfare functions of the state from being covered within the definition but the latter does not explicitly provide for any such exemptions. The primary reason for drafting such an expansive definition implies that the intention of the legislature is to protect the workmen who have been excluded by a narrow definition at least till such alternative statutory regimes are enacted.

Part IV

The preceding three parts have elucidated the gradual evolution in the definition of industry. This paper takes into consideration the rationale of the Government, which also forms the foundation of the definition provided in the Draft Code Bill, 2015, for not implementing the amended definition of 1982 i.e. there is no alternative machinery for redressal of the service disputes of the employees of the categories exempted from the definition[16]. However, this paper is of the view that there is need to remove the inhibitions and difficulties faced by the executive in implementing the law, that is to say, the legislature should draft a concise definition with certain restrictions and exemptions; for such exempted categories new legislations should be carved to address any redresses of the employees. It is conceded that demands of the competing sectors have to be taken into account but that should not act as an excuse for non-implementation of legislative intent by the executive. Therefore, the judgement of the Coir Band and Jai Bir Singh seems to be the correct position that such sweeping definition of industry in the Bangalore case needs to crystallised and refined taking into consideration the interests of workmen and employers equally and for achieving the object of the Act, 1947 i.e. growth of industry by harmonisation of employer-employee relation. Similarly, the overarching definition of industry provided in the Draft Code Bill, 2015 which merely reiterates the Bangalore case with no specific exceptions requires modification along the same lines so that floodgates to litigation are not opened.

About the author

This article is written by Sneha Bhawnani, a student of O.P. Jindal Global University.

Get all the templates, formats, step by step guides, checklists and information you need related to employment laws in one place, free of cost. we have simplified compliances, record-keeping, contracts, policies, disputes and litigation for you. Never struggle with employment and labour law again in your life. Click here to download the Legal handbook for HR managers.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content

Endnotes

[1] Part I shall explain the definition of industry as provided in the Industrial Disputes Act, 1947 along with case laws. Part II shall explain the definition of industry as provided in the Industrial Disputes (Amendment) Act, 1982 along with relevant case laws. Part III shall throw light on the definition of industry as provided in the Labour Code on Industrial Relations Bill, 2015 and provide analysis of the same. Part IV shall attempt to provide a critical analysis of the definition of industry and suggest possible changes for its effective implementation.

[3] It relates to the activities of employer- ( i) business, (ii) trade, (iii) undertaking, (iv) manufacture or (v) calling of employers

[4] Nature of work done by employees or workmen – (i) calling, (ii) service, (iii) employment, (iv) handicraft, or (v) industrial occupation, or (vi) avocation of workmen

[5] Cricket club of India v Bombay Labour Union (1969 AIR 276)

[6] Management of Safdarjung Hospital v. Kuldip Singh (AIR 1970 SC 1406); Dhanrajgiri Hospital v. Workmen (AIR 1975 SC 2032)

[7] University of Delhi Vs. Ram Nath (1963 AIR 1873)

[8] National Union of Commercial Employees v. M.R. Meher (AIR 1962 SC 1080) ; Osmania University v Industrial Tribunal Hyderabad (AIR 1960 AP 388)

[9] Physical Research Laboratory v K.G. Sharma 08/04/1997

[10] General Manager, Telecom vs S. Srinivasa Rao & Ors decided on 18/11/ 1997

[11] All India Radio v Shri Santosh Kumar & Anr, Etc (05/02/1998)

[12] Bombay Telephone Canteen v Union Of India & Anr decided on 09/07/ 1997

[13] It was held that functions of the Postal Department are part of the sovereign functions of the state and it is, therefore, not an ‘industry’ within the definition of Section 2(j) of the Industrial Disputes Act, 1947.

[14] Coir Board, Ernakulam Cochin & Anr v Indira Devi P.S. & Ors on 04/03/1992

[15] State of U.P vs Jai Bir Singh Appeal (civil) 897 of 2002 decided on 05/05/2005

In this blogpost, Sonal Srivastava, Student, Amity Law School, Lucknow, writes an overview of the Insolvency and Bankruptcy Code, 2015.

There is a saying that “Capitalism without bankruptcy is like Christianity without hell” and in India, the pursuit of bankruptcy proceedings can be a stressful event. The reason for the same is that India does not have a single bankruptcy code; instead, it works on an assortment of law that governs insolvency proceedings. The present laws are inefficient because they operate at a painfully slow pace as the courts try to interpret the various laws governing insolvency. The Government of India thereby decided to bring forth a new code on bankruptcy and thus introduced the Insolvency and Bankruptcy Code, 2015 in the Lower House of the Parliament on 22nd December 2015 to consolidate and amend the laws relating to insolvency. The present article aims to cover the various aspects of insolvency process and the new code on bankruptcy.

“Bankruptcy” connotes to a legal procedure for liquidating a business (or property owned by an individual) which cannot fully pay its debts out of its current assets.

The two main objectives of bankruptcy proceedings are- (1) a fair settlement of the legal claims of the creditors through an equitable distribution of debtor’s assets and (2) to provide the debtor an opportunity for a fresh start.

Why does India need a bankruptcy law?

The failure of business impacts employees, shareholders, creditors and the economy on a whole. In a country like India because of the delay in making decisions on the viability of businesses, the tactics involved by the promoters in delaying the process of reorganization, attempts to stop selling off assets, the changes in management and the litigation that goes on and on makes the drag on the new business units, economic growth and income generation a significant issue. Though there are laws on bankruptcy such as Security and Enforcement, Corporate Debt Restructuring (CDR), Sick Industries Act (SICA) yet they have proved to be inept in working because of inefficient and weak enforcement and court delays.[2]

India’s plan for new bankruptcy code

PROPOSALS BY T.K VISHWANATHAN COMMITTEE[3]– A committee headed by former Law Secretary T.K Vishwanathan had proposed the following-

A time period of 180 days, extendable by 90 days to deal with resolving cases of Insolvency and Bankruptcy.

During the period of resolving the issue of bankruptcy, the management of the business or the firm would vest in the hands of a Resolution Professional that is a new class of professional equipped to deal with such cases and who would be supervised by a proposed New Regulator.

The proposal also envisages them getting into talks to revive firms and work out a repayment plan.

FINANCIAL SECTOR INSOLVENCIES[4]– The Financial Sector Legislative Reforms Commission (FSLRC) had recommended the creation of a resolution corporation to monitor financial firm and intervene before they go bust. It envisages the aim to either close the firms that cannot be revived or change their management to protect the investor or depositors. The proposal was to promote the Deposit Insurance and Credit Guarantee Corporation (DICGC) as Resolution Corporation.

THE INSOLVENCY AND BANKRUPTCY CODE, 2015[5]– The Union Finance Minister Arun Jaitley introduced The Insolvency and Bankruptcy Code, 2015 in the Lower House of the Parliament on 22nd December 2015, paving the way for a complete overhaul of the current insolvency and bankruptcy system in the country. The bill seeks to consolidate and amend the laws relating to reorganization and insolvency resolution and would also apply to partnership firms and individuals. The bill being a money bill connotes that there would be a limited role of Rajya Sabha, thereby brightening its chances of passage.

Important aspects of the insolvency and bankruptcy code, 2015[6]

Key agencies

The code would apply to Limited Liability Partnerships (LLP’s), partnership firms and companies.

National Company Law Tribunal and the Debt Recovery Tribunal shall be the designated bodies.

Insolvency and Bankruptcy Board of India shall regulate the agencies and the professionals involved.

An Insolvency and Bankruptcy Fund of India would be set up.

How the law would work

Start of proceedings

On default of debt, the financial creditor, operational creditor or the corporate itself can start insolvency proceedings.

Financial Creditor

The Financial Creditor can file proceedings with the National Company Law Tribunal along with the proof of default.

The creditor shall also suggest an interim resolution professional to manage the defaulter.

Operational creditor

They have to give a 10-day notice to the debtor for repayment before taking action.

Corporate creditor

The defaulting company can start proceedings by making a reference to the Adjudicating Authority.

Time to recognize default

Tribunal or the Adjudicating Authority to determine the default within 14 days.

Admission of application

On satisfaction of the default and the antecedents of Resolution Professional by the tribunal, it shall admit the application.

Declaration of moratorium

The Adjudicating Authority shall declare the moratorium to protect the assets and allow the company to function.

Interim resolution professional

The Interim Resolution Professional shall be appointed within 14 days from the date of admission to run the company.

Committee of creditors

The committee of creditors shall be set up to draft resolution plan and shall include all financial creditors of the debtor. They need to take the decision by at least 75% vote.

Appointment of resolution professional

The committee of the creditor shall confirm to the Interim Resolution Professional one or may appoint a new one who shall be responsible for managing resolution process.

Resolution plan

Any stakeholder can present a resolution plan, and the committee of creditors shall approve one plan and present it before the Adjudicating Authority.

Sanctionaing of plan

On being satisfied with the plan, the Adjudicating Authority may approve the same, and the plan shall be binding on all the stakeholders.

Liquidation: Adjudicating authority can order liquidation if-

Resolution plan is not as per rules.

No resolution plan submitted within the specified time limit.

Committee of Creditors request for liquidation.

Debtor Company violates the terms of a resolution

Resolution Professional shall be appointed as Liquidator.

The law enumerates the details of Liquidation Process.

Strict time limit

The code provides for 180 days time limit for completing insolvency process.

In certain cases, the time limit of 180 days could be extended by 90 days.

Fast track insolvency resolution

It is available for a certain class of debtors.

The insolvency process has to be completed within 90 days with maximum 45 days extension.

How will thw law help

It shall protect the interests of the lenders and creditors of the company.

It shall ensure that the productive assets are released quickly.

It shall allow failed businesses to wind up.

It shall help entrepreneurs by quick exits.

Thus the Insolvency and Bankruptcy Code, 2015 once passed shall provide for an efficient and swift insolvency regime and shall ensure greater availability of credit and funds for businesses by freeing up capital thereby boosting innovation and productivity.

In this blogpost, Tanusree Banerjee, Student, South Calcutta Law College, writes about the new securities and exchange board of India (prohibiton of insider trading) regulations, 2015

Introduction

Insider Trading and laws prohibiting it had always been a centre of attraction as it is a fascinating subject. It is now under the spotlight because of the new rules which had been brought into effect by the capital market regulator on 15th May 2015.

As we know that the basic norms governing the world of insider trading forbid anyone from dealing with the firm’s share publicly who has access to the insight knowledge of unpublished price sensitive information. If someone is convicted of doing such an offence, such person could be penalized with 10 years of imprisonment or to pay a fine of up to Rs.25 crore or thrice the amount of profits made.[1]

Given that there may be several officers in a company who may always possess price sensitive information the objective to the Insider Trading Regulations in order to prevent the misuse of such information may not always, be intended with the ground reality of performing several crucial functions of the company by such officers. These come about in no small part because unprincipled traders will always find new laws and escape holes in the rules and regulations governing the insider trading and will continue to make profits out of it in their own secretive ways so as to avoid prosecution.

Even if we keep that aside for a moment, still it is very important for the capital market regulator to structure the insider trading practice since the stock market is getting affected by this which often lead to a huge loss for genuine investors.

Keeping in mind the drawbacks in the insider trading regulations, the Securities and Exchange Board of India (SEBI) has introduced the SEBI (Prohibition of Insider Trading) Regulations, 2015 which will make the insider trading laws more stringent by replacing the SEBI (Prohibition of Insider Trading) Regulations, 1992.

A Brief Analysis of the SEBI (Prohibition of Insider Trading) Regulations, 2015

As we know insider trading is a globalized phenomenon, it was a very good initiative taken by SEBI by introducing new regulations which can match the line of global business. The new regulations are more restrictive, appealing and promising to constrain the insider trading.

Every law should be dynamic in its nature, in order to maintain a constant pace with the changing needs of society. Similarly, laws related to a financial transaction must also need a constant change in order to fulfil the need of the present market dynamics. Based on this concept, we can clearly state that insider trading is also a crucial part of the business transaction, and we have seen that its laws were last notified in the year 1992 and have not changed since then. This lead to impediments in the smooth transactions of listed securities.

The SEBI (Prohibition of Insider Trading) Regulations, 2015 do not take into account the flow of price-sensitive information during the due diligence exercise of a company as part of any restructuring of the company. For instance, for the comfort of private equity investors, demand is made for all legal and financial documents of the company. It is unclear how the regulations would operate vis-a-vis the financial and legal advisors of the incoming investors, should price sensitive information be disclosed to them during due diligence.

This more often leads the unscrupulous investors getting a hand on the price sensitive information about the target company prior to buying stocks, which ultimately becomes a penalized offence of insider trading.

SEBI has introduced these new regulations, trying to make the due diligence a device to curb insider trading. The regulations provide that due diligence needs to be a prerequisite process to determine that whether target listed company is a good deal for the investor; it also states the lacuna and the risks involved in such transaction and helps to determine the stopping cost and acquiring price. However, uncertainty may arise that whether the company and the acquirer will be charged for violation of the law if the deal does not go through.

The new regulations propounded new dynamics of the capital market. For instance, it provides provisions for due diligence when a person wants to acquire a listed company which is subject to competent compliance and proper disclosure, it further defines the term trading and direct more structured disclosure regime.

Give it to that the acquirer becomes an “insider” under the New Insider Regulations. Unlike the earlier SEBI (Prohibition of Insider Trading) Regulations, 1992 when he gets the knowledge “unpublished price sensitive information” (“UPSI”) about the target listed company, which is not readily available to the public. Now, through due diligence sensitive information can be shared or communicated with the acquirer with relation to the business transaction.

The above clause is subject to certain restrictions; it specifically states that the person who has the knowledge of UPSI must sign a confidentiality and non-disclosure agreement. There can be no trade in securities, of the target listed company by the acquirer who has an insight knowledge of UPSI.

These provisions are covered in Regulation 3(3) and 3(4) of the New Insider Regulations. Regulation 3 (3) which permits communication, provision, allowing access to or procuring UPSI to the acquirer, covers only two situations for a transaction: one, when the transaction results in an “open offer” under the SEBI takeover regulations and second when the transaction does not result in an “open offer”.

When the resultant of a transaction is an “open offer”, the UPSI necessitates that the public shareholders of the target listed companies decide whether to retain their shares in the open offer or sell them. When the letter of offer is sent to these companies, this option is readily made available to them. In the event of the transaction not resulting in an open offer, the UPSI should be published two days prior to the actual acquisition by the acquirer.

Prior to the completion of transactions with the acquirer, in both the cases, the UPSI should be made available to the public, thereby bringing centralization of information in the market.

Due to this centralization of information in the market, no one has the other upper hand and the information reception is the same at everyone’s level. According to Regulation 3(3) only two situations are provided which result in acquisition although it is silent where there is no acquisition even after due diligence.

Therefore, we can clearly observe that SEBI has given liberty to the Company to determine the process and the manner of disclosing the UPSI prior to the proposed transaction.

This situation leads to the dilemma of the uncertain reaction of the market and it is also difficult to say the effect and the consequences of such public disclosure of UPSI prior to the proposed transaction, in such instances where an open offer obligation is not set off under the Takeover Code.

Now the question arises that in the case of an M&A transaction if the acquirer does not want to complete the deal, then what will be the status of the UPSI which has already been shared with the acquired? The answer to this is that the acquirer is not entitled to share such information about the target listed company unless it is made public. This was a very prominent step mentioned under the new regulations in order to constrain insider trading.

Further, it is stated under Regulation 3(1) of the New Insider Regulations provides that no insider will allow access to any UPSI relating to a company, or securities listed or proposed to be listed, to any person except under three circumstances: when the communication is in furtherance of legitimate purposes, performance of duties or discharge of legal obligations.

Although the New Insider Regulations is silent on the issue that what will happen if a due diligence of a terminated deal does not come under the purview if the three above mentioned exceptions. It is quite a possibility that it will be used for other legitimate or lawful purposes.

Apart from introducing some basic rules of insider trading, the new regulations have brought some impeccable and significant changes in the world of insider trading. For example, in addition to listed companies, the new regulations apply to companies that are proposed to be listed as mentioned under Regulation 3 of the New Insider Regulations.

The words ‘relating to a company or proposed to be listed’ prima facie seems unwarranted – as definition of UPSI covers information relating to the company or its securities. SEBI may have included these words to give a clear information that UPSI relating to securities need not to be restricted only to the listed companies.

However, the words” proposed to be listed” creates ambiguity as it puts the acquirer of the unlisted company in a jeopardize situation that if he has an insider of a “proposed to listed” company knows any insider information he cannot deal with the securities of such company. Well, this might lead to problems as it might cover the companies who have filed a DRHP (draft red herring prospectus) with SEBI.

The new regulation has increased the scope of the definition “connected person”, now it covers anyone who is in connection or is associated with the company or an organization, even by a conversation with an employee which gives a reason to believe that UPSI can be exchanged. It also includes deemed close relatives, members of the board of directors (which earlier was not treated as a connected person under Section 12A of SEBI Act, under 1992 regulations) and people connected with a decision (that is price-sensitive) as ‘connected persons’. Now includes holding company, subsidiary company and associate company. As regards mutual funds, under 1992 Regulations only employees having fiduciary relation with the company were treated as deemed to be connected. Now the condition of ‘fiduciary relation’ is dropped. Thus, all employees of mutual fund / asset management company are deemed to be connected, person”.[2] The regulations bar any form of communication of such information by the people as mentioned above.

The restrictions on communication by the new SEBI regulations can lead to prosecution even on innocent disclosure of information to any person who falls under the purview of the definition “connected person”. For instance, if a mother shares some information with her daughter, and she does nothing to misuse it, still both of them fall in the wrong side of the new law.

Apart from this, the new regulations also cover the public servants like high-ranking officers, who may not have personal or any professional relationship with the company, but who may be aware of a judgment or policy which, when made public, may impact the price of shares of the company.

Furthermore, the new regulations provide that the compliance officer of the company must supervise and monitor the employees and the connected person while they are trading. As we have observed that the scope of the definition has increased based on such demarcation, the compliance officer may find difficulty while delivering his obligation under this Rules.

The new regulations provide provisions for the formulation of trading plans. According to this provision, one can formulate a trading plan, get it approved by the compliance officer and trade in accordance with it subject to the conditions as specified in the rules, so that any insider information is not misused. “This provision intends to give an option to persons who may be perpetually in possession of unpublished price sensitive information and enabling them to trade in securities in a compliant manner. This provision would enable the formulation of a trading plan by an insider to enable him to plan for trades to be executed in future. By doing so, the possession of unpublished price sensitive information when a trade under a trading plan is actually executed would not prohibit the execution of such trades that he had pre-decided even before the unpublished price sensitive information came into being.” [3]

After the new regime has come into existence, many companies are facing difficulty while trading. “For instance, India Inc is still grappling with the strictures and stipulations. The biggest grey area has been the dos and do not’s on price-sensitive information.

The trading plan would be disclosed to the public, and a person cannot trade within six months of such public disclosure. Further, once approved, the person cannot back out or deviate from the plan.”[4]

As mentioned earlier, the new regulations not only restrain dealing in security but also communicating or procuring of insider information, except where this is in furtherance of, among other things, legitimate purposes.

The phrase “legitimate purposes”, too, has not been defined. Thus, it is very unclear as to what purposes are legitimate enough to allow insider information to be communicated or procured.

The new regulations also direct the companies to formulate codes for regulating, monitoring and reporting trading by employees or connected persons, and fair disclosure of material information, such as financial information, key business decisions, etc., by the company.

These rules are becoming very problematic and cumbersome for large companies, who have a large number of shareholders and employees. SEBI must take certain steps to solve such kind of problem, although that seems unlikely. However, there’s hope that the regulations are interpreted by courts and authorities in a progressive manner, and timely clarifications are issued by the capital market regulator.

The new regulations covered up the lacuna very effectively of the old Act. This can be clearly and briefly explained with the Satyam’s case study. One of the issues faced by the SEBI when dealing with the Satyam scandal was that SRSR Holdings Pvt. Ltd., a holding company, which owned almost all of the shares held by the promoter group of Satyam (SRSR Holdings held 8.27% of the total shareholding of Satyam while the total shareholding of the promoter / promoter group of Satyam was about 8.6%)[5], in which the Directors of the Company had information regarding the financial irregularities present in Satyam, still it went ahead and pledged such securities of Satyam to financial institutions for acquiring loan that amounts to Rs.1258 crore[6]. This Company took the defence that the pledge securities does not constitute the trading of securities as per the old regulation under the definition “dealing in securities”[7]. Based on this we can say that, one of the major change in the new 2015, regulation is that there has been the inclusion of pledge of securities and other activities which are not strictly restricted to buying, selling or subscribing, when in possession of UPSI under the definition of “trading” [8] in order to circumvent the prohibition on sale when in possession of inside information, as similar to Satyam’s case. However, such a move may curb the ability of promoter to bona fide secured credit for the company on an emergency basis. [9] Furthermore, if we consider the lender’s perspective, we can state that these new norms add transparency to the process. Now the share pledge route is clearer and these new trading regulations are in supposition with the RBI[10] guidelines on loans against shares issued on July 1, 2014. Thus, we can say that the silver lining of this is that the pledger or pledgee can use the defences available to them under Regulation 4 and demonstrate that the creation or invocation of the pledge was bona fide, unlike the view which was taken by the Whole Time Member of SEBI in the aforementioned case.

Conclusion

SEBI has remodelled the entire structure of the insider trading mechanism, which is seen to be a very deep-seated problem in India. The country can gloat of the dynamic capital market with its efficient and effective laws and an efficient Regulator. This new regulation has provided a shield to the investors to protect their interest while playing in the securities market. This action of SEBI will provide a much-needed filip and exposure to the players of Indian capital market and facilitate further economic expansion. But above all this, only one thing that is required to be observed is that all the actions of this newly introduced regulations are actually needed to be practiced and must possess a realistic approach rather than just a provision that is comprehended in any statute for the sake of it to be amended later on. From this, we can hope that these regulations may successfully bring new insight to the “insider trading” mechanism in the capital market of India.

[1] Section 24 of The Securities and Exchange Board of India Act, 1992.